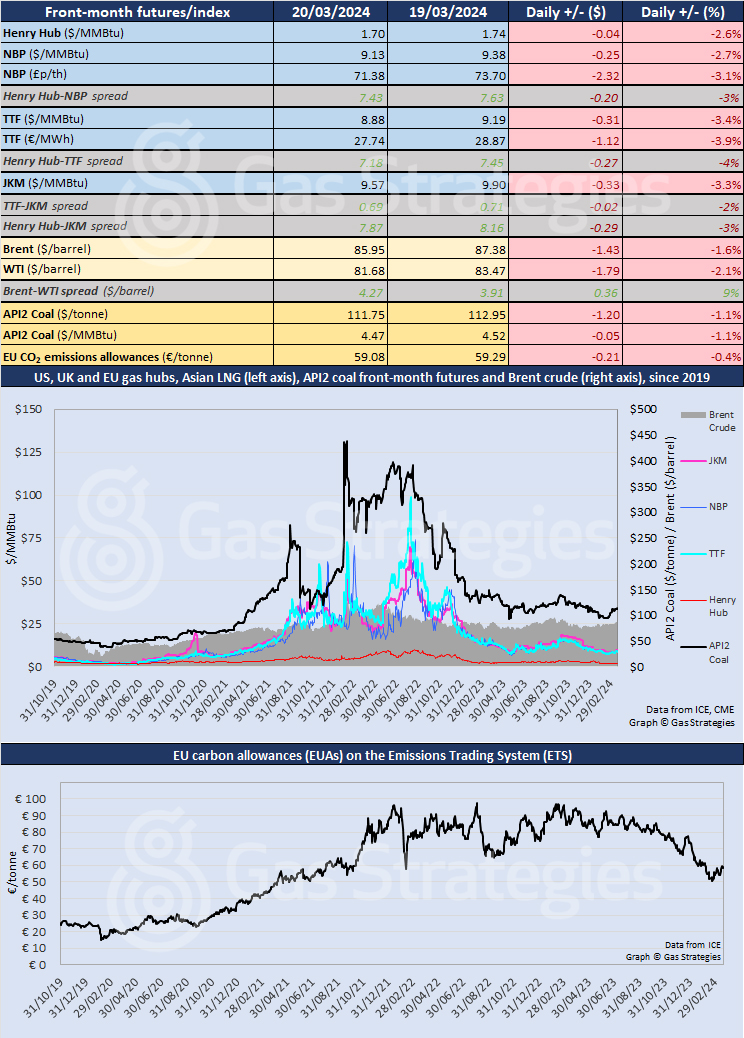

Prices in global energy markets fell across the board on Wednesday as the vernal equinox marked the start of astronomical spring in the northern hemisphere and the approaching end of the heating season.

In the US, front-month Henry Hub fell by 2.6%, from USD 1.74/MMBtu on Tuesday to USD 1.70/MMBtu, wiping out the gain in the previous session as forecasts pointed to warmer weather in the near term.

The price was edging down further on Thursday morning as the market awaited storage data from the Energy Information Administration, with some traders expecting an injection rather than a withdrawal. A similar expectation last week failed to materialise.

In an interview at CERAWeek, the CEO of Freeport LNG, Michael Smith, said repairs to one of the liquefaction trains were expected to be completed by May, following which capacity of the whole facility would increase by 10% from 15 mtpa to 16.5 mtpa. Repairs to another train are expected to be completed this week.

A fourth train is permitted but has yet to reach final investment decision. Discussions with potential customers continue.

As expected, the US Federal Reserve held interest rates for another month, with chair Jerome Powell signalling that rate cuts are likely later in the year, as inflation eases despite a recent monthly rise.

In the so-called “dot plot”, a majority of Fed officials expect rates to fall three times in 2024 but the rest would like to see fewer cuts. In the UK, the Bank of England announced it is holding interest rates.

In continental Europe, the April TTF contract fell by 3.4% – ending a run of five consecutive rises – from USD 9.19/MMBtu on Tuesday to USD 8.88/MMBtu on Wednesday.

In the UK, NBP was down 2.7%, from USD 9.38/MMBtu to USD 9.13/MMBtu.

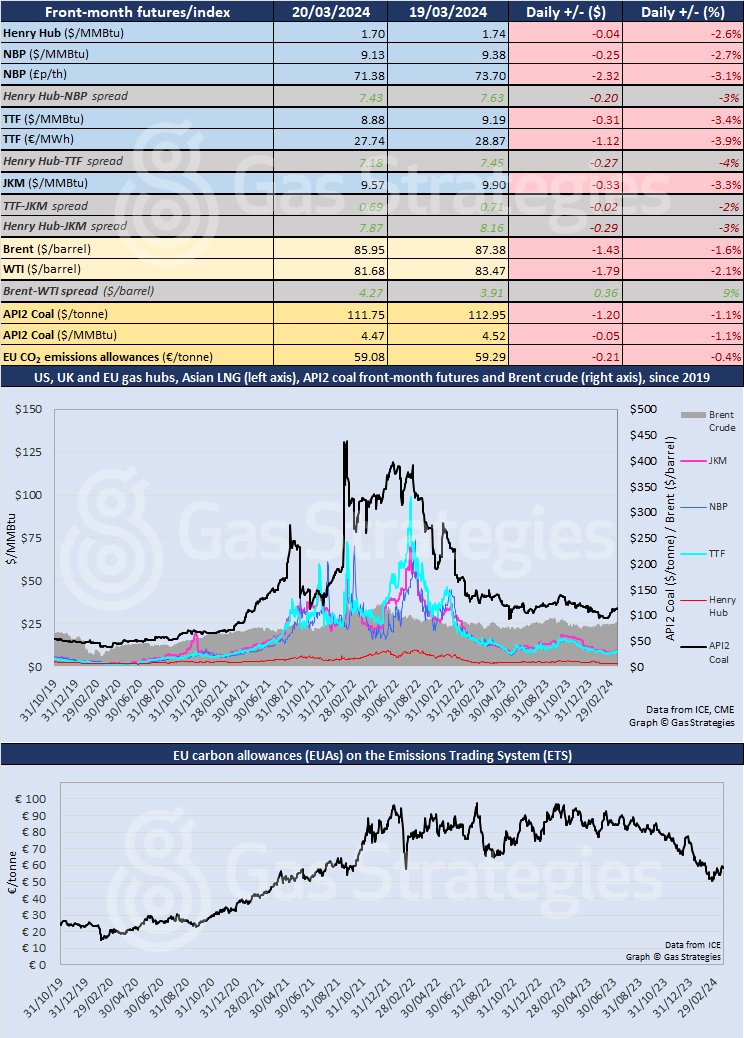

The Europe Union ends the winter with storage at unusually high levels. According to data from Gas Infrastructure Europe (GIE), storage facilities are just under 60% full, a good starting point from which to prepare for the coming winter, with political pressure building for imports of Russian LNG to cease.

UK storage is significantly less full, at 38%, but capacity is a much smaller share of peak demand than in other big consumers in Europe, so volatility is not unusual. It is currently on a gentle rising trend.

In Asia, the JKM LNG price slumped by 3.3%, from USD 9.90/MMBtu on Tuesday to USD 9.57/MMBtu on Wednesday, moving away from the psychologically significant level of USD 10/MMBtu for price-sensitive buyers.

Crude oil prices took a pause from their recent rally. Brent fell by 1.6%, from USD 87.38/barrel on Tuesday to USD 85.95/barrel on Wednesday, while WTI was down 2.1%, from USD 83.47/barrel to USD 81.68/barrel.

Front-month futures and indexes at last close with day-on-day changes:

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.