European natural gas futures rocketed up to close at their highest levels in three months on Thursday amid an intensification of Russian aggression against energy infrastructure in Ukraine and increasing political pressure to ban gas and LNG imports from Russia.

US gas prices moved sharply in the opposite direction as weekly government storage data showed a larger than expected injection.

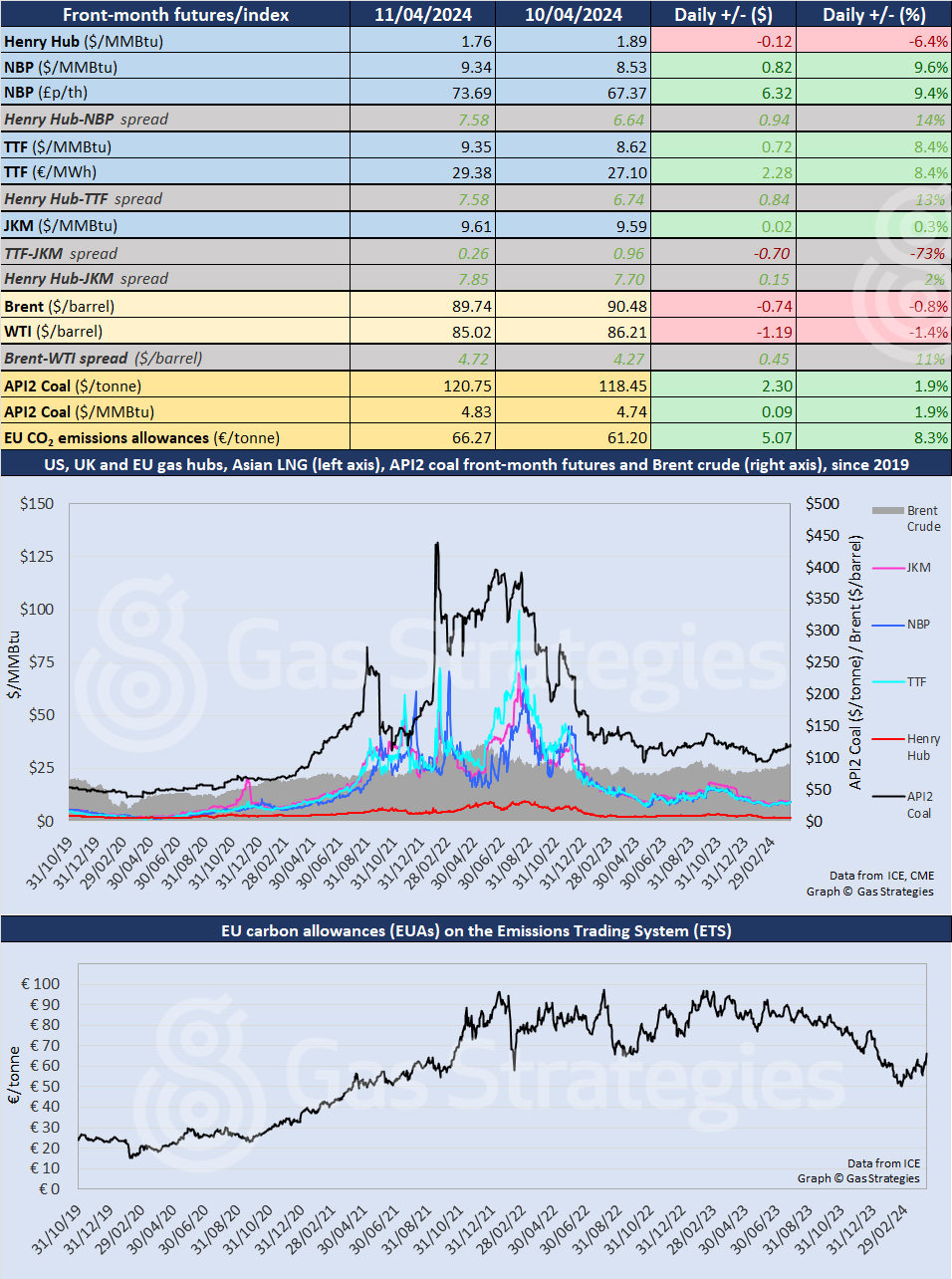

In continental Europe, the May TTF contract climbed by 8.4%, from USD 8.62/MMBtu on Wednesday to USD 9.35/MMBtu on Thursday, the highest front-month close since 12 January. A further rise on Friday morning saw the contract trading above EUR 30/MWh in local currency terms.

In the UK, NBP futures closed up 9.6%, from USD 8.53/MMBtu on Wednesday to USD 9.34/MMBtu on Thursday, putting NBP close to parity with TTF. Its trajectory on Friday morning was similar to that of TTF.

The European parliament yesterday voted to approve a new directive and regulation on the gas and hydrogen markets that includes provisions to enable EU member countries to restrict imports from Russia.

Lead MEP on the regulation, Jerzy Buzek, said: “We have introduced a legal option for EU countries to stop importing gas from Russia if there is a security threat, which gives them a tool to phase out our dependence on a dangerous monopolist.”

Both texts will now have to be formally adopted by Council before publication in the Official Journal.

In Asia, the JKM LNG price maintained its run of stability, edging up 0.3% to USD 9.61/MMBtu. Combined with the change in TTF, this saw the TTF-JKM spread collapse from just under a dollar to USD 0.26/MMBtu.

US storage builds despite output curbs

In the US, front-month Henry Hub closed down 6.4%, from USD 1.89/MMBtu on Wednesday to USD 1.76/MMBtu on Thursday, as traders responded to the ramifications of the latest data on gas storage.

In yesterday’s weekly storage report, the Energy Information Administration (EIA) estimated working gas in storage at 2,283 Bcf as of 5 April, up 24 Bcf from the previous week and above the five-year historical range. Stocks were 435 Bcf higher year-on-year and 633 Bcf – or 38% – above the five-year average of 1,650 Bcf for this time of year.

The storage injection comes despite falling output as producers curb production in response to low prices, with mild weather a driving factor. Storage in the Lower 48 states remains well outside the five-year maximum-minimum range, though the gap is slowly narrowing. The latest producer to announce output curbs is APA Corporation.

The Brent crude front-month contract continued its oscillations around USD 90/barrel, falling by 0.8%, from USD 90.48/barrel on Wednesday to USD 89.74/barrel on Thursday. WTI was down 1.4%, from USD 86.21/barrel to USD 85.02/barrel.

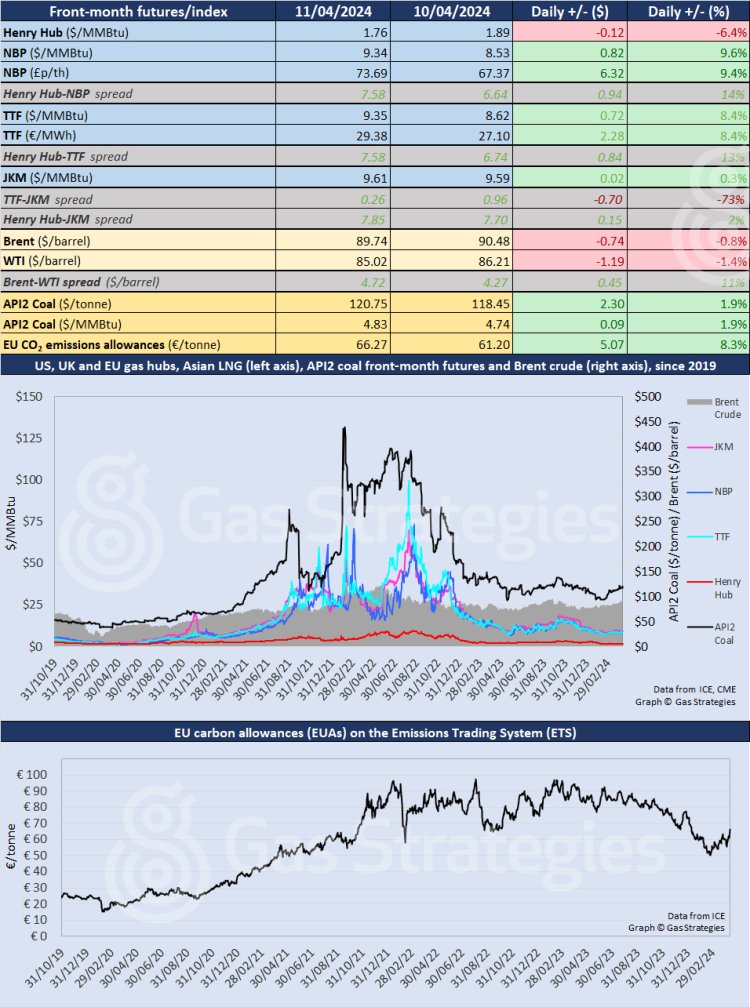

European carbon prices took their cue from natural gas, with EU emissions allowances up 8.3%, from EUR 61.20/tonne to EUR 66.27/tonne.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.