Energy and carbon prices rose across the board on Friday as anticipation built of an imminent and unprecedented direct attack on Israel by Iran. However, there has been no sign of panic on markets – then or since – despite the attack materialising, in the form predicted by US intelligence sources, late on Saturday.

More than 300 drones and ballistic and cruise missiles were directed at Israel but most were shot down by the military forces of Israel and its allies – mainly the US and the UK – with some destroyed by Jordan as they crossed its airspace.

Iran claims it achieved its objectives but the consensus among defence analysts is that the outcome must have been a disappointment – and a dent to Iran’s military credibility.

Nevertheless, there is universal agreement that Saturday’s attack marks a dangerous new phase in the geopolitics of the Middle East, with strenuous diplomatic efforts under way to prevent a wider conflagration.

Much now depends on what Israel chooses to do next. Its allies are urging it to “take the win” and stay its hand. The US, for its part, has stressed it will not participate in any retaliatory strike.

Little impact on Israel or markets

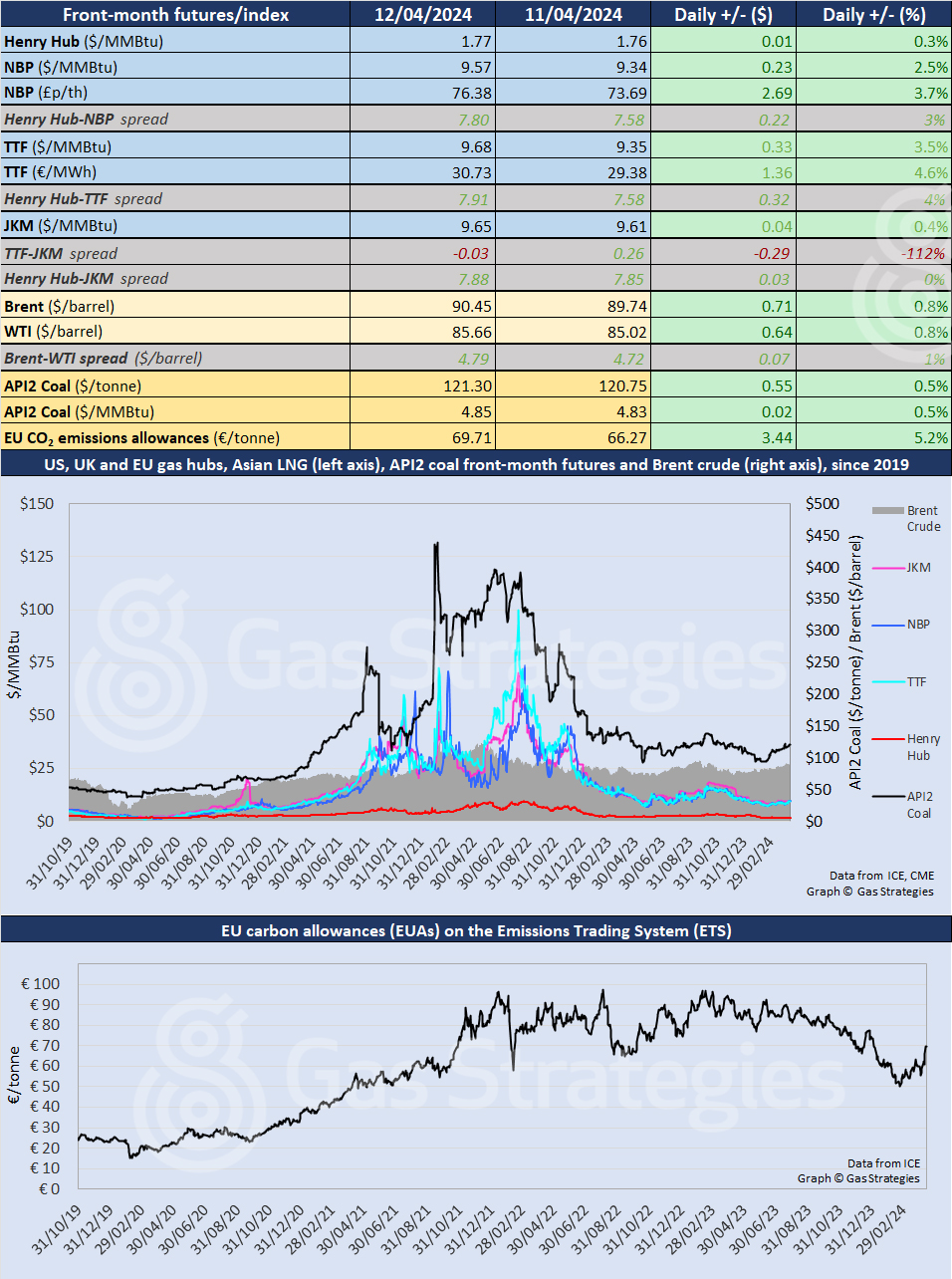

Brent crude oil futures closed up 0.8% on Friday, from USD 89.74/barrel on Thursday to USD 90.45/barrel. Significantly, the price was back below USD 90/barrel on Monday morning.

Similarly, WTI also rose by 0.8%, from USD 85.02/barrel to USD 85.66/barrel but was down below USD 85/barrel in early trading on Monday.

The rise in European natural gas prices was well within recent day-to-day volatility.

In Continental Europe, the May TTF contract climbed by 3.5%, from USD 9.35/MMBtu on Thursday to USD 9.68/MMBtu on Thursday.

Currency effects were significant. In local currency the price was up 4.6% to EUR 30.73/MWh, the highest front-month close since the first half of January. The price was back below EUR 30/MWh on Monday morning.

In the UK, NBP futures closed up 2.5%, from USD 9.34/MMBtu on Thursday to USD 9.57/MMBtu on Friday. In local currency terms the rise was 3.7% to 76.38 p/therm. NBP’s trajectory on Friday morning was similar to that of TTF – downwards.

In Asia, the JKM LNG price was little moved, edging up 0.4% to USD 9.65/MMBtu.

In the US, front-month Henry Hub closed up 0.3% to USD 1.77/MMBtu.

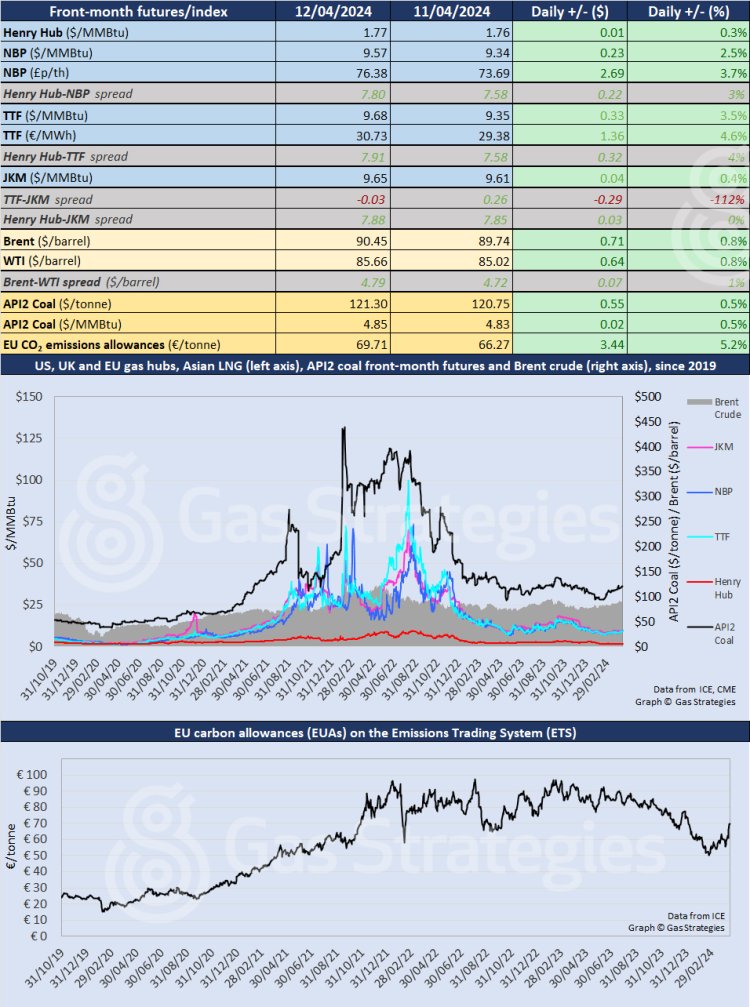

European carbon prices showed the largest rise of the day on Friday, up 5.2% from EUR 66.27/tonne on Thursday to EUR 69.71/tonne.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.