European prices continued rising on Monday, albeit at a slower pace than last week, as ongoing strikes in France raise supply risks amid an upcoming cold snap across much of the continent.

A colder-than-normal start to April could prolong the heating season which runs out on 31 March. This could add pressure to the market just as supply worries are mounting with protests in France are hitting nuclear power output and blocking LNG terminals and oil refineries.

However, the markets seem to have stopped to take a breather after the big losses witnessed on Friday last week.

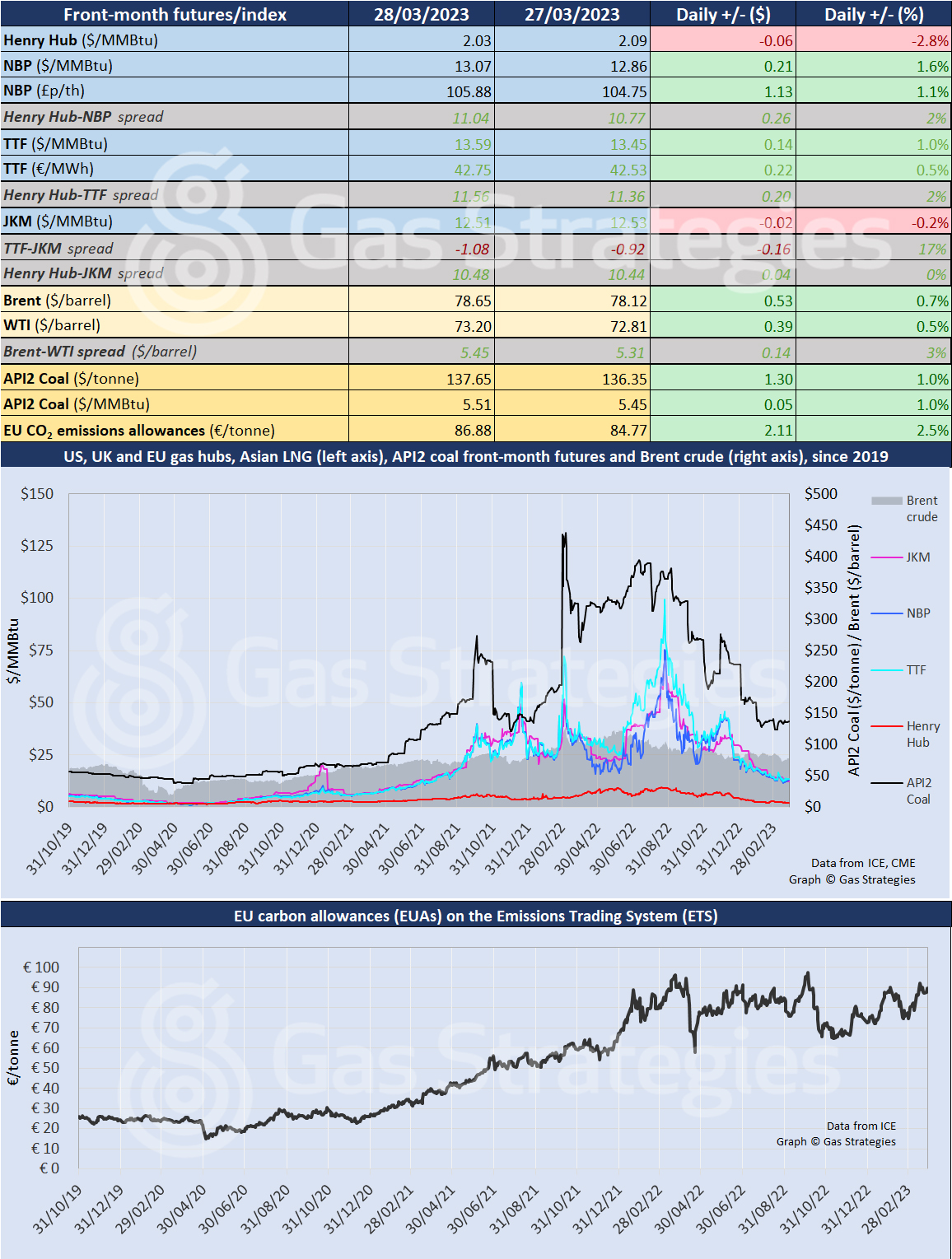

NBP’s front-month contract advanced by 1.6% to USD 13.07/MMBtu, while TTF rose 1% to USD 13.59/MMBtu.

JKM saw its third-consecutive decline on Monday and settled at USD 12.51/MMBtu.

In the US, Henry Hub fell for the second time in a row, further hampered by abundant supplies and weakening weather-driven demand. Henry Hub’s front-month price settled at USD 2.03/MMBtu, its lowest this year and the weakest it has been since July 2020, when the Covid-19 pandemic was in full swing.

Crude continued slipping on Monday, but also at a slower pace than the USD 3 losses seen on Friday. Brent gained 0.7% settling at USD 78.65/barrel and WTI rose 0.5% to USD 73.20/barrel.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):  Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.