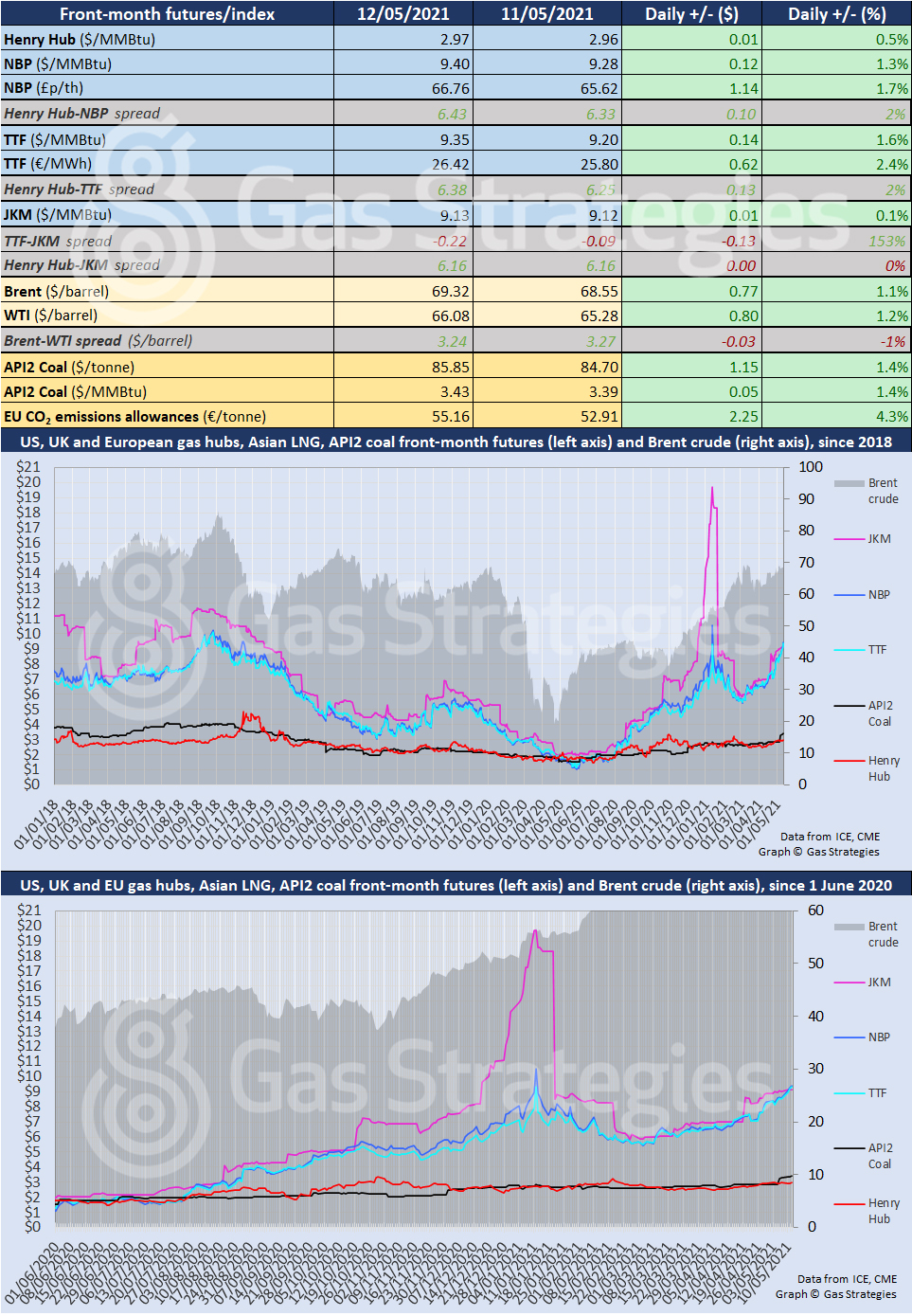

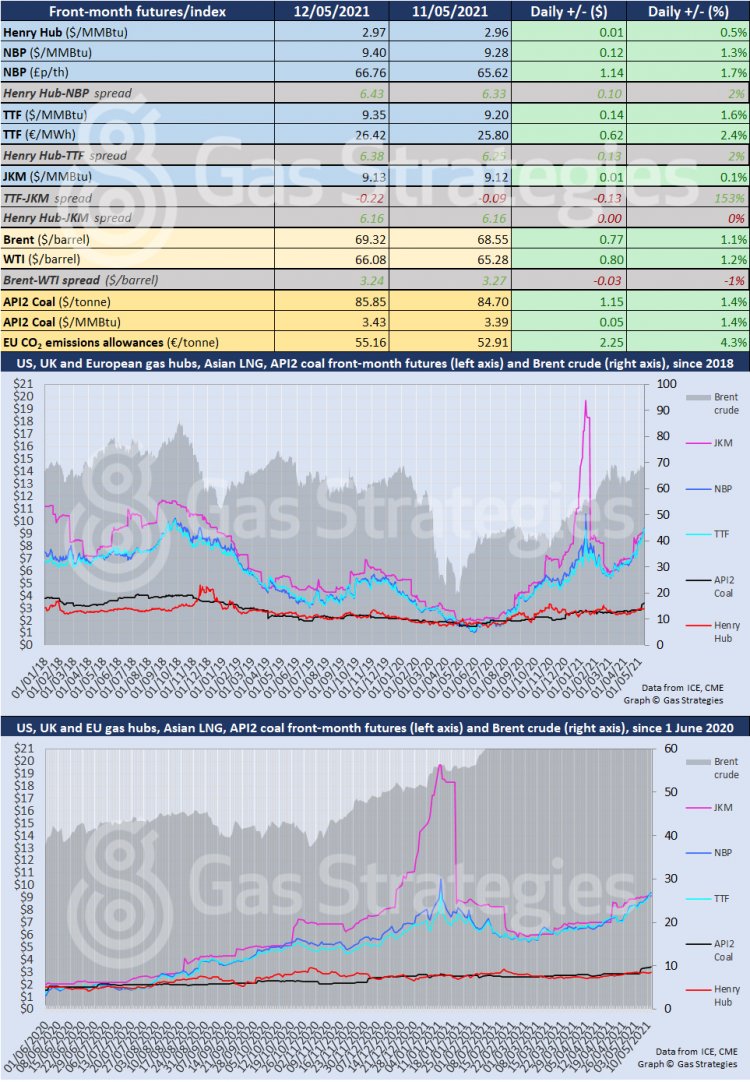

The European carbon price surged by EUR 2.25/tonne on Wednesday to hit a fresh record high, with the rally helping push European gas and coal prices higher.

The bull run by the European carbon price shows no sign of slowing, with the June-dated EUA contract settling at a fresh record high of EUR 55.16/tonne on Wednesday. As for the benchmark December 2021 contract, it closed at EUR 55.32/tonne yesterday.

The rally is being driven by multiple factors, including growing interest by investors – with many banking on reforms to the EU ETS that will tighten the cap on emissions and drive prices even higher. The European Commission will in July take proposals to tighten the market in line with the recently-agreed target of a 55% reduction in emissions from 1990 levels by 2030.

The surging carbon price has helped lift gas and coal prices, with European gas markers TTF and NBP hitting fresh four-month highs on Wednesday. The front-month NBP price rallied by 1.7% to settle at USD 9.40 on Wednesday, with TTF up 1.6% to close at USD 9.35/MMBtu.

Tight supply and strong demand have also helped lift European gas and coal. The front-month AP12 contract settled at the equivalent of USD 3.43/MMBtu on Wednesday – its highest since January 2019.

The rally by the European gas markers helped push Asian LNG marker JKM higher, with the front-month contract recording a marginal gain to close at USD 9.13/MMBtu. The gain was not enough close the gap on the European markers, which extended their premium over JKM on Wednesday. TTF now holds a USD 0.22/MMBtu premium over JKM, with NBP’s premium over the Asian LNG marker standing at USD 0.27/MMBtu.

In the US, gas benchmark Henry Hub continued to rally, recording a 0.5% gain to close at USD 2.97/MMBtu.

Crude prices continued to tick higher on Wednesday, settling at an eight-week high. The front-month Brent and WTI contracts rallied by over 1% to settle at ~USD 69/barrel and ~USD 66/barrel respectively.

Price were lifted by bullish demand-side news, with the US Energy Information Administration (EIA) reporting on Wednesday that US oil exports fell to ~1.8 million barrels/d last week – the lowest level since October 2018. Meanwhile crude storage in the US fell by 0.4 million barrels – however the figure was much lower than the 2.8 million draw down expected, according to Reuters.

The International Energy Agency (IEA) added to the bullish sentiment in its latest monthly oil market report – released this week – which stated that crude demand is already outstripping supply. The Paris-based organisation said that the shortfall will increase even if Iran increases exports.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.