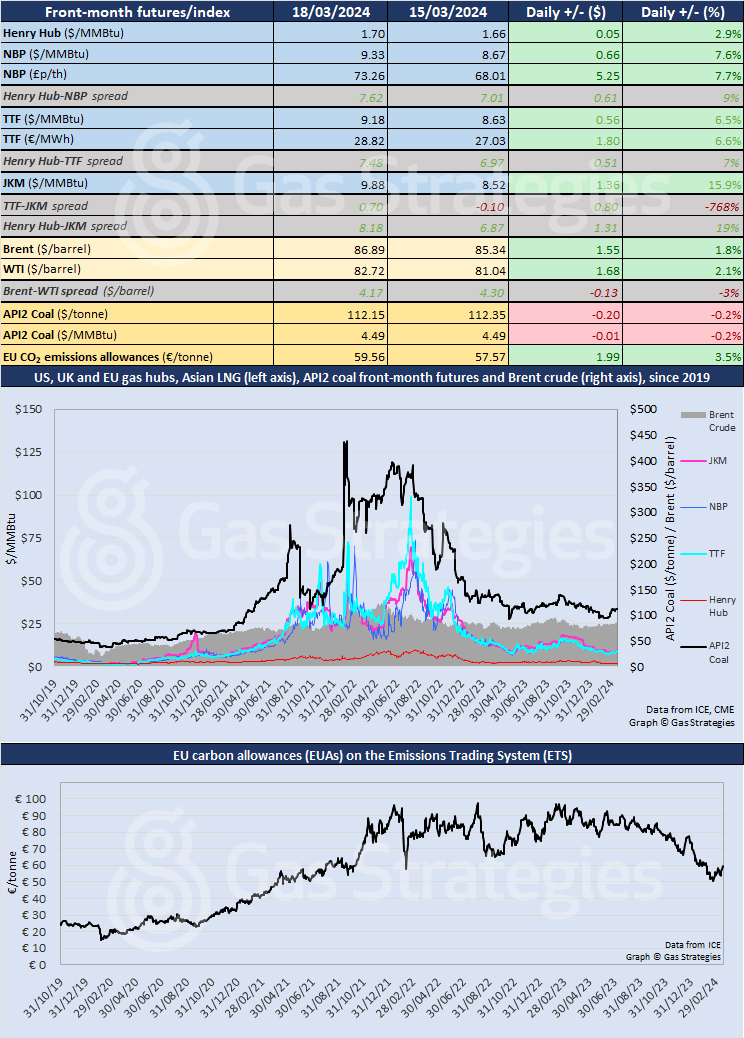

Natural gas markets had an electrifying day on Monday, with front-month futures rising in all three main consuming regions – notably Asia, where the JKM price leapt by almost 16% on expiry of the April contract. Prices continued to rise sharply in Europe and even the US managed an increase amid a mostly declining trend.

It is not unusual for the expiry of a JKM futures contract to lead to a sharp movement in the front-month price.

The closing price of the May JKM contract yesterday was USD 9.88/MMBtu, a 15.9% rise from the closing price of the April contract on expiry, USD 8.52 /MMBtu. This is the closest that front-month JKM has been to USD 10/MMBtu since mid-January. The low point of USD 8.13/MMBtu was on 23 February.

Ironically, the rise came as industry leaders at the first day of the CERAWeek conference in the US were speculating that low LNG prices would lead to an increase in demand, while Shell CEO Wael Sawan said that was already happening.

European gas futures again confounded bearish fundamentals, with April TTF up 6.5%, from USD 8.63/MMBtu on Friday to USD 9.18/MMBtu on Monday and NBP up 7.6%, from UDSD 8.67/MMBtu to USD 9.33/MMBtu. Prices were on a declining trend on Tuesday morning.

Yesterday’s rises came amid an unplanned outage at a Norwegian gas field, with supply disruptions expected to end today, and the steep rise in front-month JKM, which makes Asia a more attractive market for spot LNG cargoes, subject to shipping costs. The TTF-JKM spread is now USD 0.70/MMBtu.

In the US, front-month Henry Hub was up 2.9%, from USD 1.66/MMBtu on Friday to USD 1.70/MMBtu on Monday, continuing the sawtooth pattern of the past week, after a week of consecutive declines earlier in the month. The rise came amid short-term forecasts of cooler weather.

An interesting cameo during the CERAWeek conference was the statement by US energy secretary Jennifer Granholm that Biden’s LNG export permitting pause would be “well in the rear-view mirror” by the time delegates assemble for CERAWeek 2025.

Crude oil prices continued to climb, with front-month Brent up 1.8%, from USD 85.34/barrel on Friday to USD 86.89/barrel on Monday, and WTI up 2.1%, from USD 81.04/barrel to USD 82.72/MMBtu. Crude prices were last at these levels in October 2023.

The European API2 coal price edged down by 0.2%, remaining at USD 4.49/MMBtu, while carbon prices were up, with EU emissions allowances rising by 3.5% to EUR 59.56/tonne.

Front-month futures and indexes at last close with day-on-day changes:

Time references based on London GMT. Brent, WTI, NBP, TTF and EU CO2 data from ICE. Henry Hub, JKM and API2 data from CME. Prices in USD/MMBtu based on exchange rates at last market close. All monetary values rounded to nearest whole cent/penny. Text and graphic copyright © Gas Strategies, all rights.

Subscription Benefits

Our three titles – LNG Business Review, Gas Matters and Gas Matters Today – tackle the biggest questions on global developments and major industry trends through a mixture of news, profiles and analysis.

LNG Business Review

LNG Business Review seeks to discover new truths about today’s LNG industry. It strives to widen market players’ scope of reference by actively engaging with events, offering new perspectives while challenging existing ones, and never shying away from being a platform for debate.

Gas Matters

Gas Matters digs deep into the stories of today, keeping the challenges of tomorrow in its sights. Weekly features and interviews, informed by unrivalled in-house expertise, offer a fresh perspective on events as well as thoughtful, intelligent analysis that dares to challenge the status quo.

Gas Matters Today

Gas Matters Today cuts through the bluster of online news and views to offer trustworthy, informed perspectives on major events shaping the gas and LNG industries. This daily news service provides unparalleled insight by drawing on the collective knowledge of in-house reporters, specialist contributors and extensive archive to go beyond the headlines, making it essential reading for gas industry professionals.