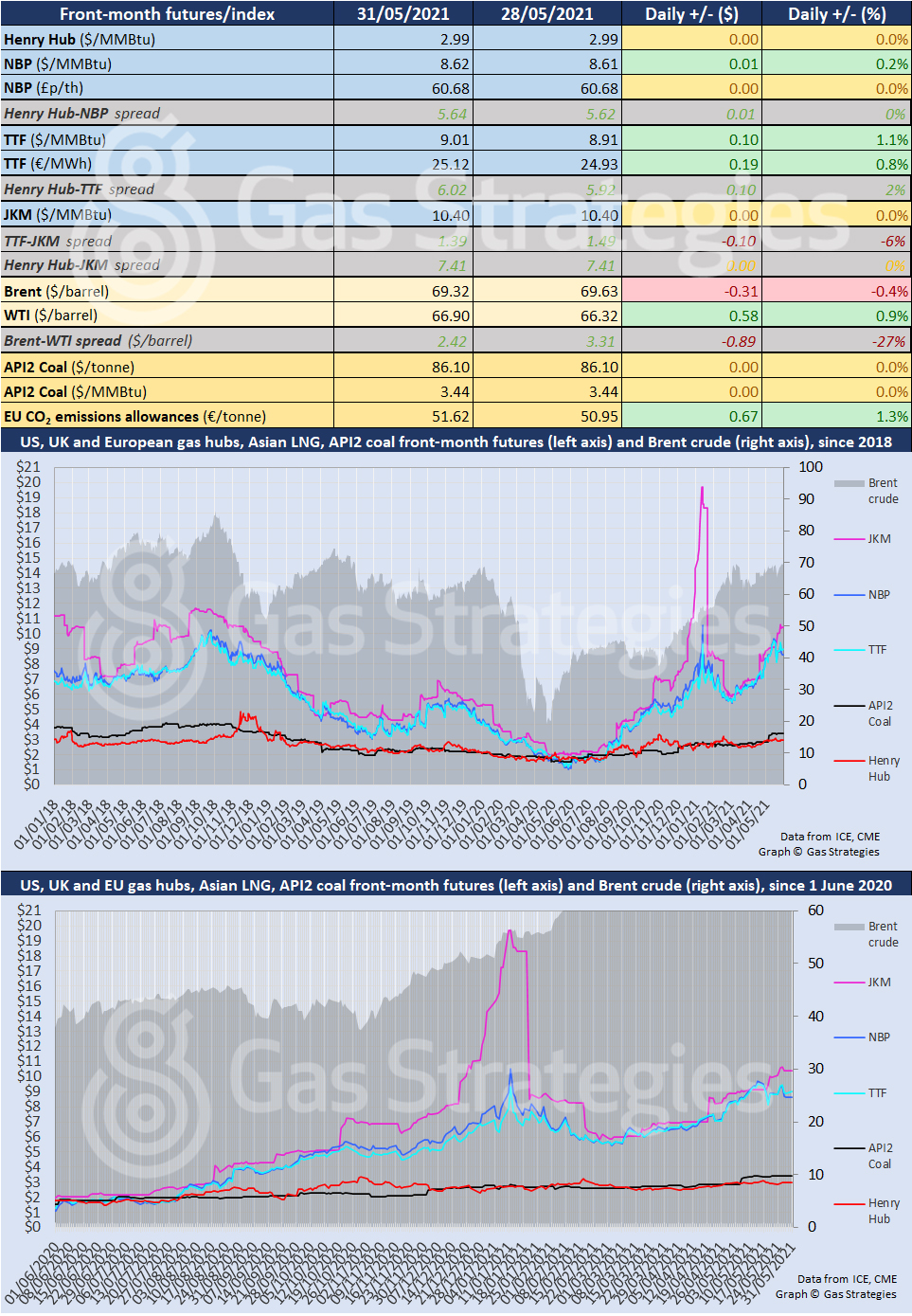

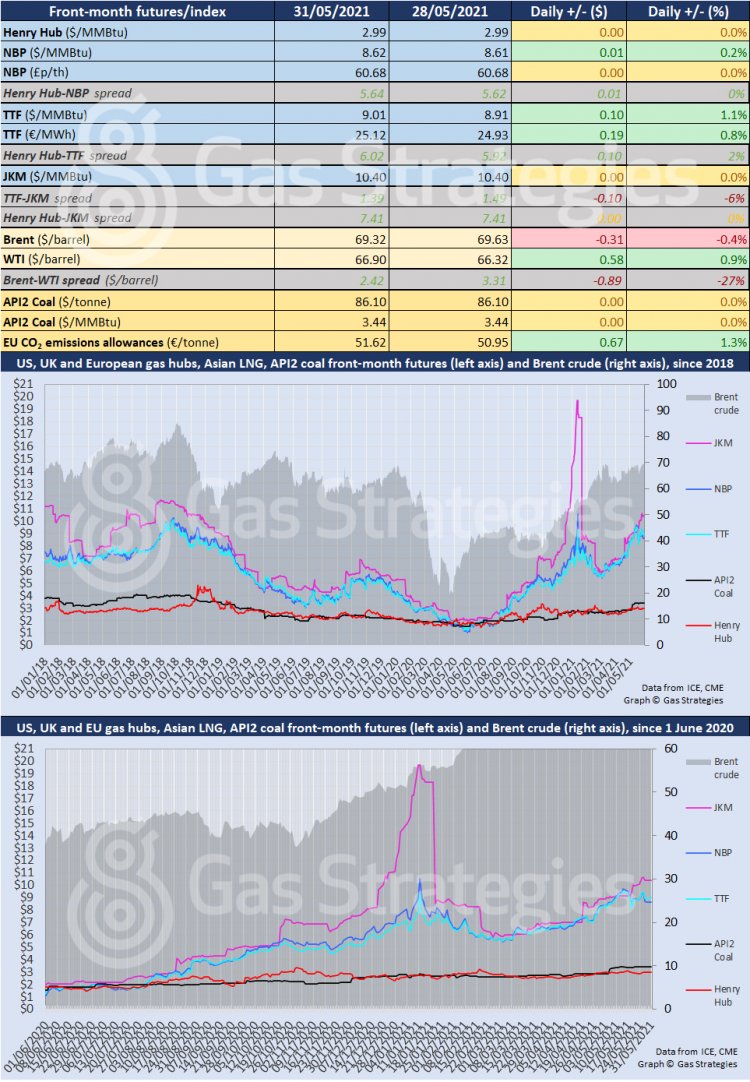

Commodity markets were relatively calm on Monday amid public holidays in the UK and US.

The major movements on Monday were seen on the front-month TTF and European carbon contracts.

TTF rallied by 1.1% to settle in the USD 9/MMBtu range for the first time in three days. Gas prices in Europe have slipped in recent days due to warmer weather which is expected to dent demand, however TTF was rallying on a tight supply outlook amid several LNG plant outages.

The rebound by TTF helped lift the European carbon price, with the June-dated contract settling in the EUR 51/tonne range.

Both JKM and Henry Hub remained unchanged on Monday, however the Asian LNG marker could rally on Tuesday amid the LNG plant outages.

Crude prices continued to rally, with WTI up 0.9% to close at USD 66.90/barrel. The Brent contract rolled over to August on Monday, with the price down 0.4% compared to the final day of trading on the July contract, however the August-dated contract was up ~0.9% day-on-day to start the week.

Brent hit USD 71/barrel during trading on Tuesday morning, with crude rallying on the back of expectations of bullish demand in the US over the summer driving season. Support has also been offered by Chinese data showing that the nation’s factory activity grew at its fastest pace – so far in 2021 – last month.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.