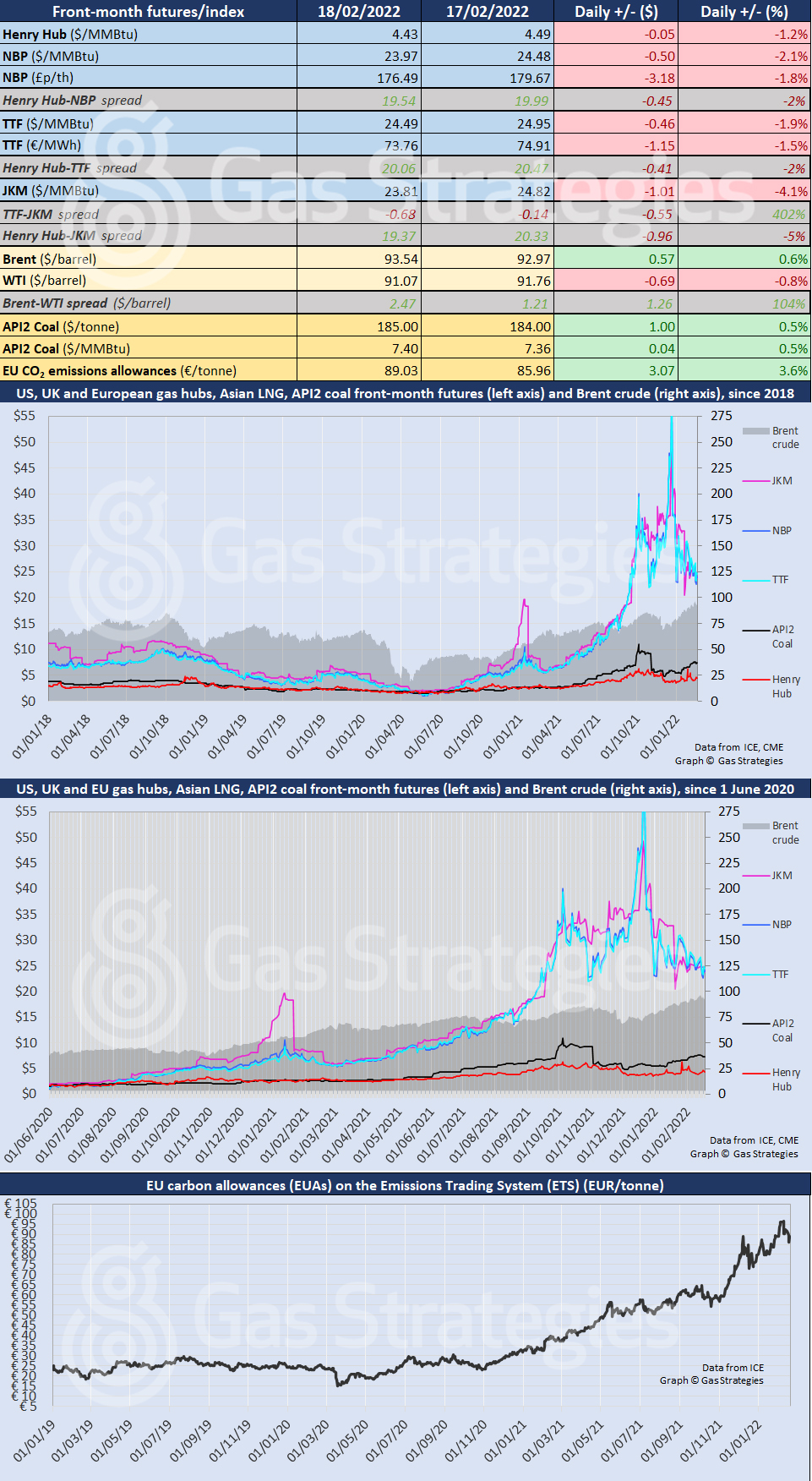

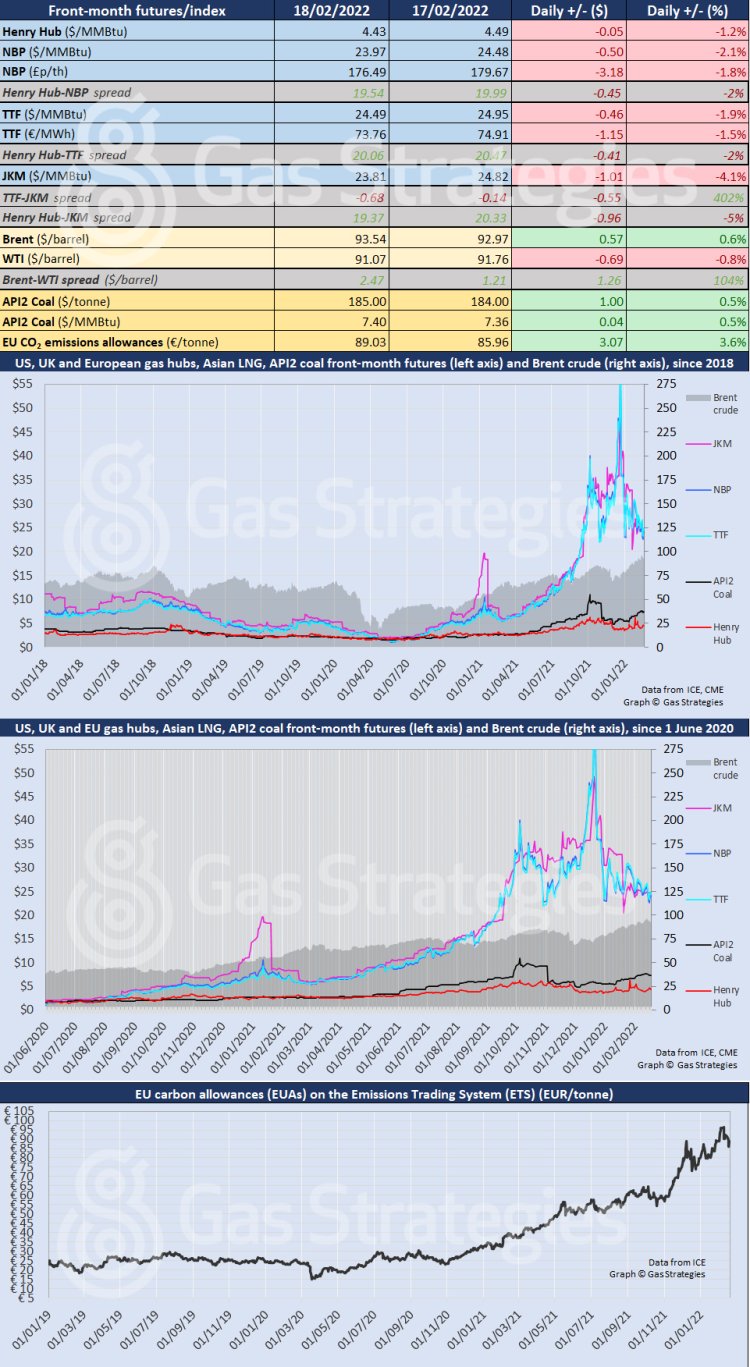

European gas prices returned to the red on Friday, falling amid strong LNG imports and weaker gas demand due strong wind power generation.

The front-month NBP and TTF contracts closed ~2% lower on Friday, with the Dutch marker settling at the equivalent of USD 24.49/MMBtu, USD 0.48/MMBtu higher than the UK gas benchmark.

The slump was pinned on continued strong LNG imports into Europe, helping offset a dip in pipeline flows from Norway. Lower gas demand also weighed on prices, with strong wind power generation denting gas demand in the power sector.

While gas prices fell, the European carbon price bounced back, closing 3.6% at EUR 89.03/tonne.

US natural gas benchmark Henry Hub fell back into the red at the end of the week, closing 1.2% lower at USD 4.43/MMBtu.

The front-month JKM contract rolled over to April on Friday and closed 4.1% lower at USD 23.81/MMBtu.

In the oil market, prices diverged on Friday, with Brent up 0.6% and WTI closing 0.8% lower. Market participants were weighing up potential supply disruption caused by a conflict in Ukraine, and a potential increase in Iranian oil exports should the nuclear deal be revived.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.