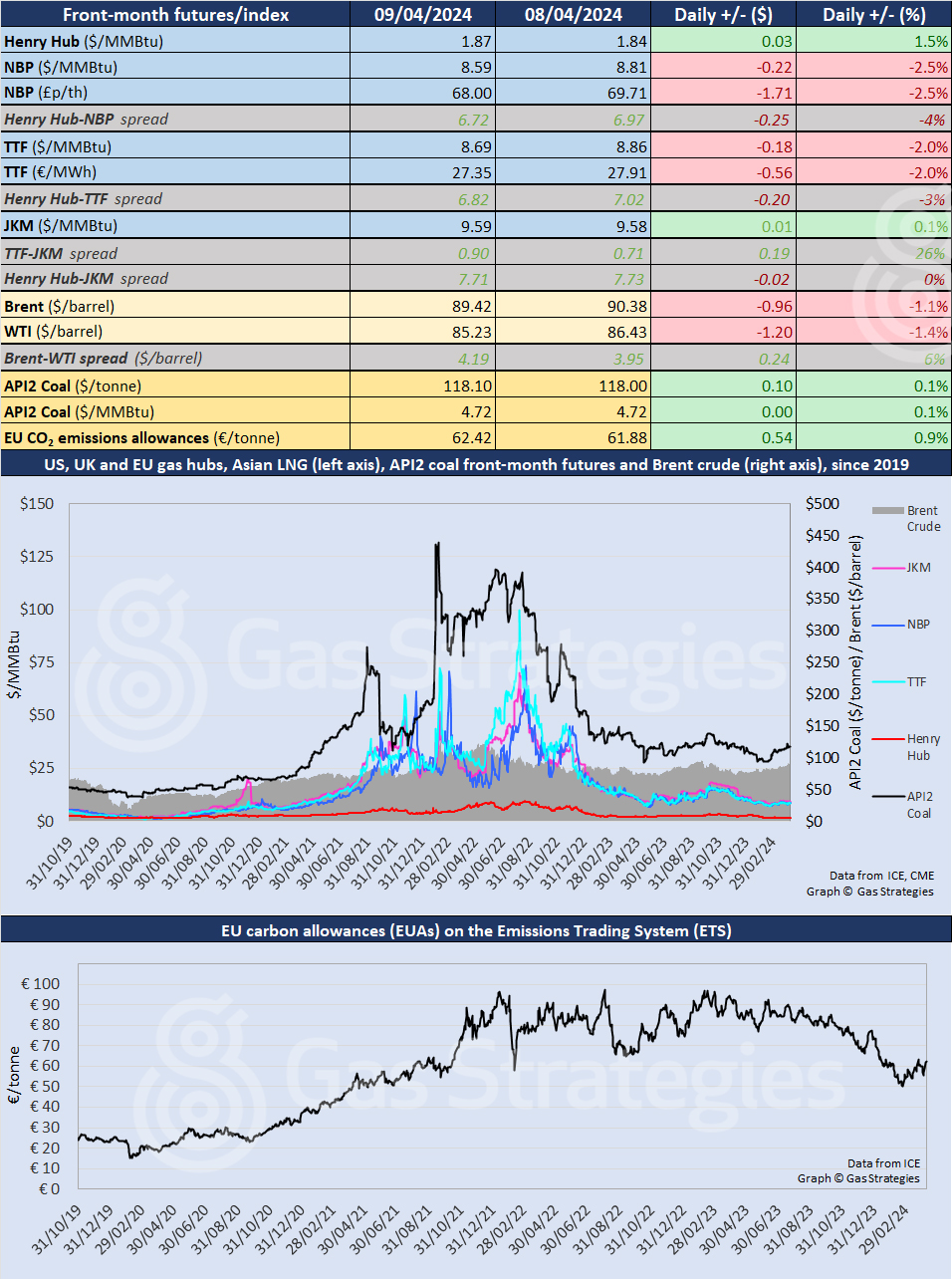

European natural gas futures ended their rally of three consecutive rises on Tuesday, returning to the sawtooth pattern that has characterised trading over recent weeks. Oil prices, meanwhile, continued to fall, with Brent closing below USD 90/barrel. Price movements were muted in other markets.

In Continental Europe, the May TTF contract closed down 2.0%, from USD 8.86/MMBtu on Monday to USD 8.69/MMBtu on Tuesday. The fall comes after three rises that pushed the front-month price up by a combined 10.1%, from a closing price of USD 8.05/MMBtu on 3 April.

In the UK, NBP futures did much the same, closing down 2.5%, from USD 8.81/MMBtu on Monday to USD 8.59/MMBtu on Tuesday. The three previous sessions saw the price rise by a combined 11.1%, from USD 7.93/MMBtu.

Gas prices in Europe remain skittish – with daily changes of 5% commonplace – but behind this day-to-day volatility the underlying trend remains flat, with the main drivers priced in, and little new in recent weeks to shift prices to a new level.

That said, last summer and autumn showed that the unexpected is never far away, with prices responding sharply to strikes at LNG facilities in Australia, prolonged maintenance outages in Norway, the onset of the war in Gaza and subsequent Houthi attacks on Red Sea shipping.

Storage starting to fill

For now, natural gas inventories are at record highs, supply remains comfortable and storage facilities are beginning to fill rather than empty. Data from Gas Infrastructure Europe shows that EU storage facilities are 60.6% full, up 2.3% since the start of the month. UK storage is at 44.4%, up 12.7% on a month ago.

In Asia, the JKM LNG price barely budged on Tuesday, up by 0.1% to USD 9.59/MMBtu.

In the US, front-month Henry Hub rose for the third consecutive session, closing up 1.5%, from USD 1.84/MMBtu on Monday to USD 1.87/MMBtu on Tuesday. This takes the price back to where it was earlier in the month.

The Energy Information Administration (EIA) yesterday lowered its forecast for Henry Hub spot prices this year, with the average falling from USD 2.30/MMBtu to USD 2.20/MMBtu, a 5.2% reduction, because of high inventories.

In its short-term energy outlook, the EIA said: “The US winter natural gas withdrawal season ended with 39% more natural gas in storage compared with the five-year average … Despite lower production, we still expect the US will have the most natural gas in storage on record when the winter withdrawal season begins in November.”

Despite this, the EIA’s forecast for the average Henry Hub spot price in 2025 remains at USD 2.90/MMBtu. Dry gas production is expected to average 103 Bcf/d between now and October, down from 104 Bcf/d in the same period of 2023.

Crude oil prices fell for a second consecutive session, with front-month Brent down 1.1%, from USD 90.38/barrel on Monday to USD 89.42/barrel on Tuesday. The return to below USD 90 is contrary to expectations in some quarters that Brent might be on its way to USD 95 or even triple digits.

For its part, the EIA forecasts that Brent will average USD 90/barrel in the second quarter of 2024 and USD 89/barrel over the whole of the year.

European coal prices remained flat on Tuesday, with API2 at USD 4.72/MMBtu, despite the market disruptions caused by the Baltimore bridge accident in the US.

The EIA comments that the closure of the port of Baltimore has caused it to reduce its forecast for coal exports from the US by “more than 30% in April and 20% in May” compared with its March forecasts. Baltimore is the second-largest export hub for coal in the US.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Subscription Benefits

Our three titles – LNG Business Review, Gas Matters and Gas Matters Today – tackle the biggest questions on global developments and major industry trends through a mixture of news, profiles and analysis.

LNG Business Review

LNG Business Review seeks to discover new truths about today’s LNG industry. It strives to widen market players’ scope of reference by actively engaging with events, offering new perspectives while challenging existing ones, and never shying away from being a platform for debate.

Gas Matters

Gas Matters digs deep into the stories of today, keeping the challenges of tomorrow in its sights. Weekly features and interviews, informed by unrivalled in-house expertise, offer a fresh perspective on events as well as thoughtful, intelligent analysis that dares to challenge the status quo.

Gas Matters Today

Gas Matters Today cuts through the bluster of online news and views to offer trustworthy, informed perspectives on major events shaping the gas and LNG industries. This daily news service provides unparalleled insight by drawing on the collective knowledge of in-house reporters, specialist contributors and extensive archive to go beyond the headlines, making it essential reading for gas industry professionals.