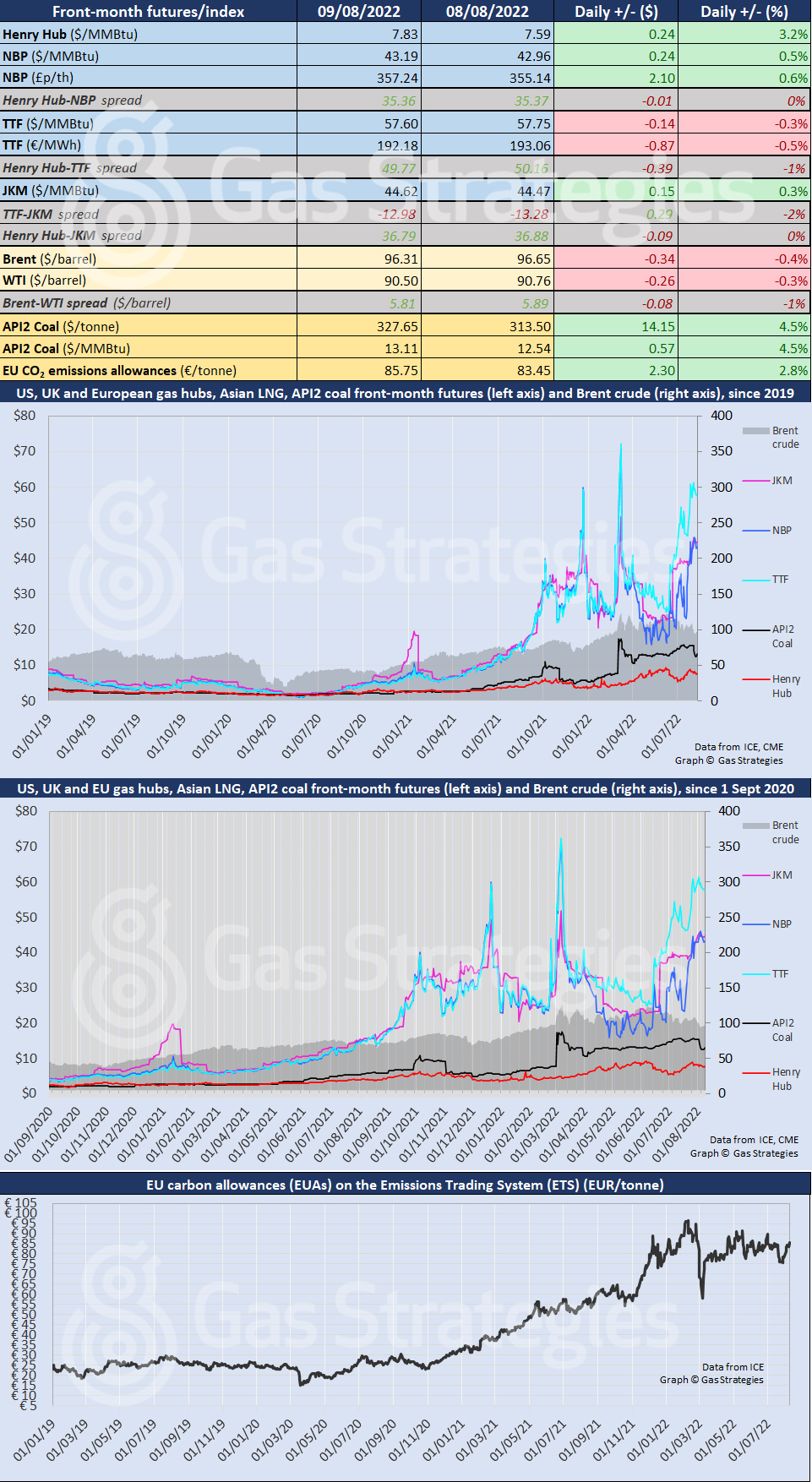

US gas benchmark Henry Hub staged a recovery on Tuesday, pushed higher by domestic gas production tumbling ~2 Bcf day-on-day.

The front-month Henry Hub contract closed 3.2% higher at USD 7.83/MMBtu, with the rally prompted by gas production falling from a near all-time high of ~98 Bcf/d to 96 Bcf/d on Tuesday. The dip was pinned on maintenance activity across several US shale basins.

In Europe, gas prices diverged but were largely stable. Dutch marker TTF closed 0.3% lower at the equivalent of USD 57.6/MMBtu, with NBP settling 0.5% higher at USD 43.19/MMBtu.

Asian LNG marker JKM brushed off Monday’s loss, closing 0.3% higher at USD 44.62/MMBtu. The rally, combined with TTF’s loss, saw the TTF-JKM spread narrow to USD 12.98/MMBtu.

As for crude, Monday’s rally was short-lived as Brent and WTI stumbled on Tuesday. The fall came despite news of the suspension of Russian oil exports to Europe through the Druzhba pipeline which transits Ukraine. Recession fears and reports suggesting the EU is close to reviving the nuclear deal with Iran outweighed news of the suspension of flows on the Druzhba pipeline.

Brent settled 0.4% lower at USD 96.31/barrel, with WTI down 0.3% at USD 90.50/barrel.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.