European gas prices hit a four-month high on Wednesday amid strong demand and tightening supply, with the rally expected to continue after Elengy announced on Tuesday evening that the Montoir LNG terminal in France is likely to be out of action for the remainder of May.

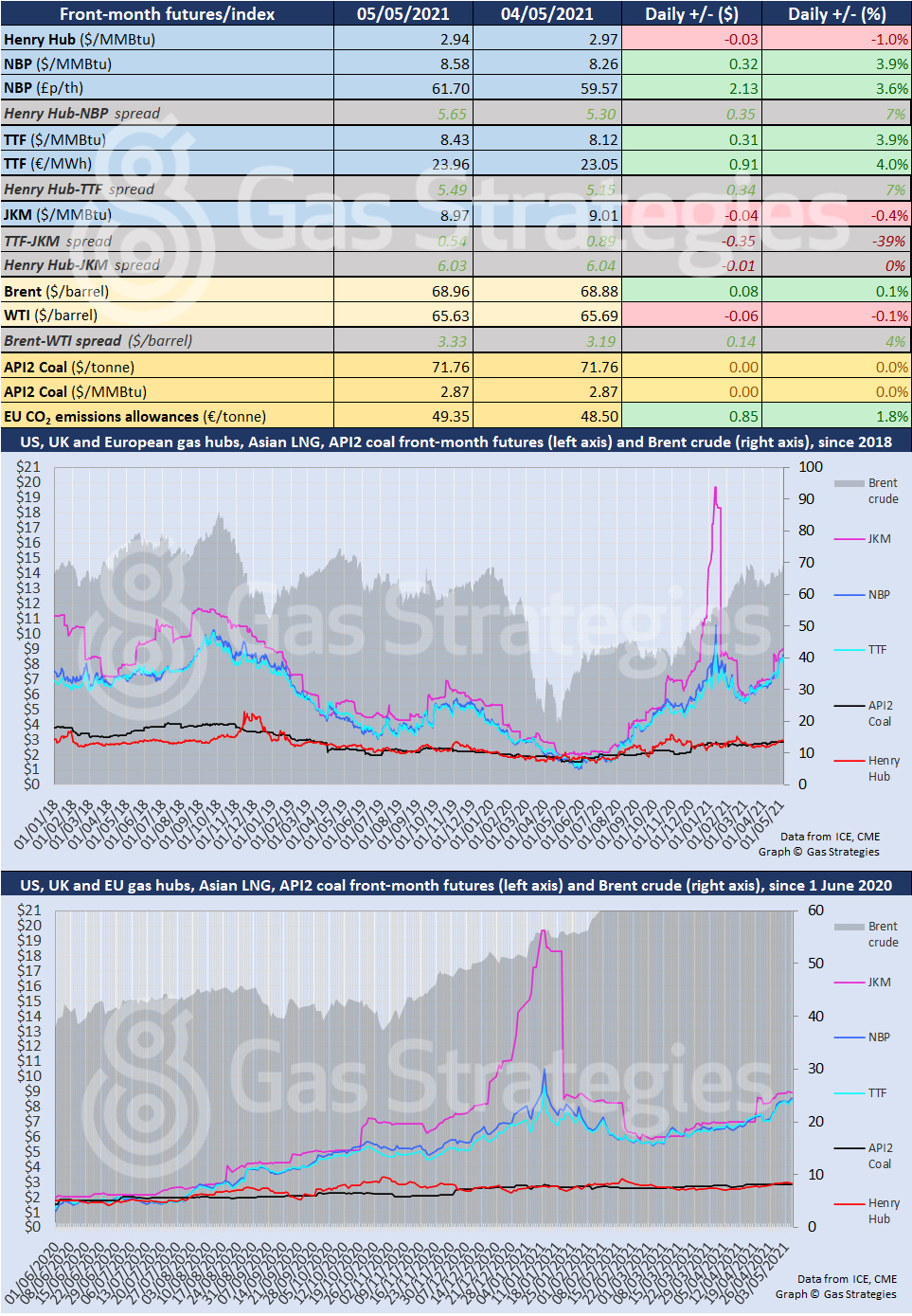

The front-month NBP and TTF contracts recorded gains of 3.9% on Wednesday amid bullish demand and bearish supply, with NBP settling at 8.58/MMBtu and TTF closing at 8.43/MMBtu.

The rally continued on Wednesday morning as the market digested Elengy’s announcement regarding Montoir LNG. A pipeline problem at the terminal was detected on Tuesday, forcing the facility to halt regasficiation operations.

The terminal is expected to receive no more cargoes in May, Elengy said, with Montoir having been expected to take seven cargoes previously. Elengy said it is aiming to resume operations as soon as possible, however the terminal operator has not set restart date.

“The outage comes at a time when European storage inventories are low, and French injections are expected to be already weak due to strong demand on cool weather and supported gas-to-power. The lack of send out will further dent efforts to fill French storage levels during May,” on trade source told Gas Matters Today.

Three vessels had confirmed destinations as Montoir before Elengy’s announcement yesterday, with two vessels en route from Nigeria and one from Corpus Christi.

At least two of the three cargoes will be diverted elsewhere in north-west Europe given the availability of slots and costs of re-routing, the source suggests.

As for the cargoes that were meant to arrive at Montoir in late May – they have not loaded yet and are most likely to be diverted to Asia to take advantage of the price premium, the trade source suggests.

The gas price rally helped lift the European carbon price to a record high on Wednesday, with the June-dated contract settling at EUR 49.35/tonne. The benchmark December 2021 contract closed at a record high of EUR 49.45/tonne. The carbon price also rallied on news that Germany is planning to fast-track plans to become carbon neutral in 2045, five years earlier than the current target.

Whilst the Montoir news pushed European gas prices higher, the outage may apply downward pressure to Asian LNG marker JKM, with Asia currently mopping up cargoes diverted from India – where gas demand has fallen due to spiralling Covid-19 cases.

The front-month JKM contract fell by 0.4% on Wednesday to settle at USD 8.97/MMBtu. The fall, coupled with the rally by the European gas markers, cut JKM’s premium over TTF to USD 0.54/MMBtu.

In the US, gas benchmark Henry Hub slipped by 1% amid a minor reduction in exports and increasing production. The front-month contract settled at USD 2.94/MMBtu.

Crude prices diverged on Wednesday, with Brent recording a minor gain of 0.1% and WTI falling by 0.1%. The US crude benchmark fell due to news of domestic gasoline inventories increasing for a fifth consecutive week. Gains by the crude markers remain capped by spiralling Covid-19 cases in major oil consuming nations.

The front-month Brent contract remained in the USD 68/barrel range, with WTI glued to the USD 65/barrel range.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.