Crude oil prices maintained their upward momentum as a tumultuous week in Middle Eastern politics came to an end on Friday, in the wake of an attack on an Iranian embassy in Syria and the death of foreign aid workers in Gaza, both blamed on Israel.

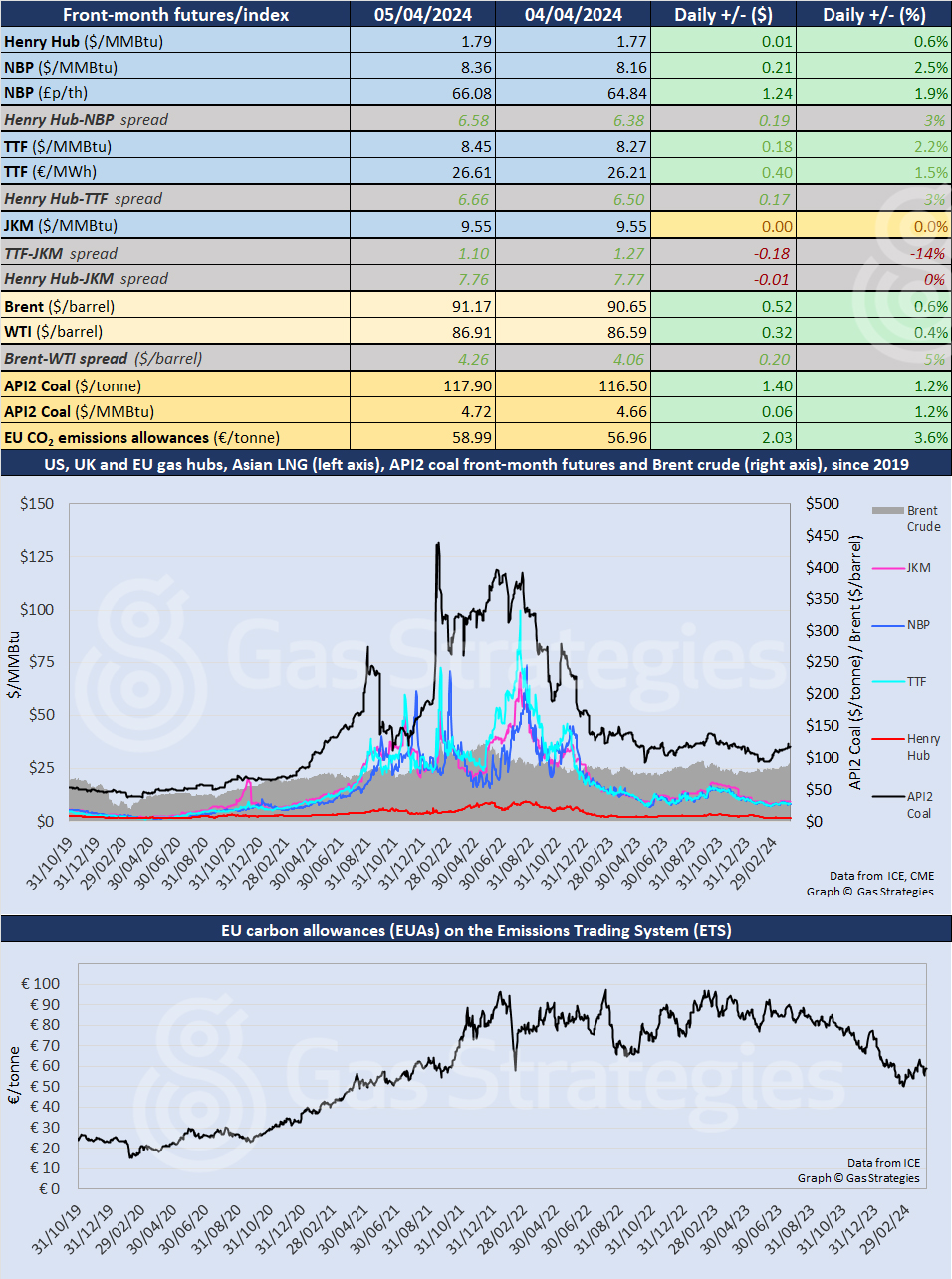

The Brent front-month contract pushed further into USD 90-plus territory, rising by 0.6% from USD 90.65/barrel on Thursday to close at USD 91.17/MMBtu on Friday. WTI was up 0.4%, from USD 86.59/barrel to USD 86.91/barrel.

Despite predictions from some quarters that the prospect of USD 100/barrel oil is looming larger, the rally lost steam over the weekend and prices were down in Monday morning trading, but with Brent still above USD 90/barrel.

Israel marked the six-month anniversary of its war with Hamas on Sunday by announcing it was withdrawing troops from the largest city in southern Gaza, Khan Younis. Reports followed on Monday that some Palestinians were returning to the devastation wreaked by Israeli military attempts to obliterate Hamas.

Ceasefire talks are under way in Cairo but fears remain that Israel still intends to attack the southern city of Rafah on the border with Egypt – where more than a million Palestinians are sheltering. The US and the UN have warned such an attack could lead to a humanitarian disaster.

European natural gas prices rose for the second consecutive session, with the TTF May contract rising by 2.2%, from USD 8.27/MMBtu on Thursday to USD 8.45/MMBtu on Friday. In the UK, NBP was up 2.5%, from 8.16/MMBtu to USD 8.36/MMBtu.

In Asia, the JKM LNG price was flat at USD 9.55/MMBtu, narrowing the TTF-JKM spread to USD 1.10/MMBtu.

Both European and Asia prices have been on an underlying flat trend in recent weeks but TTF and NBP have exhibited much more day-to-day volatility than JKM, which has been trading in a narrow range of USD 9.40-9.72/MMBtu for the past fortnight.

In the US, natural gas prices rallied after two consecutive falls amid expectations of production curbs and strengthening industrial demand. Front-month Henry Hub was up 0.6%, from USD 1.77/MMBtu on Thursday to USD 1.79/MMBtu on Friday. US gas output is currently below 100 Bcf/d.

European coal prices rallied, with API2 up 1.2%, from USD 4.66/MMBtu on Thursday to USD 4.72/MMBtu on Friday, with global markets still adapting to the impacts of the Baltimore bridge accident in the US, which has significantly curtailed its coal exports.

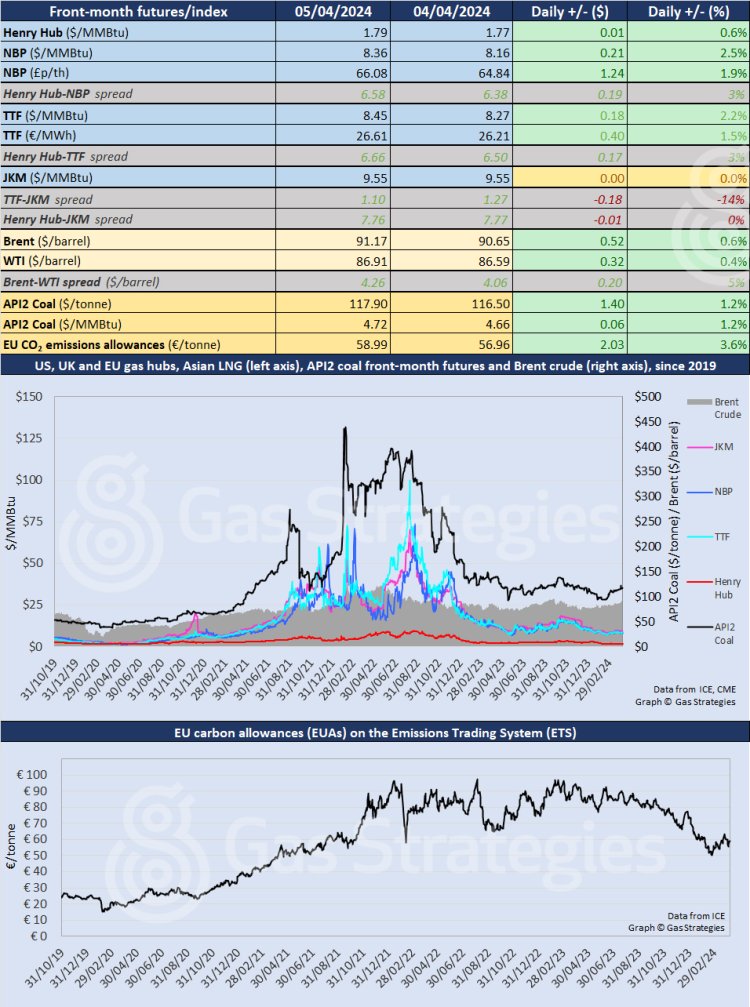

European carbon prices rallied after slumping last week, following a report from the European Commission of a record fall in emissions under the EU’s Emission Trading System (ETS) in 2023.

“The data reported by EU member states as of 2 April 2024 show a 15.5% decrease in emissions in 2023, compared with 2022 levels,” said the commission. “With this development, ETS emissions are now around 47% below 2005 levels and well on track to achieve the 2030 target of -62%.”

The commission attributes the fall mainly to a substantial increase in the production of renewable electricity, at the expense of coal and gas, and the “effectiveness and efficiency of the EU’s cap-and-trade system”.

EU emissions allowances were up 3.6%, from EUR 56.96/tonne on Thursday to EUR 58.99/tonne on Friday.

Front-month futures and indexes at last close with day-on-day changes:

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.