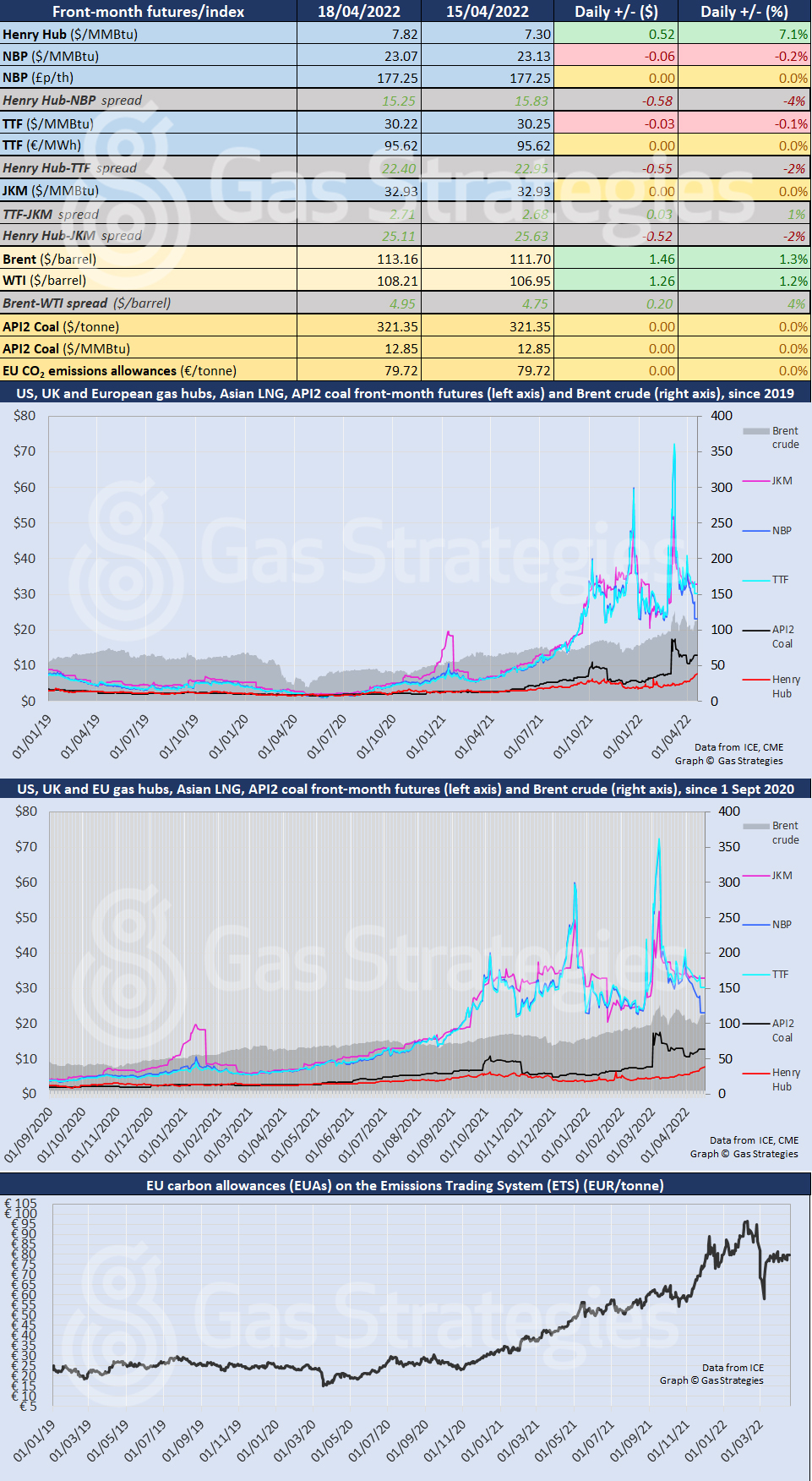

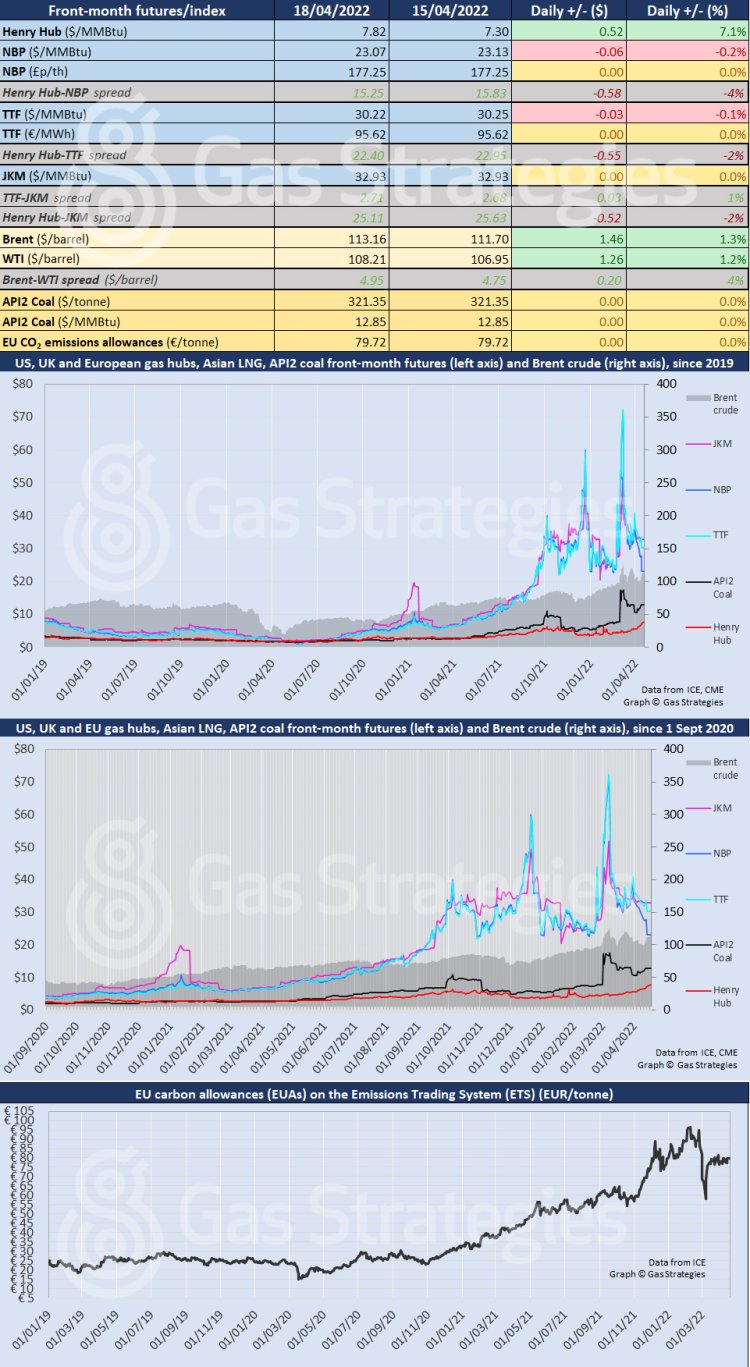

US gas benchmark Henry Hub hit an intraday high of USD 8.7/MMBtu to start the week, with the May-dated contract settling at its highest level since August 2008 on Monday.

The front-month Henry Hub contract closed at USD 7.82/MMBtu on Monday, marking a 7.1% increase compared to Thursday last week – the previous close due to the Easter public holiday.

The marker has been soaring in recent days amid supply concerns, with US gas production showing no signs of increasing in the short term. While production remains flat, demand is soaring. Colder weather across the north-east of the US is expected to increase gas demand in the coming days.

Additionally, gas flows to US LNG plants recovered on Monday, having fallen to 10.48 Bcf/d on Friday – the lowest level since 22 February, according to data compiled by RonH Energy. Feedgas flows stood at 12.38 Bcf/d on Monday, with Cheniere’s Corpus Christi plant behind the dip in flows on Friday. Flows to Corpus Christi fell from 2.28 Bcf/d on Thursday to 0.55 Bcf/d on Friday, according to RonH Energy.

Across the pond, European gas markers TTF and NBP remained unchanged amid limited trading due to the public holiday. Asian LNG marker JKM was also unchanged.

As for oil, Brent and WTI closed over 1% higher on Monday, with outages in Libya exacerbating supply concerns.

Brent settled at USD 113.16/barrel, with WTI closing at USD 108.21/barrel.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.