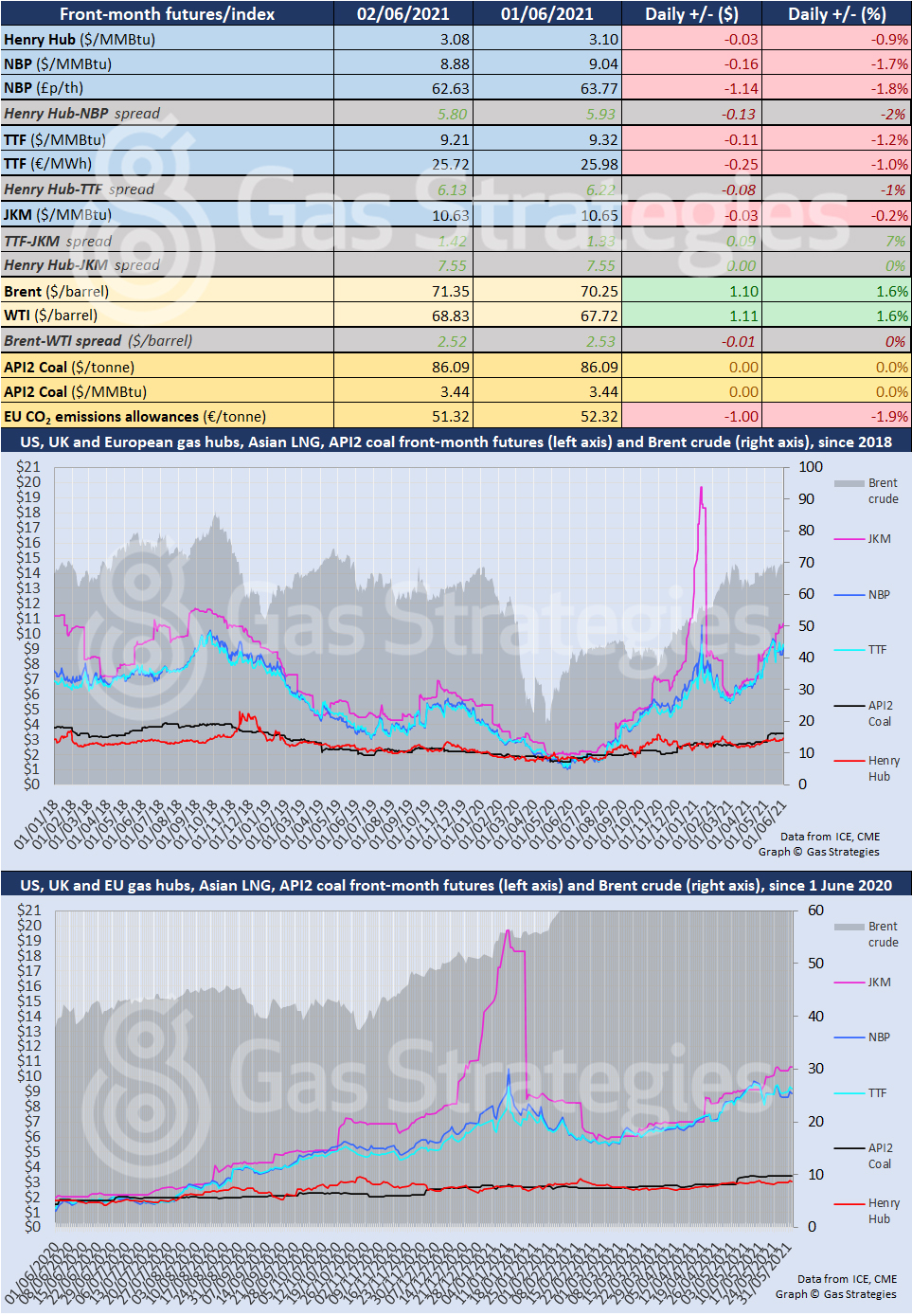

Oil prices closed at their highest level in over two years on Wednesday, with the rally aided by data showing a larger-than-expected draw on US crude inventories last week.

The front-month Brent contract closed at USD 71.35/barrel on Wednesday – its highest close since May 2019. US crude benchmark WTI rallied by 1.6% to close at USD 68.83/barrel – its highest close since October 2018.

Prices were lifted by the American Petroluem Institute reporting on Tuesday that US oil inventories fell by 5.36 million barrels for the week ending 28 May. Analysts had reportedly expected US crude storage to fall by ~2.1 million barrels last week.

The fall in US crude inventories adds to growing bullish sentiment over a recovery in oil demand, with oil prices having recently rallied on expectations of strong demand from North America and Europe this summer as Covid-19 related travel restrictions are lifted.

Prices rallied on Tuesday after the Organization of the Petroleum Exporting Countries (OPEC) and its allies, collectively known as OPEC+, agreed to maintain plans to ease production cuts – signalling an improving demand outlook.

The crude cartel expects oil demand to exceed supply in H2’21, with OPEC forecasting that by the end of the year demand will be just under 100 million barrels/d and supply will total 97.5 million barrels/d.

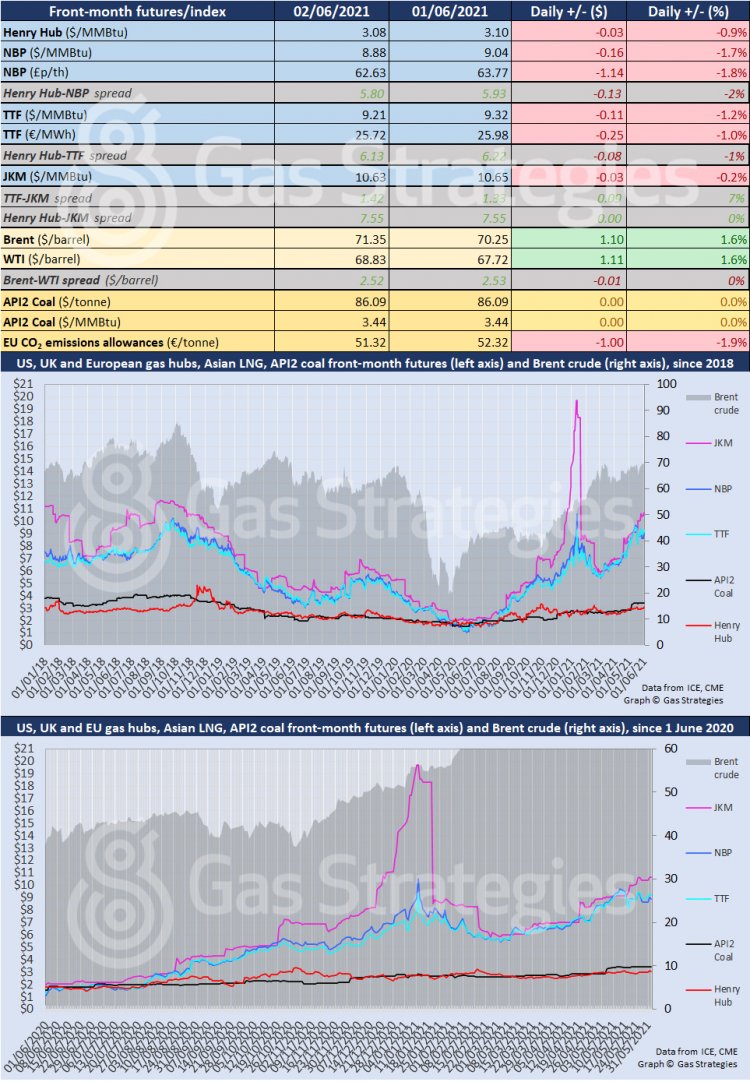

Gas prices failed to mirror the crude price rally, with prices in Europe falling after strong gains on Tuesday.

The front-month TTF and NBP contracts fell by 1.2% and 1.7% respectively, with the UK gas benchmark settling below USD 9/MMBtu.

The weaker European gas prices dragged on the European carbon price, which fell 1.9% to settle in the EUR 51/tonne range, and also weighed on Asian LNG marker JKM, which fell by 0.2%.

Earlier in the week, European gas prices rallied on tight supply, with pipeline imports remaining weak and several LNG plants currently out of action.

In the US, gas benchmark Henry Hub fell by 0.9% but remained in the USD 3/MMBtu range. Henry Hub has been rallying on expectations of warmer weather, which is expected to drive demand for air conditioning.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.