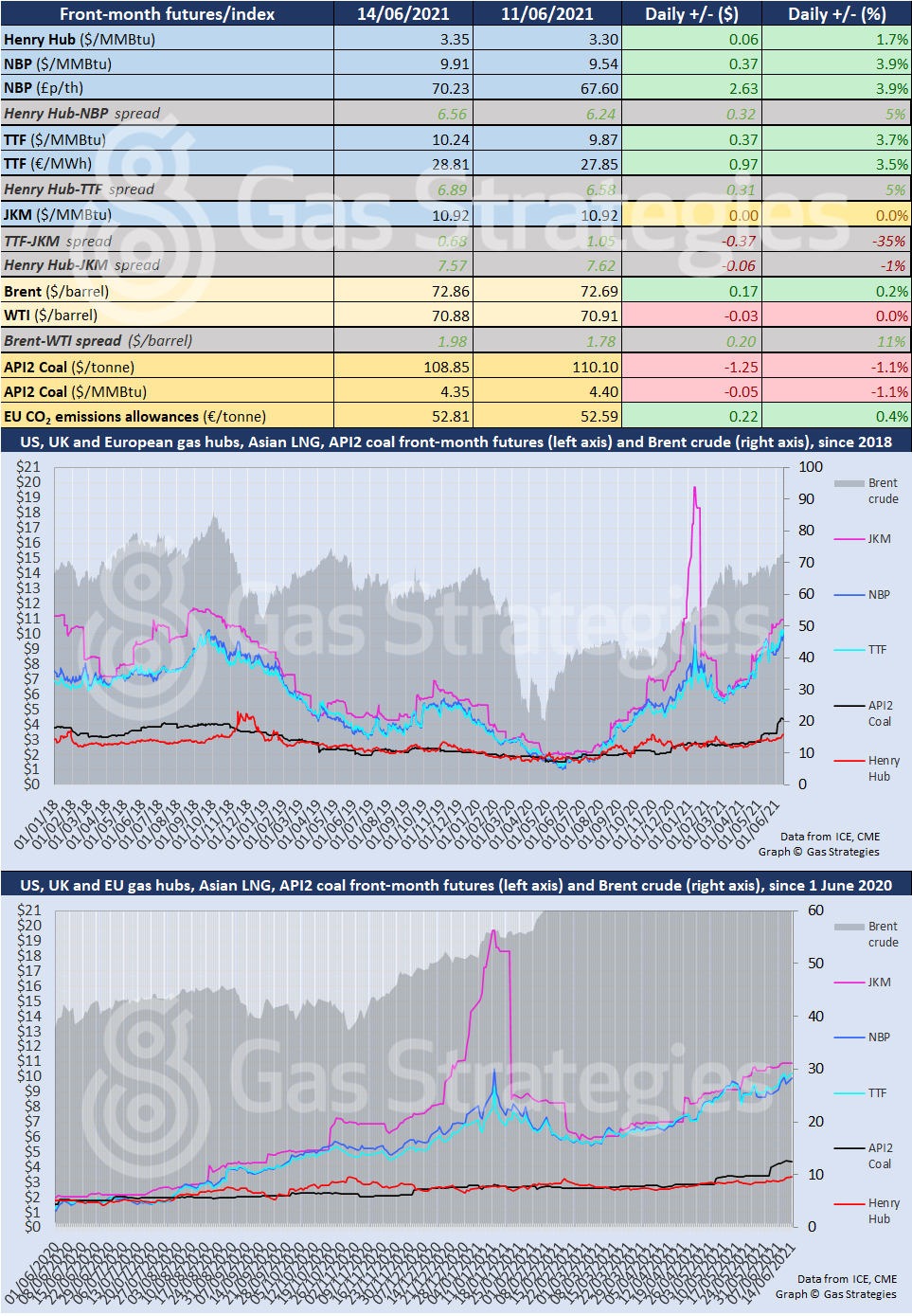

US gas benchmark Henry Hub hit an eight-month high to start the week, with the marker rallying on strong LNG and pipeline exports and warmer weather driving domestic demand.

The front-month Henry Hub price rallied by 1.7% on Monday to make it five days of gains, with the marker settling at USD 3.35/MMBtu – its highest close since October 2020.

Monday’s rally was prompted in part by a recovery in LNG exports, with feed gas deliveries to US LNG plants having dipped to ~8.5 Bcf/d for much of last week due to pipeline maintenance and maintenance at the Cameron LNG facility. However feed gas flows to US LNG plants totalled 9.85 Bcf/d on Monday, according to RonH Energy.

Whilst export demand is strengthening, domestic demand is increasing due to warm weather. On Monday, the Texas power grid operator – the Electric Reliability Council of Texas (ERCOT) – called on consumers in the Lone Star state to conserve power until Friday amid plant outages and rising power demand.

ERCOT did not provide any details on what is causing the “very concerning” number of outages.

In February, the state experienced its first winter blackouts since 2011 due to record power demand and constrained supply caused by a severe winter storm. The cold weather knocked out swathes of oil and gas production, limiting gas supply to power plants.

Across the pond, gas prices in Europe rebounded after slumping on Friday. The rally was prompted by technical buying following profit taking on Friday.

The front-month NBP and TTF contracts rallied by 3.9% and 3.7% respectively to start the week, with the UK benchmark closing at the equivalent of USD 9.91/MMBtu and TTF returning to the USD 10/MMBtu range.

The rally helped lift the European carbon price, which rallied by 0.4% to settle at EUR 52.81/tonne.

As for Asian LNG marker JKM, the front-month contract remained unchanged at USD 10.92/MMBtu to start the week. The rally by TTF saw JKM’s premium over the Dutch marker cut to USD 0.68/MMBtu on Monday.

Whilst European gas prices rallied, European coal prices fell for the first time in four days, with the front-month API2 coal contract settling at USD 108.85/tonne.

Crude prices were mixed on Monday, with Brent rallying by 0.2% and WTI recording a marginal loss.

The dip by WTI was pinned on the US Energy Information Administration (EIA) forecasting that US shale oil output will increase by ~38,000 barrels/d in July to total ~7.8 million barrels/d. Last week crude prices rallied on the International Energy Agency (IEA) calling on OPEC to “open the taps” amid an expected rebound in crude demand.

However, prices may dip on Tuesday after Britain on Monday evening pushed back the lifting of Covid-19 restrictions by a month due to surging Covid-19 cases. The move may dampen a recovery in crude demand.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.