Crude oil prices continued their rally on Wednesday amid geopolitical uncertainties and other bullish factors, with Brent settling just below USD 90/barrel – a threshold some commentators expect to see breached, possibly as soon as today. It was almost breached in intra-day trading yesterday.

The political impacts of this week’s events in the Middle East – Monday’s air strike on an Iranian embassy compound in Damascus and an Israeli drone attack on a convoy of foreign aid workers in Gaza – continued to reverberate. Iran has blamed Israel for the Damascus attack, vowing revenge.

Meanwhile, as the six-month anniversary of the 7 October Hamas attacks on Israelis looms, Israel finds itself more isolated than ever in its war in Gaza. Pressure is building in the UK to suspend arms exports to Israel.

US and UK leaders are furious over the deaths of seven aid workers, three of them UK nationals and one a US national, and question marks hang over what will now happen to desperately needed aid efforts.

Other bullish factors driving oil prices included yesterday’s review meeting of OPEC+ members and US inventory data.

Russia and Saudi Arabia confirmed their unilateral curbs would continue until at least June and the cartel is stepping up compliance pressure on some of its members.

In a statement after the meeting, the Joint Ministerial Monitoring Committee (JMMC) said: “Participating countries with outstanding overproduced volumes for the months of January, February and March 2024 will submit their detailed compensation plans to the OPEC Secretariat by 30 April 2024.”

The next meeting of the JMMC will be on 1 June.

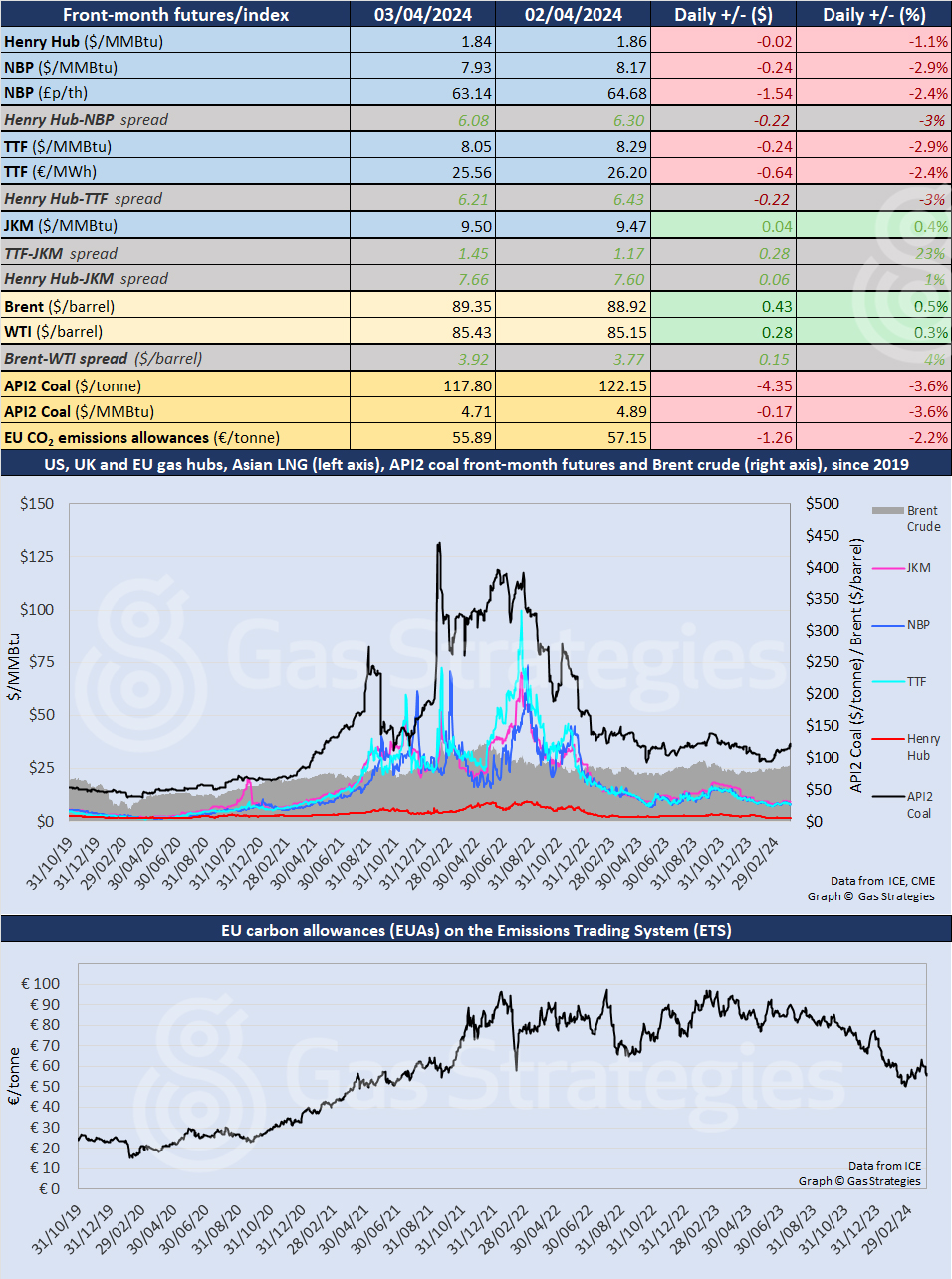

Brent crude rose to within a cent of USD 90/barrel on Wednesday before falling back to close 0.5% up at USD 89.35/barrel, the highest front-month close since October, in the wake of the 7 October atrocities. WTI settled 0.3% up at USD 85.43/barrel.

European natural gas futures fell again and prices remain roughly where they were a month ago, with the main driving factors – high storage levels and warming weather – priced in.

In continental Europe, TTF was down 2.9%, from USD 8.29/MMBtu on Tuesday to USD 8.05/MMBtu on Wednesday, while the UK NBP fell 2.9%, from USD 8.17/MMBtu to USD 7.93/MMBtu.

The Asian LKM LNG price remains rangebound, up 0.4%, from USD 9.47/MMBtu on Tuesday to USD 9.50/MMBtu on Wednesday. The contract has traded within a range of USD 9.40-9.58/MMBtu for over a week. The TTF-JKM spread widened again to USD 1.45/MMBtu, making Asia a significantly more attractive market than Europe, subject to shipping costs.

In the US, Henry Hub ended its recent rally, ahead of gas storage data due out later today. Front-month Henry Hub was down 1.1%, from USD 1.86/MMBtu on Tuesday to USD 1.84/MMBtu on Wednesday.

European coal prices ended the rally sparked by last week’s Baltimore bridge accident in the US. API2 was down 3.6%, from USD 4.89/MMBtu on Tuesday to USD 4.71/MMBtu on Wednesday.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.