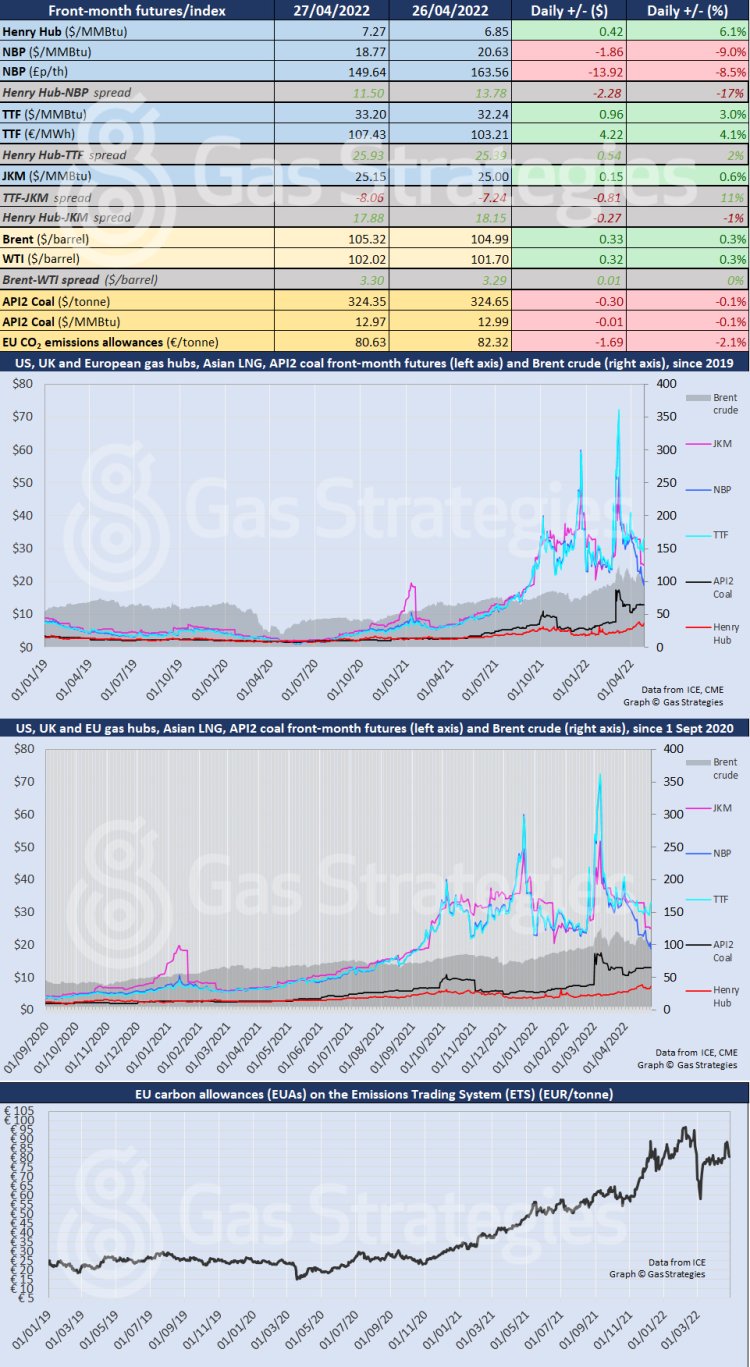

European gas prices diverged on Wednesday, with Dutch gas benchmark TTF rallying and UK maker NBP falling to a fresh seven-month low. Prices on both hubs had spiked in early morning trading following Gazprom announcing it had halted gas supplies to Poland and Bulgaria, however gains on TTF were capped by increasing gas flows from Russia.

The front-month TTF contract closed 3% higher at the equivalent of USD 33.2/MMBtu. As for NBP, it fell 9% to close at the equivalent of USD 18.77/MMBtu – its lowest close in USD/MMBtu terms since 6 September 2021.

Both markers surged during early morning trading amid news that Gazprom had halted gas supplies to Poland and Bulgaria due to both nations failing to pay for gas volumes in rubles. The move by Gazprom has raised concerns that other European nations could see supplies cut if they do not adhere to the new ruble payment terms.

However, gains were capped on Wednesday as Russian flows increased, averaging 223 MMcm/d, up from 207 MMcm/d on Tuesday, according to EnergyScan. The increase may be due to European buyers upping offtake under long-term contracts amid heightened concerns over future flows.

As for the UK marker, NBP has fallen in recent days amid strong LNG and pipeline imports from Norway, with the nation less dependent on Russian gas volumes.

Strong imports and limited storage has left the UK with a gas glut, with the nation struggling to export volumes to continental Europe. A force majeure event on the Interconnector pipeline – running between the UK and Belgium – has capped exports.

The pipeline operator informed shippers on Thursday that the Bacton terminal has “received large volumes of solid material from the National Transmission System, that has affected filters at our Bacton Facilities”.

“The delivery of off-specification Natural Gas and this material is beyond our reasonable control… and means that we are unable to fully perform our obligations under the Agreement,” Interconnector added.

Across the pond, US gas benchmark Henry Hub retuned to the USD 7/MMBtu range for the first time since 19 April. The gains were largely pinned on Gazprom cutting flows to Poland and Bulgaria, with the market viewing this as potentially signalling stronger demand for US LNG.

As for Asian LNG marker JKM, the front-month contract recovered, closing 0.6% to close at USD 25.15/MMBtu.

Oil prices remained largely flat, closing 0.3% higher.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.