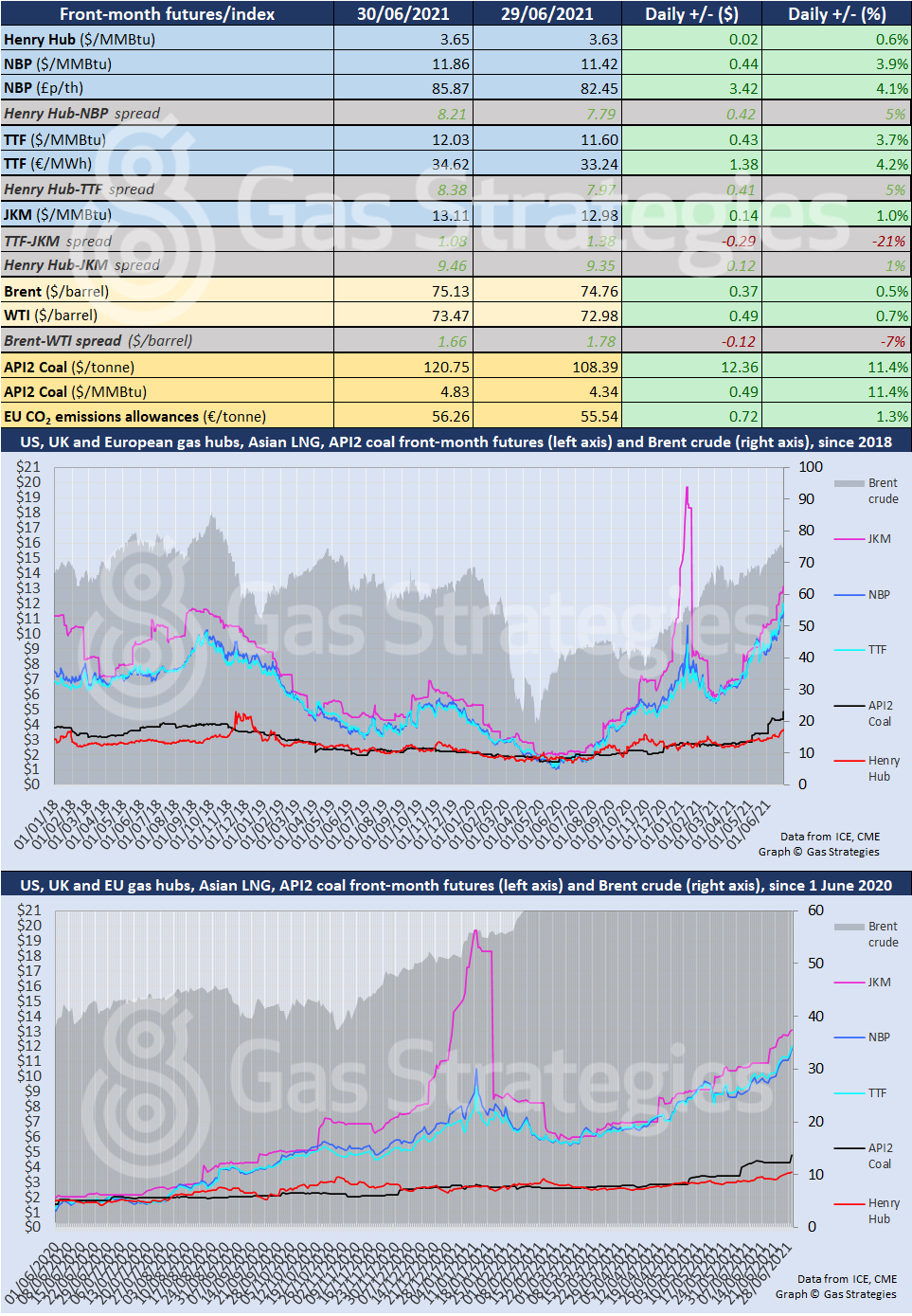

European gas prices continued to soar on Wednesday, with the front-month TTF contract closing just shy of a seasonal record high.

The front-month TTF and NBP contracts rallied by over 3% on Wednesday, with the Dutch marker closing in the USD 12/MMBtu range and the UK marker closing at USD 11.86/MMBtu. In EUR/MWh terms, TTF closed just shy of the historical peak of EUR 35/MWh, set in October 2008. As for NBP, it closed at its highest level in GBP/th terms since January 2006.

Prices have been rallying amid a tight supply outlook, with Gazprom opting not to bid for any interruptible capacity through Ukraine in the latest auction held by Ukraine’s TSO this week.

The Russian firm is set to conduct planned maintenance on its Yamal and Nord Stream 1 pipelines later this month, a move which will tighten supply to Europe which is currently battling with Asia for LNG cargoes.

The rally helped push Asian LNG marker JKM higher, with the front-month contract rallying by 1% to close in the USD 13/MMBtu range.

It is not only gas prices in Europe that are hitting multi-year highs. Coal prices on the continent have recently hit a decade high, with the front-month API2 contract rolling over to July on Wednesday to settle at USD 120.75/tonne.

Prices have been rallying amid China’s ban on coal imports from Australia, which has seen the nation draw more cargoes away from the Atlantic basin. Prices have also rallied due to strong gas and power prices in Europe.

The bullish coal and gas prices in Europe have helped push the European carbon price higher, with the July-date contract on Wednesday closing just shy of the record price set in May.

The gas price rally has not been limited to Asia and Europe, with US benchmark Henry Hub making it seven days of gains on Wednesday as the marker closed at USD 3.65/MMBtu – its highest close since December 2018. Henry Hub has been rallying on the back of lower production and strong demand, with domestic demand strengthening due to warm weather and pipeline and LNG exports booming.

Crude prices continued to rally on Wednesday, pushed higher by news of a sixth straight week of drawdowns on US crude storage.

Brent and WTI closed 0.5% and 0.7% higher respectively, with Brent pushing into the USD 75/barrel range and WTI returning to the USD 73/barrel range.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.