Crude prices slipped on Tuesday, however oil was rallying on Wednesday morning amid expectations that the Organization of the Petroleum Exporting Countries (OPEC) and its allies, a group collectively known as OPEC+, will agree to continue production cuts into May.

Front-month Brent and WTI fell by 1.3% and 1.6% respectively on Tuesday, with prices sliding as transits in the Suez Canal resumed on Monday evening after the Ever Given container vessel was successfully freed from the waterway.

However, prices were ticking higher on Wednesday morning amid expectations that the OPEC+ alliance will agree to sustain production curbs into May, when the alliance meets on Thursday.

OPEC+ surprised the market earlier this month when it announce it would continue with production cuts in April. Market observers had widely expected that OPEC+ would agree to increase production in light of higher prices, however the oil alliance voted against a collective 500,000 barrels/d increase in production starting in April.

With the demand outlook looking bearish due to spiralling Covid-19 cases – particularly in Europe – and the oil price bull run having stalled, OPEC+ is widely expected to show restraint again heading into May.

Under the existing production cuts, OPEC+ has cut ~7 million barrels/d, with Saudi Arabia having voluntarily cut its production by 1 million barrels/d.

Supporting the need for a supply-side response is growing US crude inventories. On Tuesday, the American Petroleum Institute said US oil storage increased by 3.9 million barrels in the week ending 26 March, with the figure significantly higher than the expected 100,000 barrel-build expected by analysts polled by Reuters.

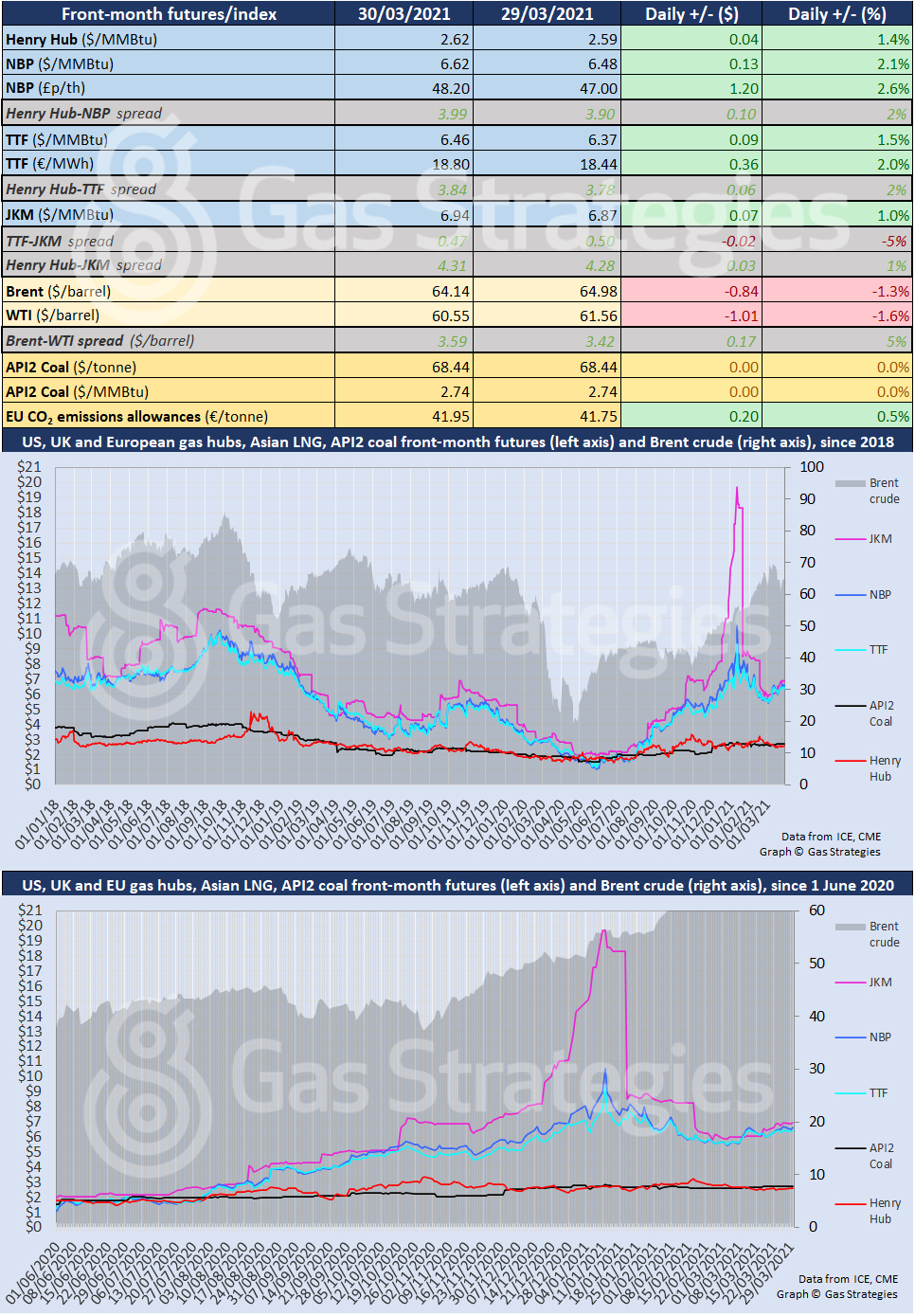

Whilst crude fell, gas rallied on Tuesday. The front-month UK NBP and Dutch TTF contracts recorded gains of 2.1% and 1.5%, respectively.

The month-ahead JKM contact also rallied, increasing by 1% to settle at USD 6.94/MMBtu – its highest close since 17 February.

US gas benchmark Henry Hub continued to rally, increasing by 1.1% to close in the USD 2.6/MMBtu range for the first time since 12 March.

The European carbon price continued to rally, recording a 0.5% gain to close at EUR 41.95/tonne.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Subscription Benefits

Our three titles – LNG Business Review, Gas Matters and Gas Matters Today – tackle the biggest questions on global developments and major industry trends through a mixture of news, profiles and analysis.

LNG Business Review

LNG Business Review seeks to discover new truths about today’s LNG industry. It strives to widen market players’ scope of reference by actively engaging with events, offering new perspectives while challenging existing ones, and never shying away from being a platform for debate.

Gas Matters

Gas Matters digs deep into the stories of today, keeping the challenges of tomorrow in its sights. Weekly features and interviews, informed by unrivalled in-house expertise, offer a fresh perspective on events as well as thoughtful, intelligent analysis that dares to challenge the status quo.

Gas Matters Today

Gas Matters Today cuts through the bluster of online news and views to offer trustworthy, informed perspectives on major events shaping the gas and LNG industries. This daily news service provides unparalleled insight by drawing on the collective knowledge of in-house reporters, specialist contributors and extensive archive to go beyond the headlines, making it essential reading for gas industry professionals.

Related Stories

-

30Mar2021

30Mar2021Pricewatch | 30 Mar 2021 | Gas Matters Today

29Mar2021

29Mar2021Pricewatch | 29 Mar 2021 | Gas Matters Today

26Mar2021

26Mar2021Pricewatch | 26 Mar 2021 | Gas Matters Today