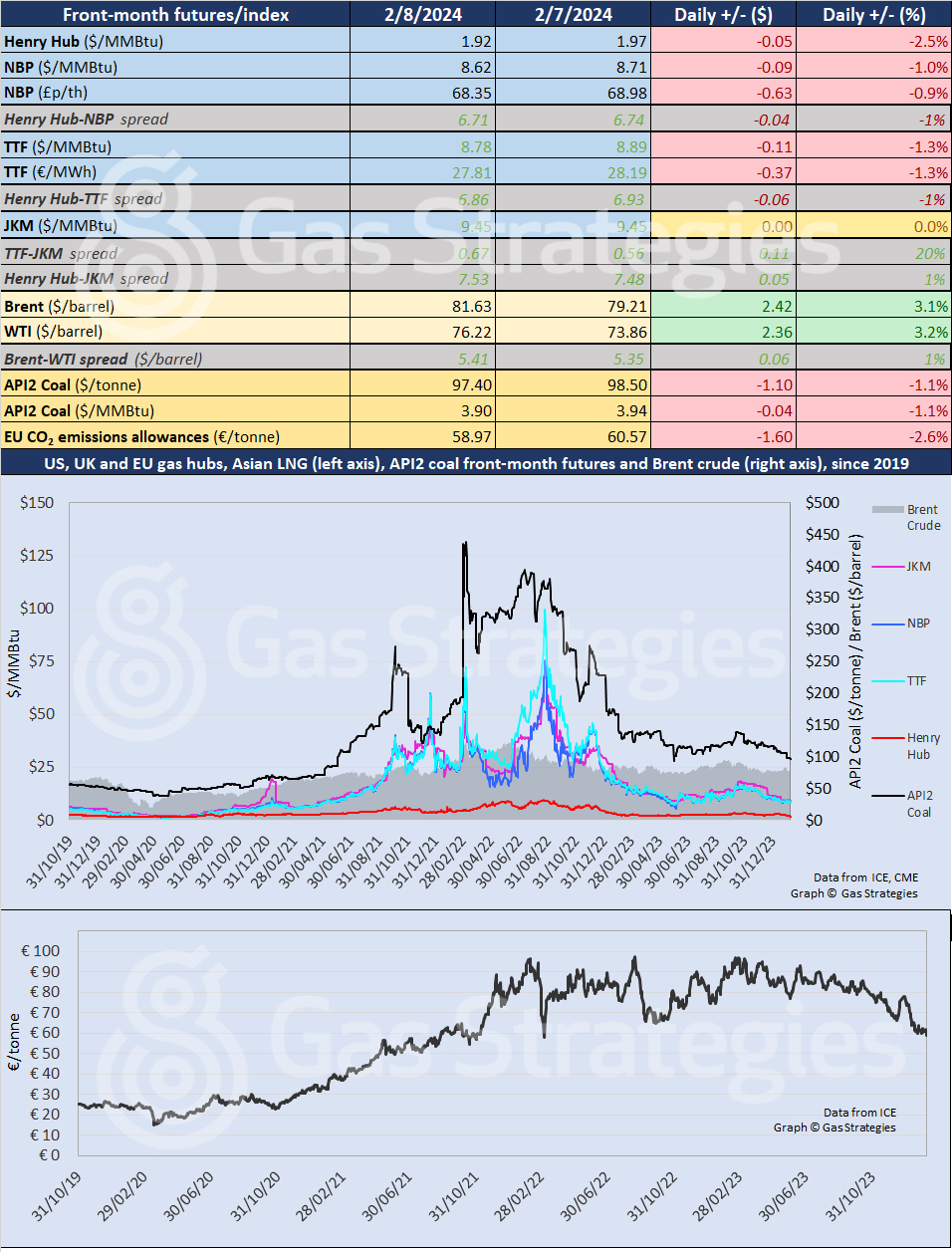

US natural gas prices continued to tumble downwards yesterday as the Energy Information Administration (EIA) issued its latest storage data update amid expectations that withdrawals will remain lower than usual over the coming fortnight because of unseasonably mild weather.

Henry Hub front-month futures closed 2.5% down, from USD 1.97/MMBtu on Wednesday to USD 1.92/MMBtu on Thursday, having closed below USD 2/MMBtu on Wednesday for the first time since March 2023.

Yesterday’s EIA report estimated working gas in storage at 2,584 Bcf as of 2 February, down 75 Bcf from the previous week and within the five-year historical range. Stocks were 187 Bcf higher year-on-year and 248 Bcf above the five-year average of 2,336 Bcf. No alarms and no surprises.

European gas prices continued their downward trajectory, with supplies strong, storage comfortable and the weather mild. Markets appear to have taken in their stride the re-routing of LNG tankers around Africa to avoid attacks from Yemen-based Houthis in the Red Sea.

In Continental Europe, front-month TTF was down 1.3%, from USD 8.89/MMBtu on Wednesday to USD 8.78/MMBtu on Thursday, with the UK’s NBP down 1.0%, from USD 8.71/MMBtu to USD 8.62/MMBtu. Prices opened lower on Friday and then tracked sideways throughout the morning.

Data from Gas Infrastructure Europe showed storage facilities to be 67.9% full in the European Union and 67.8% full in the UK.

In Asia, the JKM LNG price was unchanged at USD 9.45/MMBtu, with the TTF-JKM spread up a fifth to USD 0.67/MMBtu.

Crude oil prices continued to move upwards, with Brent back above USD 80/barrel, as traders digested the political implications of Israel’s rejection of the Hamas response to the latest ceasefire proposals for Gaza. Negotiators have not given up, however.

Brent crude rose by 3.1%, from USD 79.21/barrel on Wednesday to USD 81.63/barrel on Thursday, with WTI up 3.2%, from USD 73.86/barrel to USD 76.22/barrel. Prices remained stable at around these levels on Friday morning.

European coal prices took their lead from gas, their loose correlation continuing, with API2 down 1.1%, from USD 3.94/MMBtu on Wednesday to USD 3.90/MMBtu on Thursday.

European carbon prices were no exception to the bearish mood in European energy, with emissions allowances down 2.6% to EUR 58.97/tonne.

Front-month futures and indexes at last close with day-on-day changes (click to enlarge):

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.