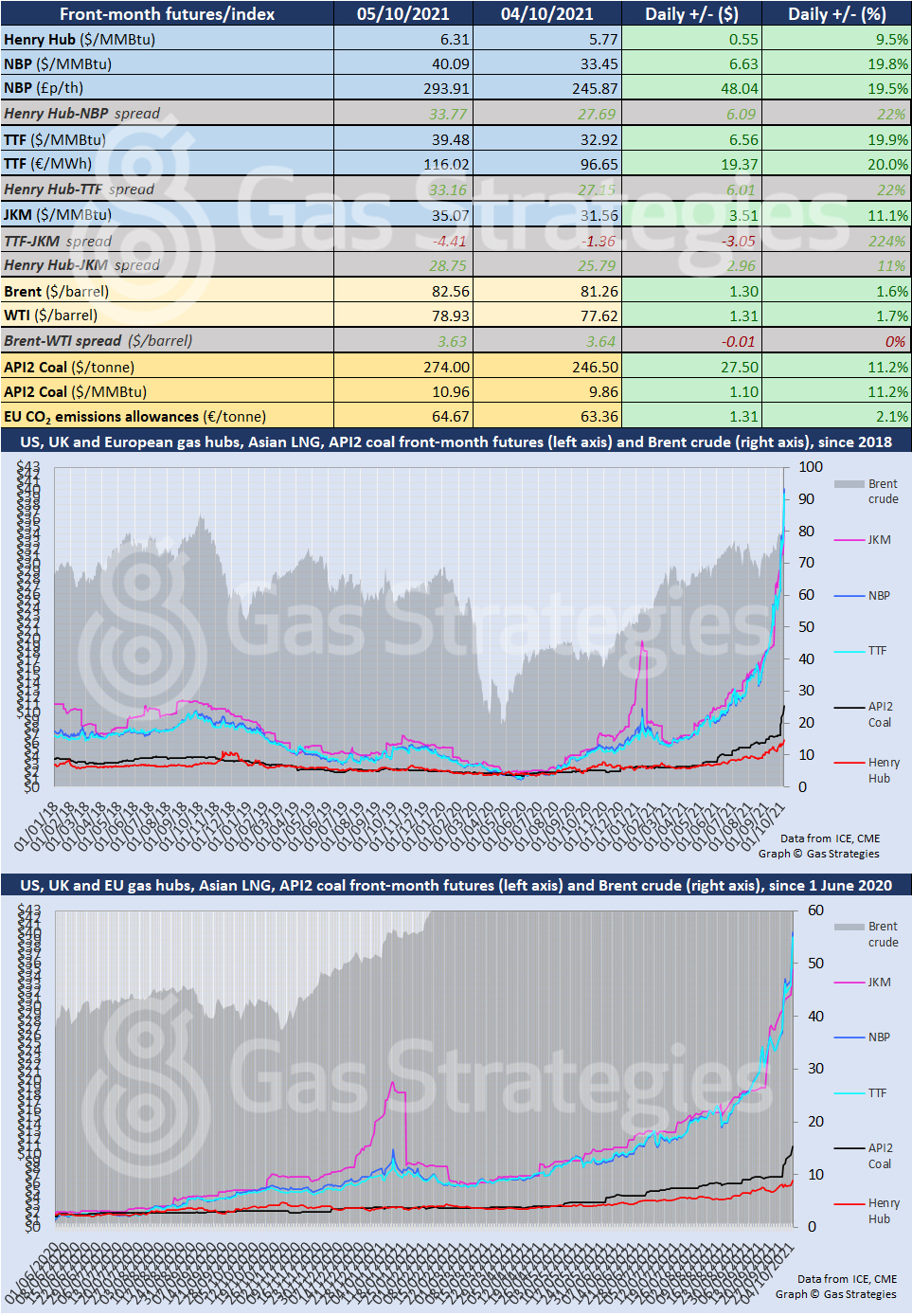

European gas prices soared to record highs on Tuesday, pushed higher by forecasts of colder weather – exacerbating ongoing supply concerns ahead of winter.

The TTF and NBP front-month contracts surged by over 19% on Tuesday, with the UK marker closing at the equivalent of USD 40.09/MMBtu – USD 0.61/MMBtu higher than the Dutch gas benchmark.

In addition to forecasts of colder weather, low wind power generation in the UK also helped push gas prices higher.

The gains outstripped those recorded by JKM, with the Asian LNG marker closing 11.1% higher at USD 35.07/MMBtu. The result saw NBP-JKM spread widen to USD 5.02/MMBtu, with TTF’s premium over the Asian LNG benchmark increasing to USD 4.41/MMBtu.

In the US, Henry Hub hit a 12-year high, closing 9.5% higher at USD 6.31/MMBtu. The rally was pinned on lower production – aiding supply concerns ahead of winter.

Coal prices in Europe also surged on Tuesday, with the front-month API2 coal contract closing 11.2% higher at USD 274/tonne. Record gas prices are forcing power producers in Europe to procure and burn more coal, however supply is tightening as China and India are increasing imports.

China is looking to import more coal to alleviate severe power shortages, with the nation this week starting to unload shipments of Australian coal despite an unofficial ban on imports from Australia.

In India, as of 1 October over half of the nation’s coal fired power plants had less than three days of supplies remaining. Domestic coal production has been hit by heavy rain, with India’s power producers having refrained from importing volumes in recent weeks due to soaring prices.

The surging coal and gas prices helped lift the European carbon price to a record high, with the front-month contract closing at EUR 64.67/tonne.

In turn, rocketing gas, coal and carbon prices pushed power prices in Europe to fresh record highs. Day-ahead prices in Germany, France, Belgium and the Netherlands averaged over EUR 180/MWh – a day-on-day increase of over EUR 20/MWh.

Crude prices hit fresh multi-year highs as the market continued to digest OPEC+’s decision to stick with its production quota, despite growing concerns over supply tightness as demand recovers.

Brent closed at USD 82.56/barrel – its highest close since October 2018, with WTI closing at USD 78.93/barrel – its highest close since late 2014.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.