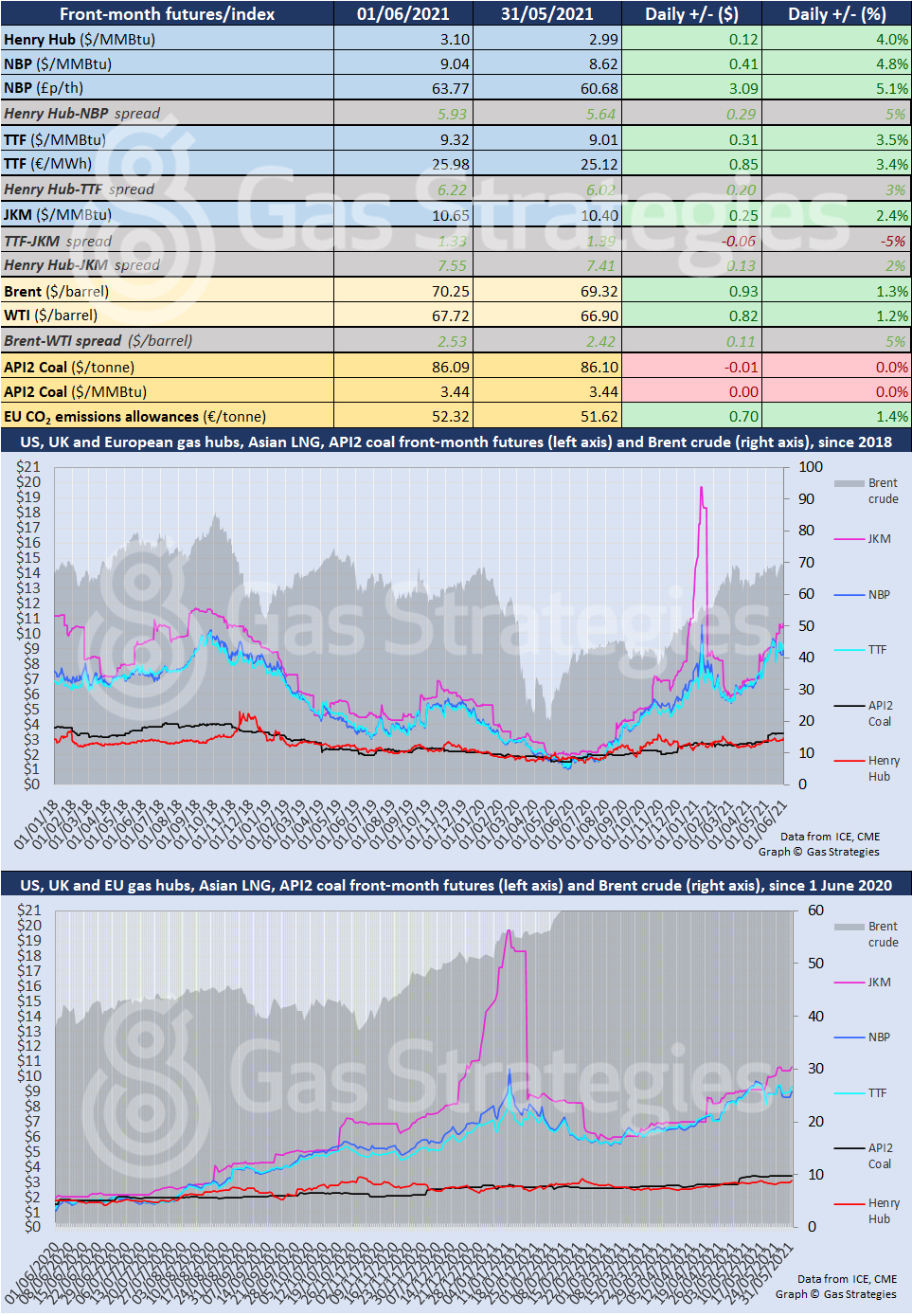

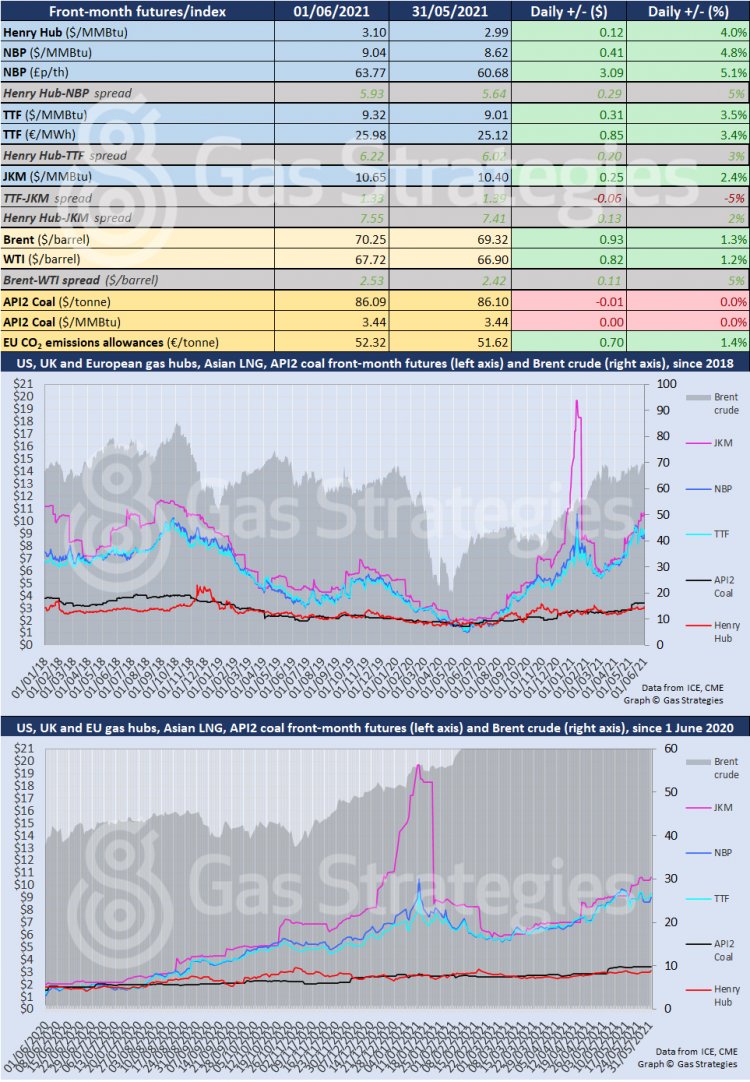

Oil prices closed at their highest level in over two years on Tuesday as the Organization of the Petroleum Exporting Countries (OPEC) and its allies, collectively known as OPEC+, agreed to maintain plans to ease production cuts – signalling an improving demand outlook.

The front-month Brent contract surged to USD 71/barrel during trading on Tuesday before settling at USD 70.25/barrel – its highest close since May 2019. US crude benchmark WTI rallied by 1.2% to close at USD 67.72 – its highest close since October 2018.

Crude prices rallied on OPEC+ agreeing at a meeting on Tuesday to maintain plans to increase production by 450,000 barrels/d starting next month. The cartel’s leader Saudi Arabia will also undo its unilateral cuts of 1 million barrels/d.

Speaking after Tuesday’s meeting, OPEC Secretary General Mohammad Sanusi Barkindo, suggested crude demand could return to the pre-pandemic range in Q4’21, pointing to progress being made with global Covid-19 vaccination programmes and an improving economic growth outlook.

“Turning first to the global economy, our latest projections show GDP growth of 5.5% in 2021, up from 5.4% at our last meeting and driven by expectations for a robust second half of the year,” said Barkindo.

“The projections for oil are largely unchanged from our last meeting, with demand expected to grow by 6 mb/d to around 96.5 mb/d on average for the year, an increase of 6.6%. As with the economy, the market outlook for later this year looks especially promising. In fact, we anticipate that demand will surpass 99 mb/d in the fourth quarter, which would put us back in the range of pre-pandemic levels,” added OPEC’s Secretary General.

Oil prices slid slightly last week amid reports suggesting the US and Iran are making progress with talks over a new nuclear deal – which would enable Iran to increase crude exports. Burkindo played down any impact of additional barrels from Iran, with some market participants suggesting the market will be able to absorb any additional volumes from Iran.

“We anticipate that the expected return of Iranian production and exports will occur in an orderly and transparent fashion, thereby maintaining the relative stability that we have worked hard to achieve since April of last year,” Burkindo said.

Despite bullish expectations over demand, OPEC’s Secretary General did however warn that “this is no time for complacency”.

“As we know from experience over the past year, COVID-19 is a persistent and unpredictable foe, and vicious mutations remain a threat to both human health and the recovery. Furthermore, many leading economies are pumped up by record levels of fiscal and monetary stimulus, debt levels have soared, and inflation is beginning to rear its ugly head in some countries,” Burkindo added.

The crude rally was mirrored in the gas market, with prices in Europe surging on a tight supply outlook.

The front-month TTF and NBP contracts rallied by 3.5% and 4.8% respectively, with both markers closing in the USD 9/MMBtu range. In addition to tight supply – with pipeline imports remaining weak and several LNG plants currently out of action – low wind power availability and strong carbon prices also aided the rally.

The European carbon price rallied by 1.4% to hit EUR 52.32 – its highest close in four days.

The rally by the European gas markers helped push Asian LNG marker JKM higher. A fire at the Shin-Kori 4 nuclear plant in South Korea over the weekend may have also helped lift JKM, with the front-month contract closing 2.4% higher to settle at USD 10.65/MMBtu.

In the US, gas benchmark Henry Hub rallied by 4% to hit USD 3.10/MMBtu – its highest close since 18 May – with the rally prompted by expectations of warmer weather, which is expected to drive demand for air conditioning.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.