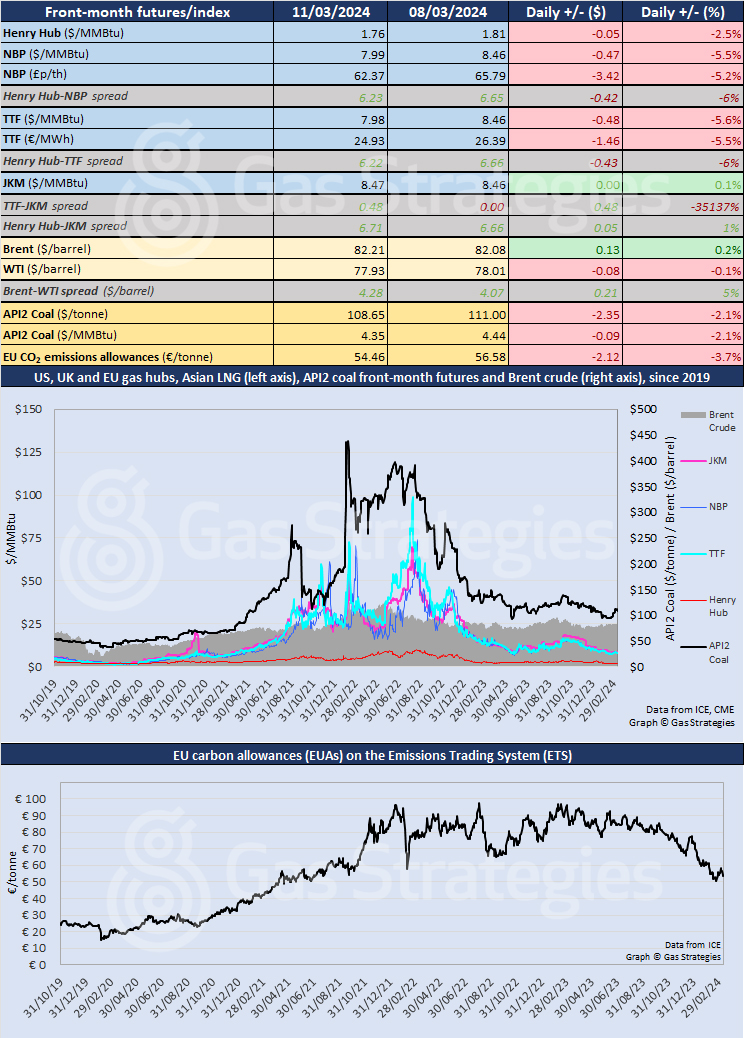

Volatility returned to European natural gas futures on Monday, with falls of more than 5% taking TTF and NBP back below USD 8/MMBtu. European coal and carbon prices also fell but less dramatically.

In continental Europe, TTF closed down 5.6%, from USD 8.46/MMBtu on Friday to USD 7.98/MMBtu on Monday. In the UK, NBP fell by 5.5%, from USD 8.46/MMBtu to USD 7.99/MMBtu. Prices remained volatile on Tuesday but without a clear direction.

Sticking with unabated gas

UK prime minister Rishi Sunak confirmed on Tuesday that investment in unabated gas-fired electricity generation would continue to be supported to “keep lights on and bills down when the sun isn’t shining and the wind isn’t blowing”.

The UK’s plan is two-pronged: to firstly extend the life of existing gas facilities, where it is practical to do so, and to build new capacity to replace the gas-fired power plants that would need to be retired.

“Without gas backing up renewables, we face the genuine prospect of blackouts,” Energy security secretary Claire Coutinho added.

Sunak said the UK would continue its efforts to meet its legally binding net-zero emissions commitments and that the country’s last coal-fired power station would close this year. New gas plants will be required to be “net-zero ready”.

However, he did not explain the potential source of the cash needed to build plants that are expected to play a primarily backup role and therefore “run less frequently as the UK continues to roll out other low-carbon technologies”, according to the Department for Energy Security and Net Zero.

Natural gas futures in the US also moved downwards, with front-month Henry Hub falling by 2.5%, from USD 1.81/MMBtu on Friday to close at USD 1.76/MMBtu on Monday. It was the fourth consecutive decline, despite forecasts of cooler weather in the second half of March.

Feed gas deliveries to Freeport LNG, where one of three liquefaction trains is being repaired, fell further over the weekend – amid speculation that gas storage data later this week might show an early injection rather than a withdrawal.

In Asia, the JKM LNG price bucked the downward trend, edging up by 0.1% to USD 8.47/MMBtu, widening the TTF-JKM margin from zero to USD 0.48/MMBtu.

Crude oil futures remained stable, with economic concerns continuing to offset geopolitical worries. Brent crude edged up 0.2% to USD 82.21/barrel, while WTI eased by 0.1% to USD 77.93/barrel.

European coal prices moved downwards, with API2 falling by 2.1%, from USD 4.44/MMBtu on Friday to USD 4.35/MMBtu on Monday.

EU emissions allowances lost 3.7% to close at EUR 54.46/tonne.

Front-month futures and indexes at last close with day-on-day changes:

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.