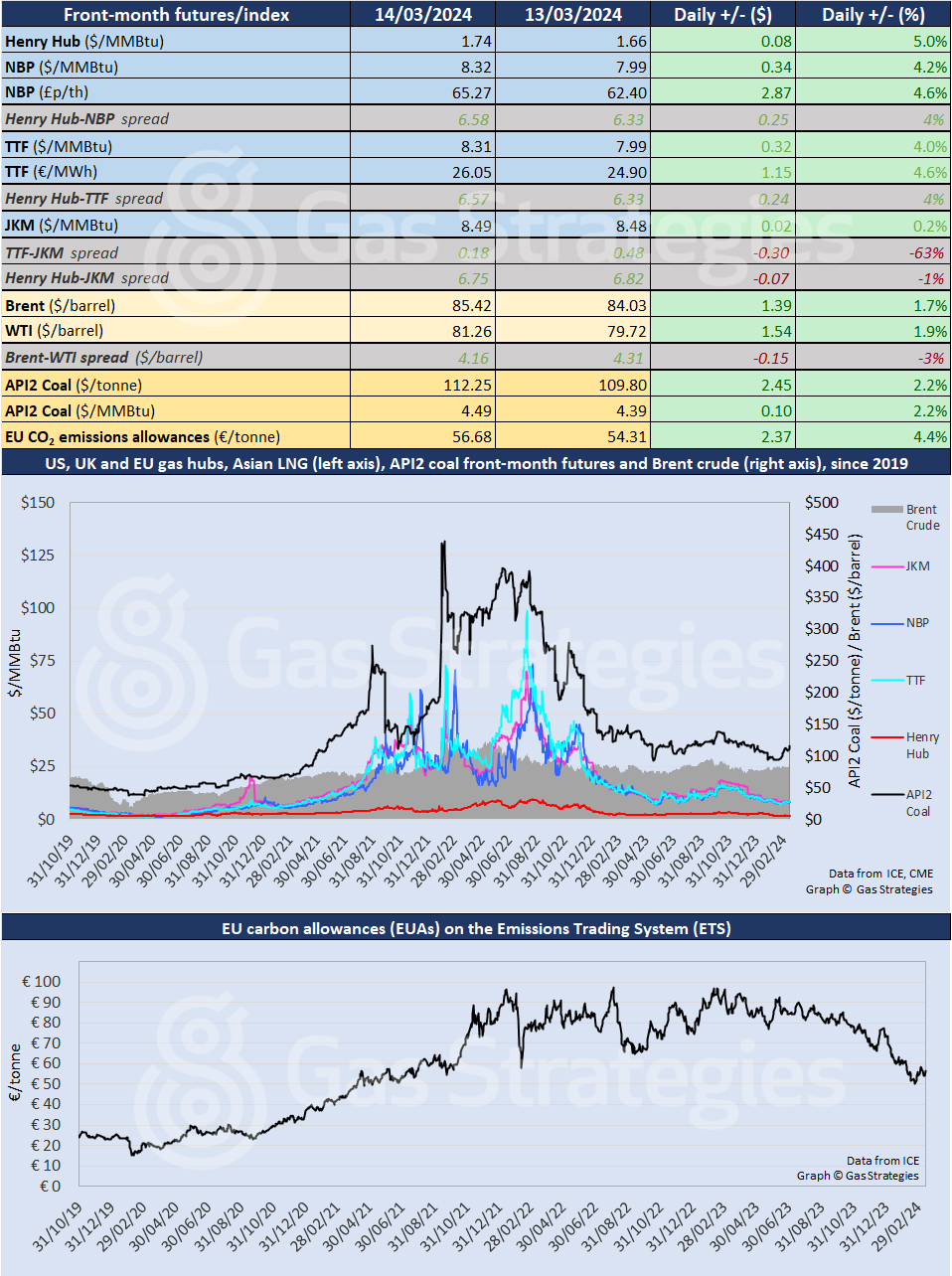

Energy prices in markets across the globe rose across the board on Thursday – most notably in the US, where Henry Hub futures rallied strongly after six consecutive declines. Expectations that government gas storage data would show an early injection rather than a withdrawal failed to materialise.

The US Energy Information Administration (EIA) estimated working gas in storage at 2,325 Bcf as of 8 March, down 9 Bcf from the previous week and way above the five-year historical range. The impact of that surprise may, however, be short-lived, given how high stocks are at the end of winter.

Stocks were 336 Bcf higher year-on-year and 629 Bcf – or 37% – above the five-year average of 1,696 Bcf for this time of year.

Perhaps more significantly, the level of storage has now wandered well outside the five-year maximum-minimum range and – with astronomical spring now only a week away – the deviation looks set to grow, given current market fundamentals. The vernal equinox in the northern hemisphere happens on Wednesday next week.

One bullish factor was a growing expectation that Freeport LNG might soon restart the 5 mtpa liquefaction train that has been undergoing repairs.

The front-month Henry Hub futures contract rose by 5.0%, from USD 1.66/MMBtu on Wednesday to USD 1.74/MMBtu on Thursday. It was climbing again, by around 1.5%, on Friday morning.

Natural gas futures were up strongly in Europe, with TTF rising by 4.0%, from USD 7.99/MMBtu on Wednesday to USD 8.31/MMBtu on Thursday, and NBP up 4.2%, from USD 7.99/MMBtu to USD 8.32/MMBtu.

In Asia, the JKM LNG price edged up 0.2%, from USD 8.48/MMBtu to USD 8.49/MMBtu, leading to a TTF-JKM spread of just USD 0.18/MMBtu.

Crude oil prices continued their rally, having well and truly broken out of their rangebound trading of recent weeks.

Front-month Brent crude was up 1.7%, from USD 84.03/barrel on Wednesday to USD 85.42/barrel on Thursday, the highest price since last October, while WTI was up 1.9%, from USD 79.72/barrel to USD 81.26/barrel, also the highest front-month price since last October.

European coal was up for the fourth consecutive session, with API2 rising by 2.2%, from USD 4.39/MMBtu on Wednesday to USD 4.49/MMBtu on Thursday.

European carbon prices rose with the tide, with EU emissions allowances up 4.4%, from EUR 54.31/tonne to EUR 56.68/MMBtu.

Front-month futures and indexes at last close with day-on-day changes:

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.