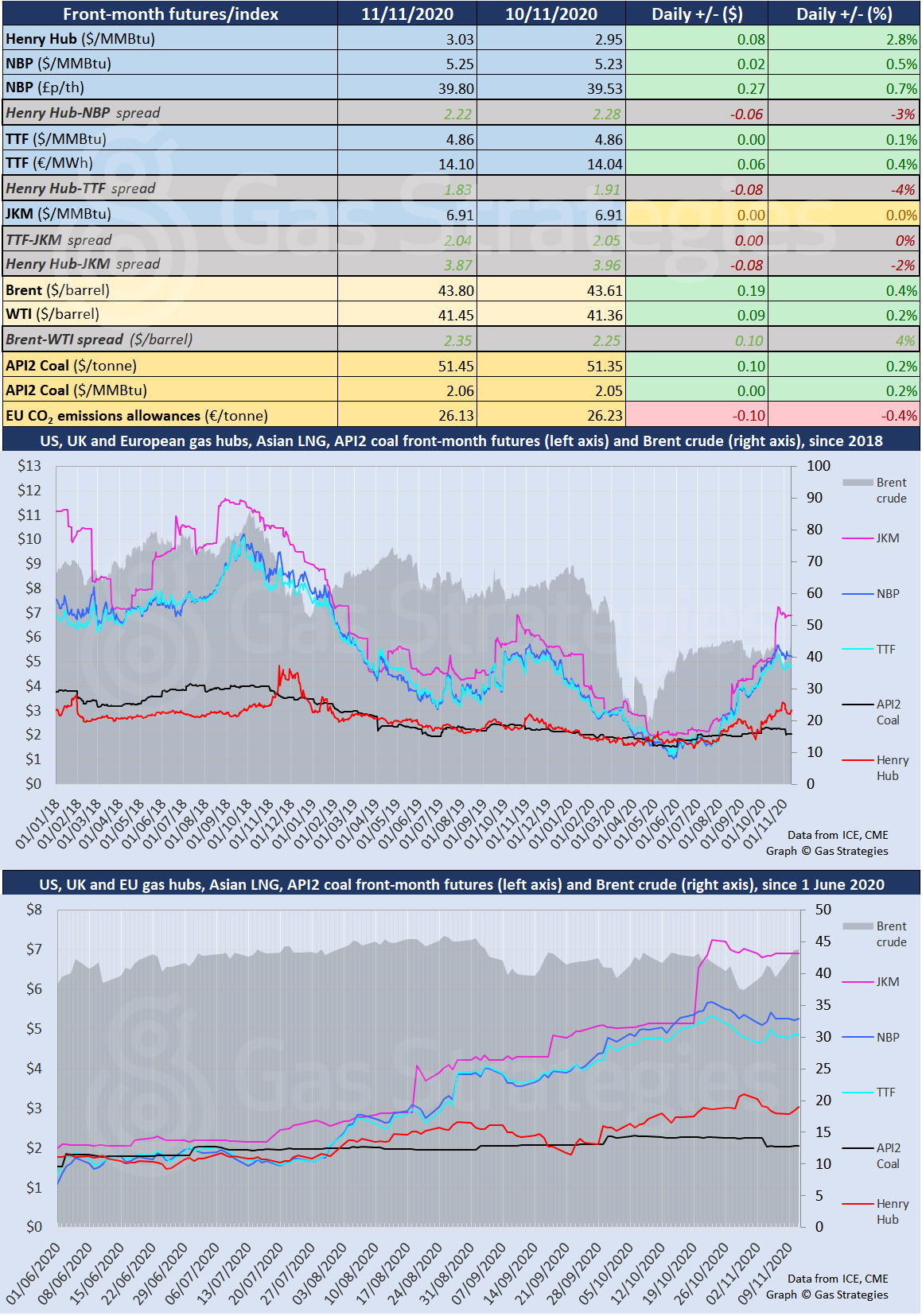

The euphoria over Pfizer’s promising Sars-Cov-2 vaccine began to peter out on Wednesday, as Brent and WTI rose just 0.4% and 0.2% in the session to close at USD 43.80/barrel and USD 41.45/barrel, respectively – indicating an imminent end to the three-day rally. Yesterday’s marginal gains were assisted by encouraging US oil stocks data and hopes that OPEC+ nations would agree to new supply cuts when they next meet on 1 December, but that sentiment sourced this morning when the International Energy Agency cut its estimates for global oil demand for the remainder of the year and into early 2021, citing soaring Covid-19 cases, tightening lockdowns and travel restrictions.

US natural gas benchmark Henry Hub’s front month contract built on Tuesday’s gains to rise 2.8% yesterday, closing the session at USD 3.03/MMBtu, after US storage data revealed a quicker-than-expected drawdown of stockpiled gas.

European gas hubs UK NBP and Dutch TTF notched up small gains yesterday’s session. CME’s December-dated JKM futures contract was again unchanged at USD 6.91/MMBtu. The European carbon price fell a bit further, as month-ahead ETS allowance (EUA) futures lost 0.4% to close at EUR 26.13/tonne.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights reserved.