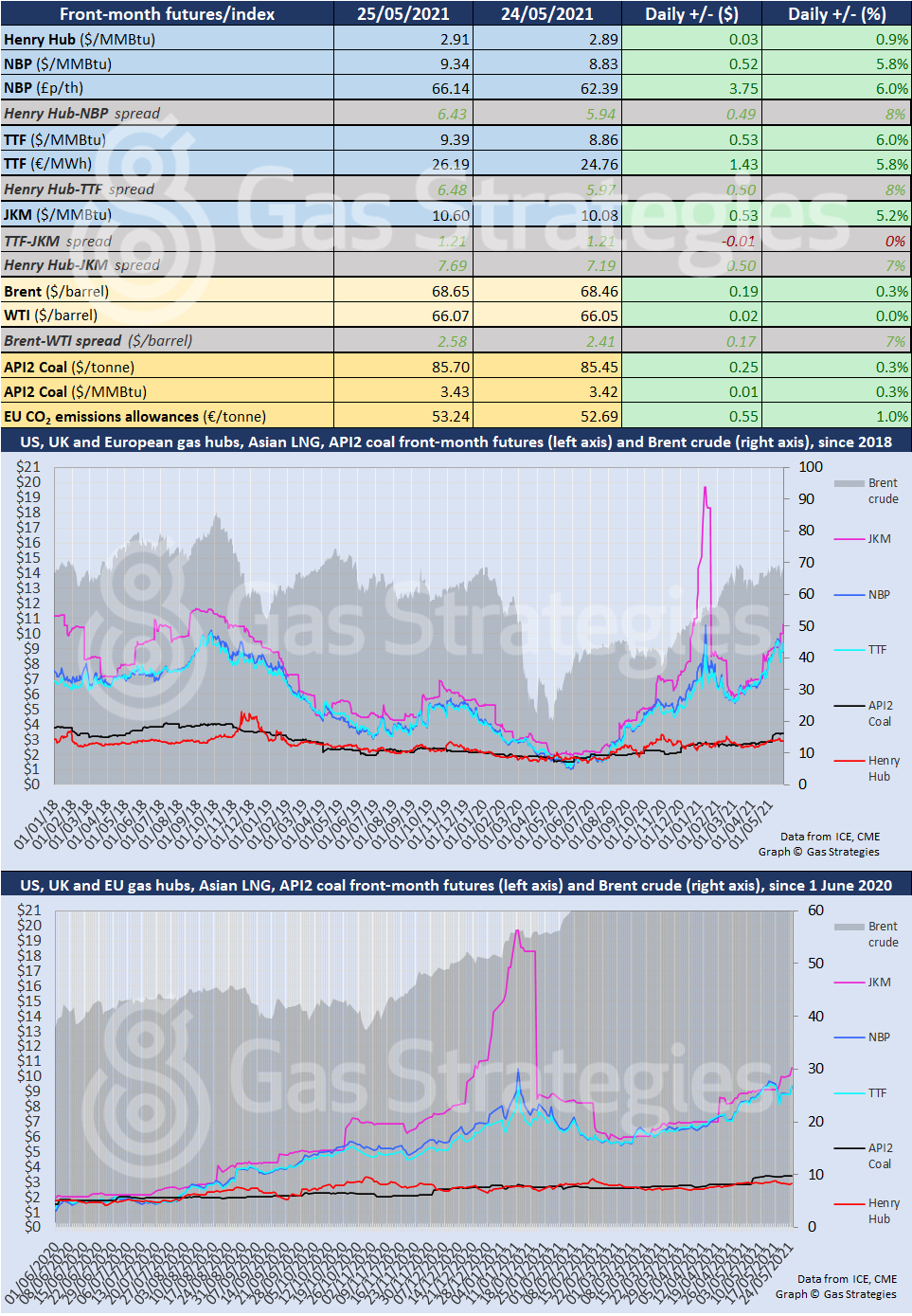

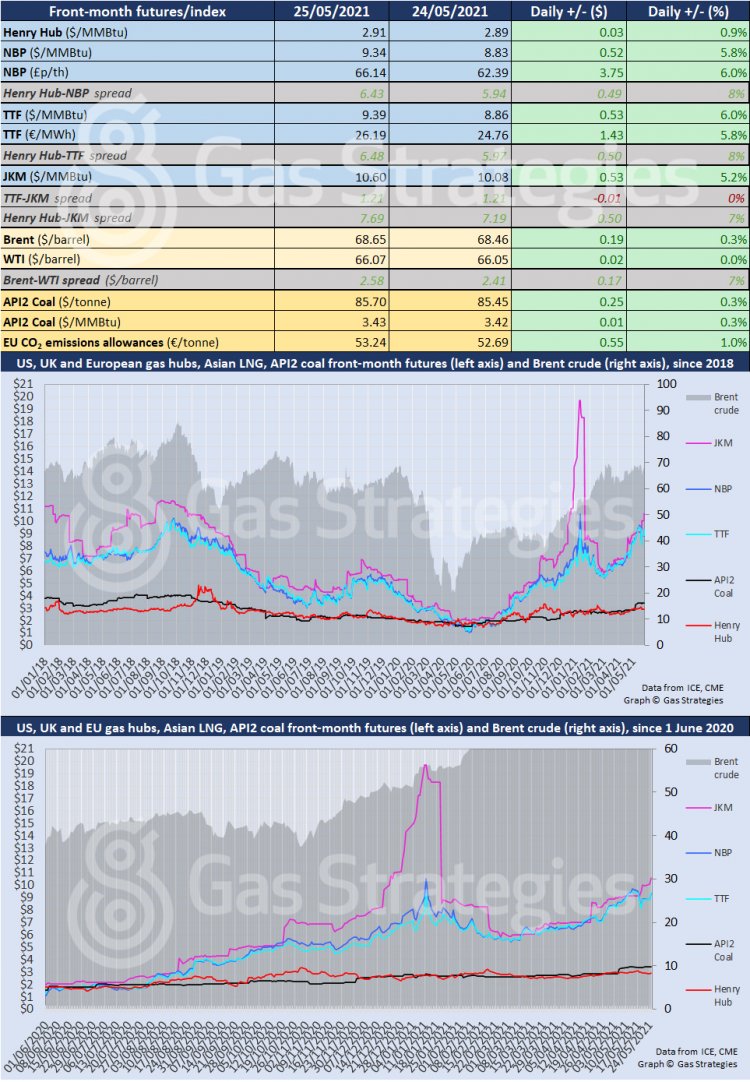

European gas prices surged on Tuesday, with prices lifted by an unplanned outage at an LNG terminal in Europe and by Gazprom’s decision to not book any interruptible transit capacity via Ukraine in June.

The front-month TTF and NBP contracts posted gains of ~6% on Tuesday to settle back in the USD 9/MMBtu range for the first time six days, with prices rallying amid supply concerns and strong demand.

An unplanned outage at the Rovigo LNG terminal in Italy saw LNG import flows tighten, with the outage coinciding with a planned outage at the country’s Panigaglia LNG terminal.

One trade source told Gas Matters Today that the Rovigo terminal may be offline for a week, adding that Italy will probably need to import more gas from north-west Europe in order to offset weaker LNG imports.

Gazprom’s decision to once again not bid for interruptible capacity via Ukraine – in an auction held by Ukrainian transmission system operator GTSO on Tuesday – also helped lift European gas prices, mirroring what happened in April when the Russian firm opted not to bid for interruptible capacity via Ukraine in May.

Following the result of the auction, GTSO’s CEO Sergiy Makogon took to LinkedIn suggesting “Gazprom's policy of artificially restricting supplies to Europe requires the immediate attention of the competent European authorities.”

“Despite high gas prices in the EU, Gazprom did not participate in today's auction for June's gas transit capacity of ~64mcm/day,” Makogon said.

“In other words, Gazprom choose not to supply Europe with 2 Bcm of gas in June, which would've accelerated the replenishment of gas storage facilities,” added Makogon.

The trade source told Gas Matters Today that Europe’s gas demand is very high this week due to unseasonably cold weather, meaning injections into Europe’s depleted gas storage sites remain low, which is helping lift prices.

From next week Europe’s gas demand is expected to fall due to higher temperatures, meaning storage injections should increase, which will weigh on gas prices, the trade source suggests.

In addition to supply and demand dynamics, the strengthening European carbon price also helped lift gas prices, with the front-month EUA price settling at EUR 53.24/tonne, up 1% day-on-day.

The rally by the European gas markers helped lift Asian LNG marker JKM. The front-month JKM contract hit a four-month high, settling at USD 10.6/MMBtu.

In the US, gas benchmark Henry Hub returned to the USD 2.9/MMBtu range after rallying by 0.9%.

As for crude, prices continued to rally, albeit at a much slower pace compared to recent days.

The front-month Brent and WTI contracts posted marginal gains amid expected strong demand in the northern hemisphere due to ongoing lifting of Covid-19 related restrictions.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.