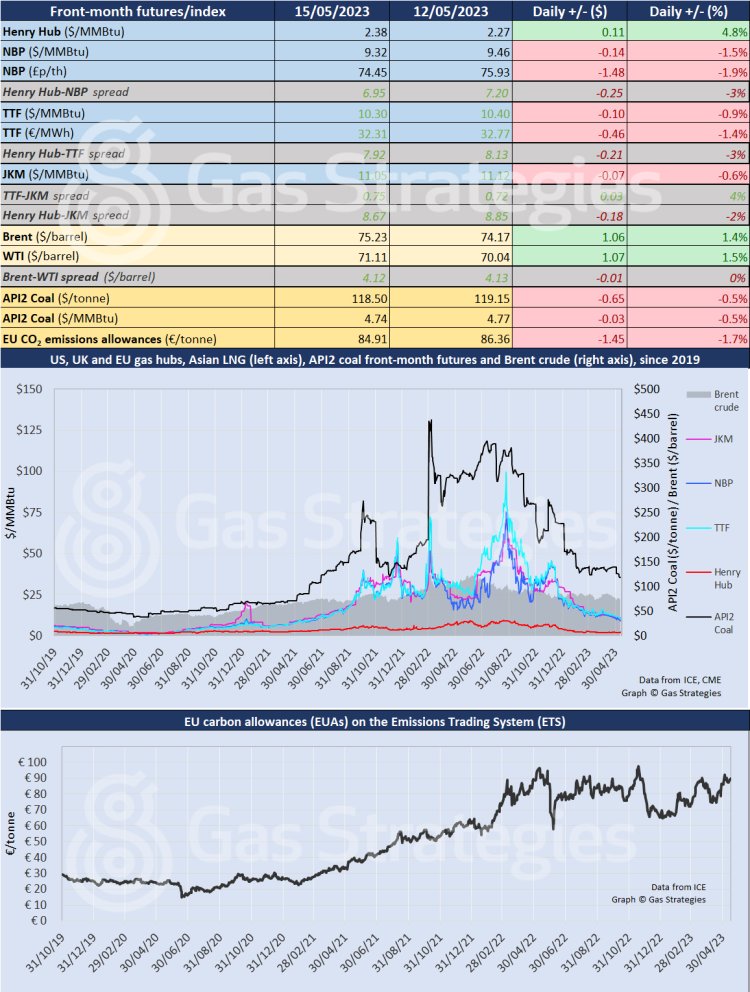

Weakness in natural gas prices in Europe continued on Monday, albeit at a slower pace than at the end of last week, as the market continues being well supplied and weather patterns remain favourable.

Weakness in natural gas prices in Europe continued on Monday, albeit at a slower pace than at the end of last week, as the market continues being well supplied and weather patterns remain favourable.

There’s growing confidence that the market will be able to withstand any potential shocks and that Europe would be able to meet storage filling targets following the price spikes last year.

However, there is still a high chance of prices rising again if gas consumption rises in line with air conditioning demand due to hotter temperatures.

But for now, the front-month NBP contract declined by 1.5% to USD 9.32/MMBtu, while TTF saw a 0.9% fall to 10.30/MMBtu. The Asian LNG marker JKM saw a 0.6% downtick to USD 11.05/MMBtu.

In addition, analysts at Kpler have forecast that UK LNG import volumes could decline by 17% to a three-month low in May, largely due to slowing seasonal demand and ample supply in storage.

The UK could receive 1.78 mt (2.4 Bcm) of LNG this month, compared with 2.14 mt in April and a year-to-date average of nearly 2 mt/month, provisional Kpler data showed.

In the US, Henry Hub prices continued ascending as they continued to recover from the extreme lows of the past few months. The front-month contract rose 4.8% to USD 2.38/MMBtu, as the market is still bearing the burden of the Baker Hughes report which showed that the number of gas rigs in the country declined to a low last week.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):  Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.