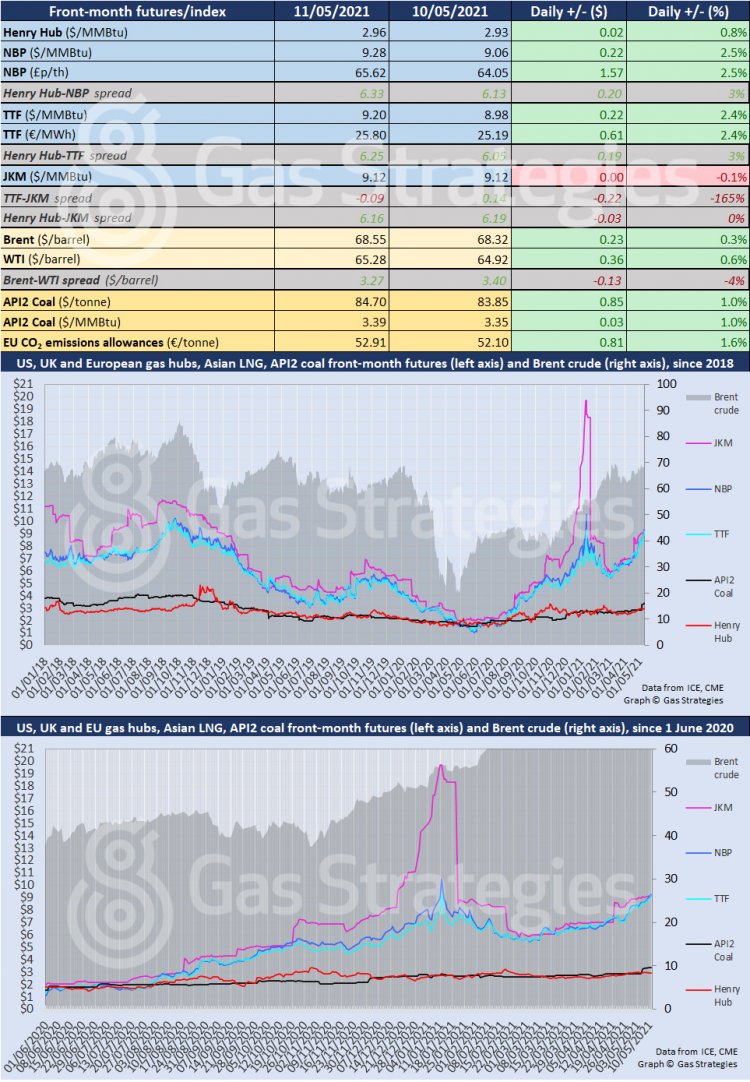

European gas prices hit a fresh four-month high on Tuesday, lifted by tight supply, strong demand and the soaring European carbon price. The rally by the European gas benchmarks saw TTF and NBP take a premium over Asian LNG marker JKM.

The front-month TTF and NBP contracts rallied by ~2.5% on Tuesday, with both markers settling in the USD 9.20/MMBtu range.

The rally was prompted by the expectation of colder weather in the coming weeks, which is expected to lift gas demand, with supply looking tight – in part due to an unplanned outage at the Montoir LNG terminal in France.

Europe’s gas storage is in need of replenishing after a cold winter, with inventories ~32 Bcm full as of Monday, a level 13 Bcm below the five-year average, according to EnergyScan. The weak storage levels are driving prices along the curve, with year-ahead TTF prices hitting EUR 22/MWh this week – the first time that has occurred since late 2018, according to EnergyScan.

The unabating rally by the European carbon price also helped lift TTF and NBP, with the June-dated EUA contract settling at a record high of EUR 52.91/tonne on Tuesday. As for the benchmark December 2021 contract, it closed at EUR 53.04/tonne yesterday.

Strong carbon and gas, coupled with tight supply, has helped lift the price of coal in Europe, with the AP12 price hitting its highest level since January 2019 on Tuesday. The front-month AP12 contract settled at the equivalent of USD 3.39/MMBtu.

The rally by the European markers, coupled with a minor loss by JKM, saw the Asian LNG marker lose its premium over TTF and NBP. The front-month JKM contract fell by 0.1% on Tuesday but remained at USD 9.12/MMBtu – a figure USD 0.16/MMBtu lower than NBP and USD 0.09/MMBtu lower than TTF.

In the US, gas benchmark Henry Hub recorded a 0.8% gain to close at USD 2.96/MMBtu.

Crude prices continued to tick higher on Tuesday, supported by the ongoing outage on the Colonial Pipeline – the US’ largest refined products pipeline system – due to a cyberattack.

Colonial Pipeline announced on Monday that it expects the major fuels artery to return to service by the end of the week.

The front-month Brent contract remained in the USD 68/barrel range after rallying by 0.3%, with WTI settling in the USD 65/barrel range after rallying by 0.6%.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.