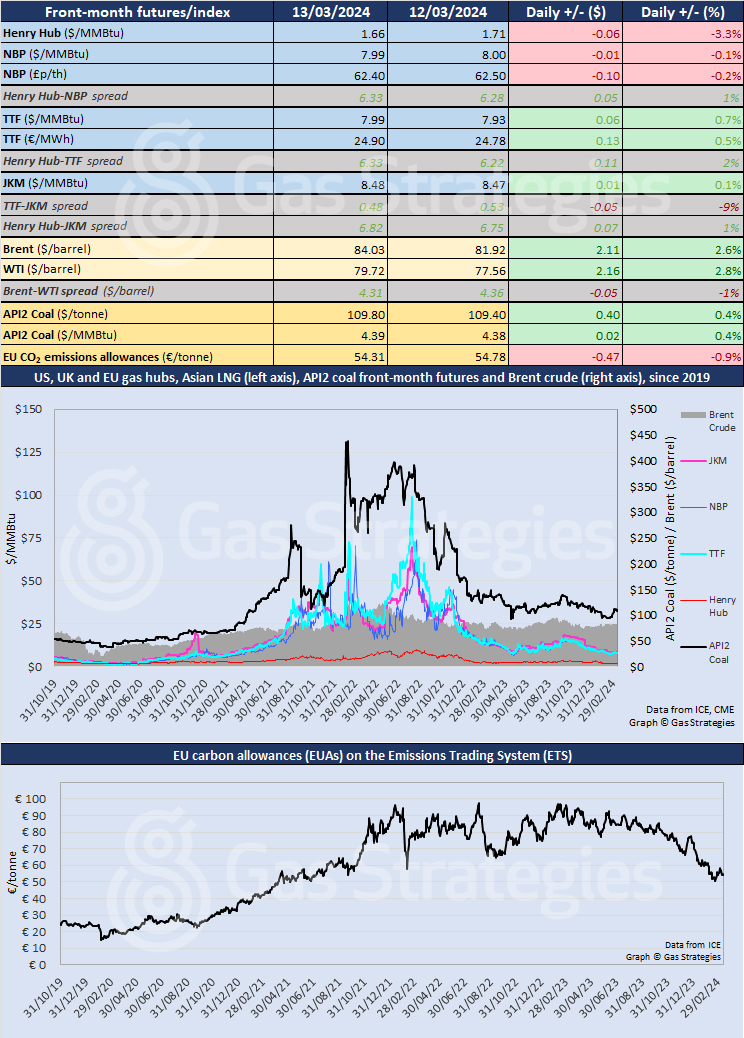

The Brent front-month crude oil futures contract closed at its highest level since the start of November on Wednesday and was climbing again on Thursday morning. The jump came amid reports of falling inventories in the US and attacks mounted by Ukraine on refineries in Russia. US natural gas futures continued to spiral downwards.

Brent climbed by 2.6%, from USD 81.92/barrel on Tuesday to USD 84.03/barrel on Wednesday. WTI rose by 2.8%, from USD 77.56/barrel to USD 79.72/barrel, its highest level for a fortnight.

The jump in Brent was notable because it has been trading within a narrow band for over a month.

In its weekly petroleum status report, the US Energy Information Administration (EIA) said commercial crude inventories were down by 1.5 million barrels week-on-week and 3% below the five-year average for the time of year, at 447 million barrels. Oil imports for the past four weeks were 2.9% higher year-on-year.

More bullish sentiment came from the International Energy Agency’s monthly oil report, which said “global oil demand is forecast to rise by a higher-than-expected 1.7 million b/d in 1Q24 on an improved outlook for the US and increased bunkering”.

Growth in 2024 has been revised up by 110 kb/d from last month’s report but expansion, at 1.3 million b/d, will be slower than 2023’s 2.3 million b/d because of efficiency gains and the growing number of electric vehicles.

Houthi shipping attacks in the Red Sea continued to impact oil prices in February, says the agency, with more oil kept on the water as oil tankers took the longer route around Africa “further tightening the Atlantic Basin market and sending crude’s forward price structure deeper into backwardation”.

Global supply for 2024 is forecast to increase by 800 kb/d to 102.9 million b/d, including a downward adjustment to OPEC+ output because of recently agreed curbs.

In the US, Henry Hub futures fell for a sixth consecutive session, ahead of today’s storage report from the EIA, which some traders believe could show an early injection rather than a withdrawal.

Front-month Henry Hub was down another 3.3%, from USD 1.71/MMBtu on Tuesday to USD 1.66/MMBtu on Wednesday.

Price movements in other markets were muted.

European gas futures diverged for a second time, with April TTF up 0.7% to USD 7.99/MMBtu and NBP down 0.1% to USD 7.99/MMBtu, putting the two contracts on parity. In Asia, JKM edged up 0.1% to USD 8.48/MMBtu.

Front-month futures and indexes at last close with day-on-day changes:

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.