Natural gas prices rose sharply in all the main consuming regions on Wednesday, led by the US – where the expiry of the March futures contract saw April become the front month.

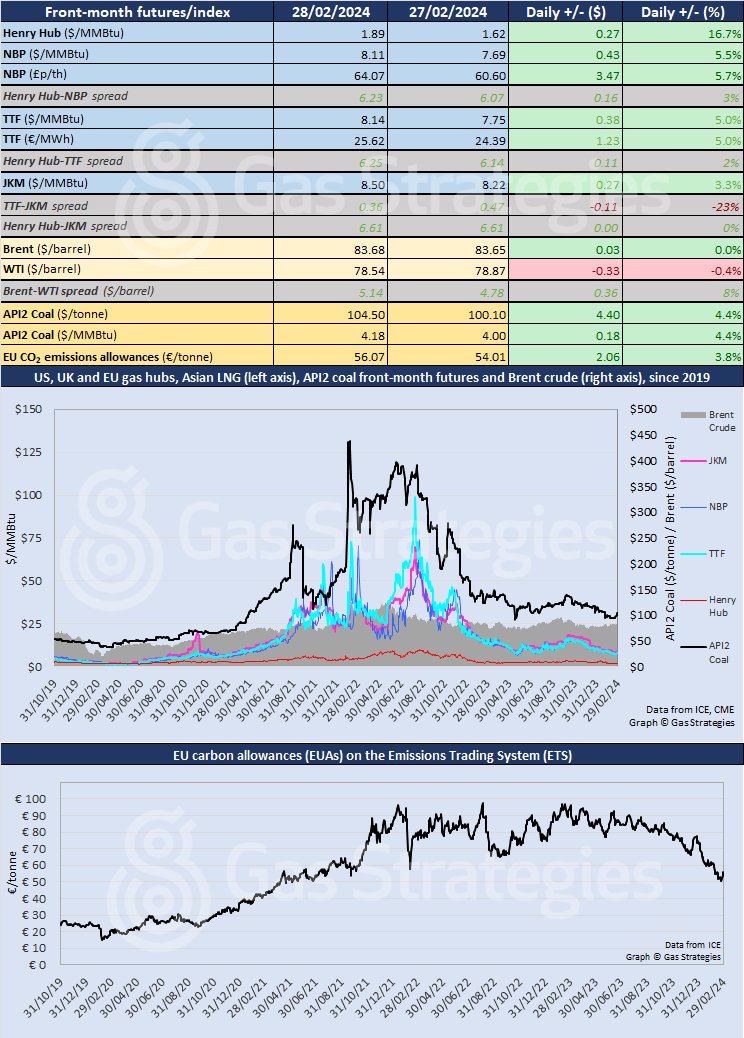

This meant that front-month Henry Hub gas closed at USD 1.89/MMBtu, 16.7% higher than the closing price for the March contract on Tuesday of USD 1.62/MMBtu.

Cooler weather and lower production have seen US prices rising in recent days but from lows in the region of prices last seen three decades ago. So there is some way to go before prices breach the USD 2/MMBtu threshold.

Extension of the partial outage at Freeport LNG, the second-largest export plant in the US, remains a driving factor for both US and European natural gas prices.

Significantly, European natural gas futures extended their rally for a third session on Wednesday, raising the question of whether this constitutes an end to the months-long straight-line decline since October, just as winter in the northern hemisphere is coming to an end.

In its morning report on Thursday, Energi Danmark says the rally “appears to be the result of short-covering among speculative buyers and technical signals than a sign of any fundamental change”. Prices were moving downwards on Thursday morning but recent days have seen several reversals to bearish starts.

In Continental Europe, TTF closed 5.0% up on Wednesday, from USD 7.75/MMBtu on Tuesday to USD 8.14/MMBtu. In EUR/MWh terms – removing currency conversion effects – front-month TTF is up 11.0% since Friday’s low, when the price was at around levels seen in the spring of 2021.

In the UK, NBP was up 5.5%, from USD 7.69/MMBtu on Tuesday to USD 8.11/MMBtu on Wednesday. In p/therm terms, the price is up 13.3% since Friday’s low.

READ Gas suppliers offer 97 Bcm of LNG and piped gas on EU joint purchasing platform

The European Commission announced on Wednesday that the first tender with a new mid-term product for joint gas purchasing under the EU Energy Platform had attracted offers for a total volume of 97.4 Bcm. This was almost three times the demand submitted by European companies through the AggregateEU mechanism.

Executive vice-president Maroš Šefčovič described this as “a remarkable outcome”, adding: “Through coordination and cooperation, we are boosting Europe's energy security in the face of a challenging geopolitical context.”

At the end of last year, EU legislators reached provisional political agreement on the hydrogen and decarbonised gases package, which will make joint purchasing of gas a permanent instrument. More tenders are due this year.

In Asia, the JKM LNG price rose by 3.3%, from USD 8.22/MMBtu on Tuesday to USD 8.50/MMBtu on Wednesday, its highest level since mid-February. The TTF-JKM spread is now USD 0.36/MMBtu.

Crude oil prices are currently in dynamic equilibrium, with bullish and bearish economic and geopolitical factors offsetting each other.

The US Federal Reserve appears to be in no hurry to start cutting interest rates but the worsening humanitarian crisis in Gaza continues to cause international alarm. Worries over global – and especially Chinese – demand are offset by optimism over demand trends in the US.

Brent edged up by a whisker to USD 83.68/barrel, while WTI fell by 0.4% to USD 78.54/barrel. Prices remained more or less flat on Thursday morning.

European coal and carbon prices continued to move upwards, in line with the rally in gas prices. API2 coal was up 4.4%, from USD 4.00/MMBtu on Tuesday to USD 4.18/MMBtu on Wednesday.

EU emissions allowances were up 3.8% to EUR 56.07/tonne. It is only a matter of days since they were testing the EUR 50/tonne threshold.

Front-month futures and indexes at last close with day-on-day changes:

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Subscription Benefits

Our three titles – LNG Business Review, Gas Matters and Gas Matters Today – tackle the biggest questions on global developments and major industry trends through a mixture of news, profiles and analysis.

LNG Business Review

LNG Business Review seeks to discover new truths about today’s LNG industry. It strives to widen market players’ scope of reference by actively engaging with events, offering new perspectives while challenging existing ones, and never shying away from being a platform for debate.

Gas Matters

Gas Matters digs deep into the stories of today, keeping the challenges of tomorrow in its sights. Weekly features and interviews, informed by unrivalled in-house expertise, offer a fresh perspective on events as well as thoughtful, intelligent analysis that dares to challenge the status quo.

Gas Matters Today

Gas Matters Today cuts through the bluster of online news and views to offer trustworthy, informed perspectives on major events shaping the gas and LNG industries. This daily news service provides unparalleled insight by drawing on the collective knowledge of in-house reporters, specialist contributors and extensive archive to go beyond the headlines, making it essential reading for gas industry professionals.