- Carbon neutral LNG deals have grabbed headlines but represent less than 1% of cargoes traded annually

- Emissions associated with ‘green’ cargoes are offset by carbon credits acquired in voluntary carbon markets

- No independent industry standard exists for verifying estimates of levels of emissions intended to be offset

- Offsetting emissions is a cheap, eye-catching solution but does not actually reduce LNG sector’s own emissions

Deals for ‘carbon neutral’, or ‘green’, LNG cargoes continue to grab headlines in the LNG space. September saw announcements by Naturgy of the first import of carbon neutral LNG into Spain and by BP of its first Asia Pacific carbon neutral LNG delivery to Taiwan’s CPC. But despite the media profile of these deals, they only represent a tiny proportion – 1% or less – of all LNG sold. Moreover, the whole area of carbon offsets, on which these carbon neutral cargoes rely, is seen as controversial, with concerns about the transparency of the so-called voluntary carbon markets in which the offsets are traded and doubts over how effective such schemes actually are in reducing CO2 emissions.

There is also a worry that offsetting is a relatively easy and cheap way to be seen to be doing something about LNG emissions, distracting attention from the much tougher decisions needed to actually reduce emissions from LNG operations. Nevertheless, offsetting is an essential part of the toolkit for reaching net zero emissions, and the process itself puts the level of emissions that have to be offset under scrutiny. In this feature, LNG Business Review takes a look at the growing trade in carbon neutral LNG cargoes and asks what contribution it could play in helping decarbonise the LNG chain.

Voluntary targets

There has been a string of announcements over the last 18 months of deals in which some proportion of the emissions associated with an LNG cargo have been offset, and the momentum has picked up in 2021, with a number of individual cargo deals, such as the Naturgy and BP ones mentioned above. Also, in what seems to be the first move of this sort, trader Vitol announced in March that it would provide its customers with the option to offset emissions on any cargo up to the DES (Delivered Ex Ship) point. In July, Shell announced what it claims is the first multi-cargo term deal for carbon neutral LNG with PetroChina.

But despite the flurry of press announcements, the proportion of all LNG cargoes which have their emissions offset remains tiny. Wood Mackenzie estimated in early July 2021 that some 16 cargoes of this sort had been traded in total, though according to an LNG industry expert, “the number now is certainly over 20, probably around 25.” With the total annual trade in LNG amounting to over 5,000 cargoes, this is less than 1% of the total.

The rationale of these deals is that the parties have agreed that the emissions associated with the cargo will be offset by carbon credits acquired in the so-called voluntary carbon markets, with the responsibility for doing so usually being with the seller. These voluntary markets are distinct from the compliance markets, such as those that exist in Europe and California, where there is a legal requirement under certain circumstances to have emissions permits, which can be acquired through emissions trading.

In the case of LNG, the carbon neutral LNG deals seem to be entirely voluntary, in the sense that, as far as one can tell, they are not being done for any regulatory compliance, but to meet voluntary corporate targets. One of the clear trends over the last year or so is the number of companies that have set voluntary targets for decarbonising aspects of their business. More than 3,000 companies have now signed up to the UN’s ‘Race to Zero’ global campaign to reduce their net emissions to zero by 2050 by various means, such as improving manufacturing processes, switching to low-carbon fuels, installing carbon capture and storage (CCS), buying renewable electricity – and by acquiring carbon offsets.

There are two parts to putting together a carbon neutral LNG deal: the first is to quantify the emissions to be offset and the second is to purchase the offsets themselves. The quantification step is not necessarily straightforward. Firstly, it has to be decided what emissions are to be offset. Some of the deals involve offsetting the emissions along the LNG chain up to the delivery, or DES, point – sometimes known as well-to-tank (WTT) emissions. The WTT emissions probably make up on average about 25% of the total greenhouse gas (GHG) emissions in the LNG chain, with the remainder being largely made up of the CO2 emitted when the regasified LNG is burned.

However, WTT emissions vary considerably from one project and delivery route to another. Published estimates indicate that the WTT emissions of LNG deliveries to Japan range from less than 0.5 tCO2(e)/tLNG for the lowest emitting LNG exporters to nearly 1.5 tCO2(e)/tLNG for the highest emitters. Moreover, there is no industry standard yet for how the WTT emissions are calculated, and different approaches can lead to different answers, as demonstrated in a study commissioned by Cheniere which showed that, depending on the source and methodology adopted, WTT emissions estimates for US LNG supplied to China can range from 1.19 to 2.95 tCO2(e)/tLNG. Despite these difficulties, some benchmarking tools are now available, such as that produced by Wood Mackenzie, which is used by Vitol to estimate the emissions to be offset for its carbon neutral LNG offer. However, there is not yet any independent industry standard for verifying the companies’ estimates of the levels of emissions that they are intending to offset.

Carbon credits

The next step in the process is to acquire carbon credits sufficient to offset the estimated emissions levels. For that, companies turn to the voluntary carbon markets. These voluntary markets have attracted a lot of criticism, and it is clear that the quality of offsets can be notably variable. One key area of criticism is over whether projects claiming to reduce emissions are truly ‘additional’: does the purchase of the credits actually lead to emissions reductions which would not otherwise have occurred? Some projects rely on counterfactual arguments, which can arouse scepticism – for example, claiming the conservation of forest areas and preventing their clearance as a reduction in emissions. Another issue is that some of the credits on sale relate to historical projects, which somewhat stretches the additionality criterion.

But even if these doubts can be overcome, the fact that such a high reliance is placed on biological sinks such as forestry raises issues in itself. Forests take a long time to grow, are susceptible to accidents and disasters such as forest fires and need to be maintained over the long-term – logically until at least 2050 if the goal is net zero by this time. For these reasons, there is an argument that the amount of credits purchased should be greater than the expected emissions in order to cater for this risk. It is not clear if this principle is being followed in any of the carbon neutral LNG deals announced.

Several organisations now offer to verify and certificate the emissions from offset schemes as a means of providing assurance on at least some of these issues. Vitol has disclosed that in its scheme it will rely on certification from one or other of the UN Clean Development Mechanism, Verified Carbon Standard (VERRA), Gold Standard, American Carbon Registry, China Green House Gas Voluntary Emission Reduction Programme or Climate Action Reserve. However, despite the efforts of such organisations, the market is far from commoditised, and large scale buyers of credits need at least to adopt an informed buyer approach. This is one of the reasons why oil majors such as Shell and Eni have become directly involved in carbon offsetting projects, and see this as not only a key tool in meeting their own corporate emissions targets, but also an area of competitive advantage.

But the scalability of the voluntary carbon market remains a big question. There are limits to the areas that can be forested, and impacts on land available for agriculture. McKinsey estimates that, allowing for what it calls “mobilisation” challenges, the global supply of carbon credits might be in the range 1-5 GtCO2 by 2030. With the global LNG market heading for in excess of 500 mtpa by 2030, offsetting the entirety of LNG emissions would require nearly 2 GtCO2/year to be offset, potentially leaving little or nothing for the multitude of other sectors looking to offset emissions.

Voluntary carbon markets

The voluntary carbon market is a market in carbon credits, which are financial instruments based on amounts of CO2 equivalent emissions removed or avoided. Corporations who wish to offset emissions can purchase these credits and then cancel or retire them so that they can no longer be traded.

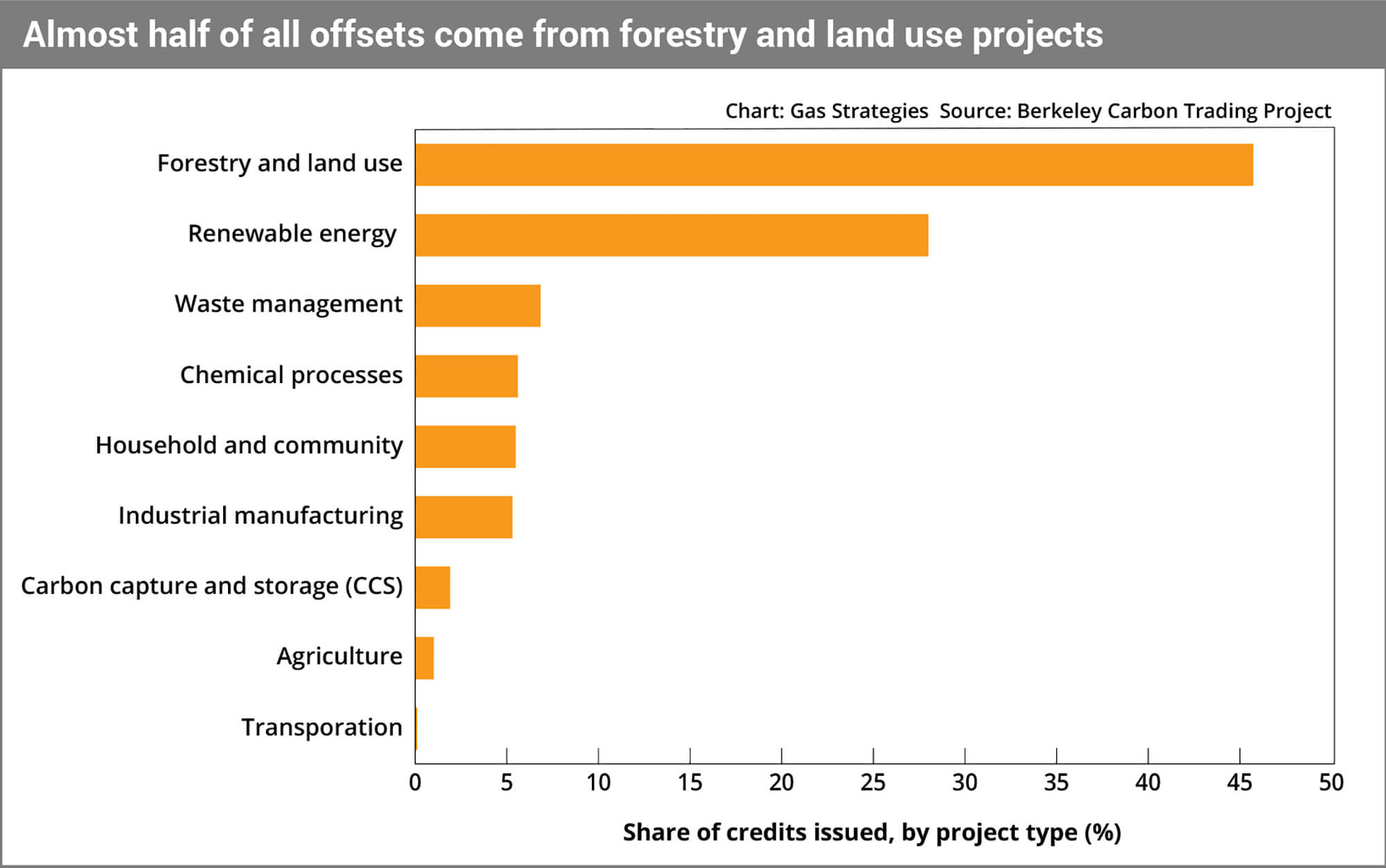

The largest sector of activity is forestry, agriculture and land use projects, and this is also the fastest growing sector.

There is no overall regulation of voluntary carbon markets, but various organisations such as VERRA, Gold Standard and American Carbon Registry verify and certify emissions. The aviation industry, which relies heavily on offsets to counter its emissions, has signed up to a UN initiative called the Carbon Offsetting and Reduction Scheme for International Aviation (CORSIA), which seeks to regulate and standardise offsets, and CORSIA-approved status is used as a standard by other sectors.

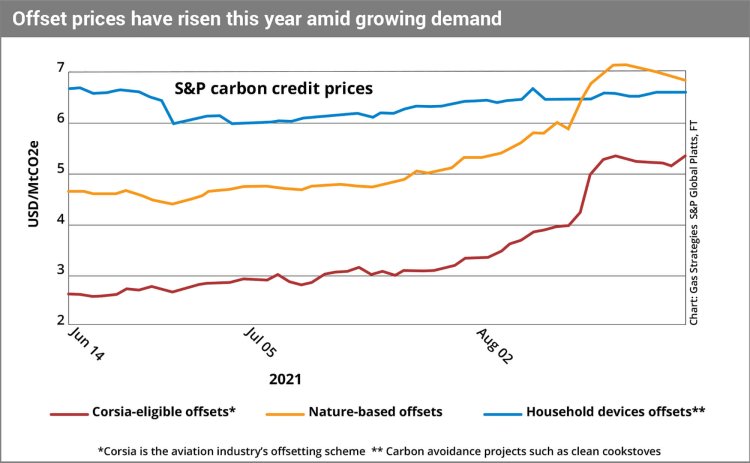

The overall volume traded on the voluntary market is estimated at 104 Mt CO2(e) in 2019 with a value of around USD 600 million.

Voluntary credits are hard to commoditise, and most trading is over-the-counter (OTC) rather than exchange based, though exchange trading is just starting to emerge. Pricing is therefore sometimes difficult to establish, but Platts now report prices for CORSIA-eligible and other offset categories.

No panacea

It is not clear in most of the carbon neutral LNG deals who is paying the cost of offsetting – is the buyer paying a premium, or is the supplier accepting an extra cost, or is it being shared? This raises the question of how much it actually costs to offset emissions in this way. The answer is that it looks surprisingly cheap. One feature of the voluntary carbon markets is the relatively low price of emissions, due to a historical surplus of credits. And though rapidly growing demand has pushed up prices, the price of emissions eligible for CORSIA – the scheme adopted by the international aviation industry, which is a major user of offsets – is still less than USD 6/tCO2(e), which compares with a European ETS price which rose above EUR 60/t (USD 70/t) for the first time in September.

This means that it does not cost very much to offset a cargo, particularly if it is only the WTT emissions that are being offset. Platts now publish assessments of the premium attached to carbon neutral LNG (CNL), based on carbon credit prices in the voluntary carbon market and a standard delivery from Australia to Japan/Korea/Taiwan (JKT). On 23 September, the Platts JKT CNL WTT premium assessment was USD 0.115/MMBtu, while the premium for full chain emissions, including combustion, which Platts refers to as JKT CNL WTW (well to wheel) was USD 0.521/MMBtu. On the same date the JKM LNG spot price was USD 26.36/MMBtu, making the cost of offsetting seem insignificant compared with the recent fluctuations in price.

The relatively low cost of offsetting emissions perhaps leads to a danger that it is an eye-catching, and relatively cheap, way of doing something about GHG emissions, while not actually reducing the LNG sector’s own emissions. While offsets are an essential tool to reach net zero emissions, there is an argument that they should be reserved for use in tackling emissions that cannot be reduced and so need to be offset. The Oxford Principles for offsetting published in 2020 take as their first principle that the priority should be to reduce emissions ahead of offsetting them. So far, the LNG industry has, arguably, not done much to adhere to this principle.

The main components of WTT emissions are upstream methane emissions, CO2 venting from acid gas removal, liquefaction plant gas turbine exhausts and shipping fuel consumption, with the relative proportions varying from one project to another. Tackling these requires serious investment in facilities such as CCS or replacement of gas turbines with electric drives – though in the case of US projects they can avoid capital investment in methane emission reduction by pushing the responsibility back on to their gas suppliers.

These sorts of emission-reducing investments require a much higher effective carbon price than the current voluntary market price and probably even more than the current ETS price. Estimates of the carbon price needed to make CCS work generally are over USD 100/tCO2(e). The question is whether voluntary schemes will ever lead to major investments of this sort. Currently the answer seems to be no, as exemplified by Santos’ decision to go ahead with the Barossa development without putting in the investment to capture the CO2 from a project that produces as much CO2 as it does LNG. But if LNG prices remain anywhere near as high as they are now, producers are going to come under increasing pressure to reinvest their cash flows to actually reduce emissions, rather than offsetting the odd cargo here and there. - DJD

Subscription Benefits

Our three titles – LNG Business Review, Gas Matters and Gas Matters Today – tackle the biggest questions on global developments and major industry trends through a mixture of news, profiles and analysis.

LNG Business Review

LNG Business Review seeks to discover new truths about today’s LNG industry. It strives to widen market players’ scope of reference by actively engaging with events, offering new perspectives while challenging existing ones, and never shying away from being a platform for debate.

Gas Matters

Gas Matters digs deep into the stories of today, keeping the challenges of tomorrow in its sights. Weekly features and interviews, informed by unrivalled in-house expertise, offer a fresh perspective on events as well as thoughtful, intelligent analysis that dares to challenge the status quo.

Gas Matters Today

Gas Matters Today cuts through the bluster of online news and views to offer trustworthy, informed perspectives on major events shaping the gas and LNG industries. This daily news service provides unparalleled insight by drawing on the collective knowledge of in-house reporters, specialist contributors and extensive archive to go beyond the headlines, making it essential reading for gas industry professionals.